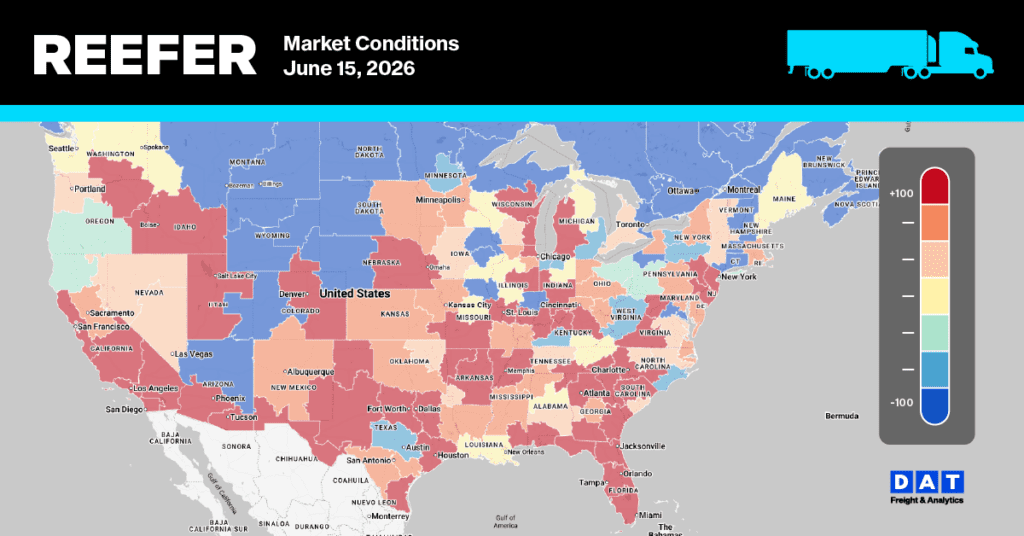

The produce freight market is quietly unwinding. Florida — the season’s dominant story for weeks — continues its rapid descent, with rates falling another 3–14% across all lanes as the summer season winds down and load counts thin out. California’s entire coastal complex flipped from Slight Shortage to Adequate this week across every district (Imperial/Coachella, Kern, Oxnard, Salinas, Santa Maria, South/Central), a broad truck availability reset that signals the spring tightness has cleared. Nogales softened across most lanes. The one market bucking the trend: Yakima Valley, which upgraded from Adequate to Slight Shortage — cherry and early apple season is tightening trucks in the Pacific Northwest, and rates are holding firm with no week-over-week change reported (new entries, no prior-week comparisons available). South Texas showed a mixed picture: slight gains on shorter lanes (Atlanta +5%, LA +12%, Miami +9%) but continued softening on the Northeast corridors. Vidalia onions remain flat and Adequate across all lanes — the pack is running at a steady pace with no supply disruption.

1. Central and South Florida — Shortage, winding down fast

Florida remains in Shortage conditions, but this is a shrinking market. The commodity mix tells the story: beans, cabbage, cantaloupes, and corn that appeared last week are gone from the report this week. What remains is a late-season mix of okra, peppers, squash, tomatoes, and watermelons. Load counts are falling and rates are following.

Florida → Baltimore has now shed roughly $700/load in two weeks (from ~$5,000 to $4,300). The season-close is approaching. Expect this market to go quiet within the next few weeks.

2. Yakima Valley & Wenatchee — Slight Shortage, cherry season arrives

Yakima is the only market tightening right now. The district upgraded from Adequate (June 9) to Slight Shortage this week, driven by cherry harvest demand layered on top of ongoing apple, blueberry, pear, and rhubarb movement. No week-over-week percentage changes are shown — these are new rate entries for the season’s tightened conditions.

Cherry season is the catalyst here – USDA vols up 400% w/w and 88% y/y. Yakima is the only district tightening in a broadly softening national market. Watch for additional rate pressure over the next 2–3 weeks as harvest volume peaks in the next three weeks.

3. Mexico Crossings Through South Texas — Adequate, mixed direction

South Texas is absorbing some displaced demand from Florida’s pullback, but the picture is lane-specific. Short-haul and backhaul lanes (Atlanta, LA, Miami) firmed up; longer Northeast corridors softened.

Narrative flag: LA +12% is the standout. Single-week move on a long backhaul lane that’s been impacted by immigration enforcement since last September.

4. California — Broad reset to adequate across all districts

Every California district flipped from Slight Shortage to Adequate this week. This is a significant availability shift — trucks are no longer tight across the California complex. Rates followed, with most lanes flat to down but still higher y/y.

5. Mexico Crossings Through Nogales — Adequate, broadly softer

Dallas +9% bucks the trend on an otherwise broadly declining board. Flag for cross-check. Dallas is the only World Cup Soccer host city showing a consistent pattern — rates into Dallas firmed across three independent origins (Nogales +9%, Imperial +7%, Santa Maria +7%) this week. Dallas hosting semifinal matches starting this month is the most plausible mechanism for the Dallas signal.

6. Vidalia District Georgia — Adequate, all lanes flat

Vidalia onions are running steady. No rate movement across any lane — consistent with a mid-pack-season cadence.

What this means for carriers, shippers, and brokers

Carriers: The window to hold rate in Florida is closing fast. Load counts are thinning, the commodity mix is narrowing, and rates are falling week over week. If you’re positioned in the Southeast, start planning your repositioning now — either north toward summer produce markets or west toward California. The real opportunity right now is Yakima: cherry season just tightened trucks to Slight Shortage, and with a broad commodity mix (cherries, blueberries, apples, pears), there’s consistent freight heading to every major destination. Northeast lanes out of Yakima ($8,700–$9,700 range) are the sweet spot.

Shippers: California just got meaningfully easier. Every district — Salinas, Santa Maria, Imperial, Kern, Oxnard, South/Central — flipped to Adequate this week. If you were struggling to cover loads during the spring Slight Shortage period, this week’s availability reset is your window to renegotiate or lock in spot coverage at improved rates. The exception is Yakima: if you’re moving cherries, blueberries, or tree fruit east, book early — this market is tightening and typically stays that way through peak summer harvest.

Brokers: Florida is a managed exit, not a market to chase. Focus attention on building Yakima capacity now before the cherry peak tightens the board further. South Texas remains a useful bridging market — Atlanta, Miami, and LA lanes firmed up this week — but the Northeast corridors (Boston, New York, Philadelphia) are softening. California offers improved coverage across the board, but watch the outlier moves on Santa Maria → Seattle (+11%) and South Texas → LA (+12%) — these could be noise or early signals of sub-regional demand shifts worth tracking next week.

National reefer spot rate trends

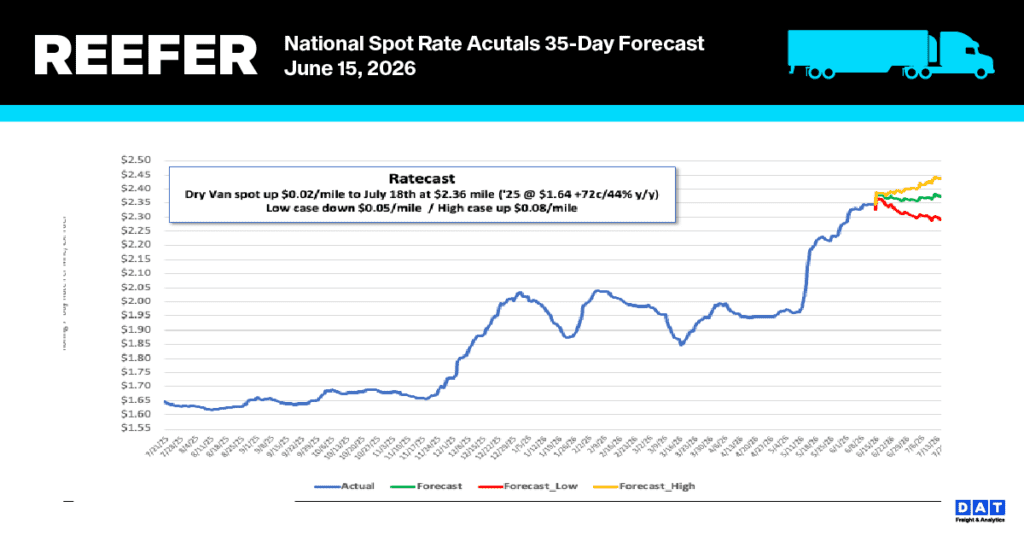

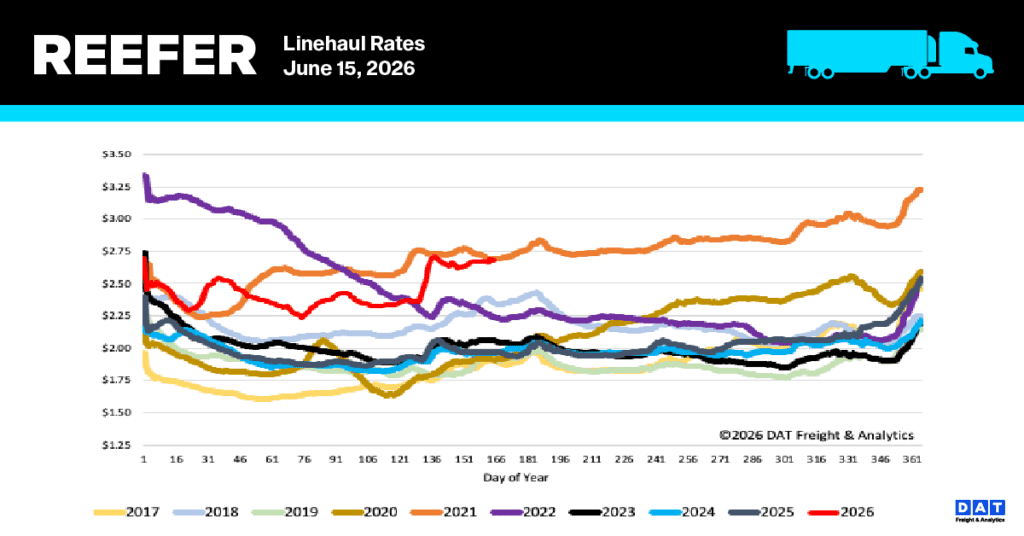

National reefer linehaul rates settled at a 7-day rolling average of $2.68 per mile after a slight one-cent decrease last week. The market remains exceptionally robust, currently 36% ($0.71) above last year’s levels and 26% ($0.70) higher than the non-pandemic five-year average. After gaining $0.32 per mile during Roadcheck Week, the reefer sector has maintained most of those increases and is now within $0.02 of the Week 24 record established in 2021.

Current spot rates for fruits and vegetables in key produce hubs are averaging $4.09 per mile. Although this represents a week-over-week decline of approximately $0.07, it remains $0.66 higher than the same period last year. As California’s produce season gains momentum, USDA volumes surged 17% week-over-week and 13% year-over-year; consequently, truckload rates in California are now $0.83 per mile above last year’s levels. On a broader scale, domestic produce volumes in the U.S. grew by 7% last week, despite being 14% lower year-to-date. Meanwhile, Mexican import volumes rose 4% week-over-week, remaining consistent with last season’s year-to-date figures. Canadian imports also saw a weekly increase of 10%, though they currently sit 3% lower year-to-date.

Reefer Market Conditions

With Independence Day approaching and the seasonal surge in reefer demand intensifying, equipment availability tightened as postings dropped 9% last week—now 25% behind last year and 47% below historical norms. Load volumes also softened, falling 7% week-over-week, yet they remain 48% higher than last year. This imbalance pushed the load-to-truck ratio up by 2%, reaching 17.17.