2017 was a wild year, as freight transportation faced one disruption after another.

The biggest influences were the Four Es:

- Economic growth

- E-commerce

- Electronic logging devices

- Extreme weather (including Hurricanes Harvey and Irma)

Those four factors added up to extraordinary pressure on spot market truck capacity, driving rates up as high as we’ve seen them since at least 2010, when we established the freight rates database that forms the foundation of DAT RateView.

I’ve heard these trends described as a “perfect storm.” I disagree, because that phrase implies that the storm will pass, and the trends will return to normal. Looking at this year’s demand, capacity and rate data, however, I see a longer-term trend building. This period of elevated rates is only the beginning of a “new normal” era in freight transportation.

Here’s evidence of the ongoing trend, in two years of load-to-truck ratios, spot market rates, and contract rates for van freight:

Load-to-truck ratios and rates declined steadily throughout 2015 and into the middle of 2016. (That slump was triggered by the collapse of oil prices at the end of 2014.) By January 2017, I saw clear signals that the 18-month freight recession was over, and spot market rates started to climb in earnest. Contract rates took a little while to catch up, which is typical. They’re expected to continue rising in 2018. As carriers and shippers renew their contracts, we are hearing about the largest increases in several years, including some increases well above 5%.

Now for those Four Es: economic growth, e-commerce, ELDs, and extreme weather:

1. Economic Growth Exceeds 3%

The economy is growing faster than it has in more than a decade, with year-over-year increases above 3% in the U.S. gross domestic product (GDP) for the second and third quarters, and similar expectations for Q4. We haven’t seen three consecutive quarters of 3% GDP growth since 2005.

Oil prices just hit $60 per barrel, which I predicted a few weeks ago, to some skeptical responses. More important, oil has been above $45 since Q4 2016. The $45 threshold is important, because at that level, energy companies are motivated to increase drilling and invest in new pipelines. Both activities generate a lot of freight, primarily for the flatbeds that move pipe and construction equipment to job sites. U.S. companies also ratcheted up manufacturing of petroleum byproducts, including plastic resins, which typically move in vans.

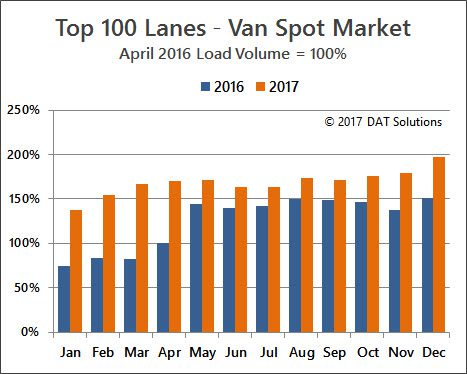

Here’s how the increased freight volume played out in the spot market for van trailers:

The graph shows a steady, year-over-year increase (orange bars for 2017 are higher than 2016, in blue) in spot market van loads. This information comes from DAT RateView, so it comes from rate agreements and carrier settlements, for loads that actually moved. There was also a big increase in the number of loads offered on DAT load boards, but that type of increase can sometimes be driven by urgency and/or a shortage of available trucks, as well as pure demand.

Expect this urgency to continue through the end of December, at a minimum. New tax rules go into effect in less than a week, so plenty of businesses will do whatever they can to accelerate tax-deductible activities, including purchases. On the other hand, they might be somewhat less enthusiastic than usual about taking end-of-year revenue under today’s tax rates. We’ll know more in a few days. Generally speaking, what’s good for business is good for freight volume. So it looks like 2018 will be a very busy year in trucking.

2. E-Commerce Changes Shipping Patterns

Back in the olden days, before 2013, the retail freight season hit its peak in October. Container ships docked in Los Angeles or Long Beach, the freight was unloaded, sorted and moved on rail intermodal or van trailers to regional distribution centers across the country. Then the retailers took over, shuttling goods to stores via private or dedicated fleets, to balance inventories in time for Thanksgiving weekend. In 2013, a new freight pattern began to emerge, with a second peak in December. E-commerce has been growing at a rate of 14% per year ever since. Now there are twice as many online shoppers compared to 2013, and packages are being delivered until the very last minute — in some cases as late as Christmas Day!

It doesn’t end there. December 26 is one of the three busiest shopping days of the year, with returns, exchanges and gift card redemptions. Even in January, which used to be a sleepy month in freight transportation, there’s continued demand for vans, as retailers re-stock inventories to accommodate those gift card-bearing shoppers. Now the lull may not happen until February, and it probably won’t last more than a few weeks.

3. Electronic Logs Restrict Driver Flexibility

Of course, the ELD mandate also took effect last week, and that contributed to the capacity crunch. Most large carriers installed ELDs long ago, but the smallest fleets and owner-operators held out, many until the last minute and beyond. With Christmas landing on a Monday, the vast majority of drivers would have wanted to get home by Friday, no matter what kind of logs they use, but ELDs may have convinced a lot more of them to take all or part of the week off between the December 18 mandate day and the big holiday weekend.

Some of those drivers are so opposed to ELDs that they plan to retire or find a different line of work in the new year. Driver turnover is already at 85% among small fleets, and it’s even higher at the big carriers, so it wouldn’t take much to cause a serious driver shortage. We’ve written a lot about ELDs on the DAT blog, and in our ELD Survival Guide, so I won’t go into detail here. Suffice it to say that electronic logs aren’t going away, and it will take time for those small fleets to adjust their operations to fit the new reality.

4. Extreme Weather Adds to the Craziness

Back-to-back hurricanes on the U.S. mainland destroyed lives and property, and caused massive disruptions in freight transportation all over the country. Hurricane Harvey had the biggest impact on freight because Houston is a nexus for rail and sea traffic as well as trucking. There was a ripple effect from Harvey, compounded by Hurricane Irma, as freight movements were canceled and re-routed repeatedly to re-stock not only the storm-affected areas but all the surrounding regions that were served by distribution centers in the Houston area. It took months for the shipping patterns to return to normal, and by then we were in the middle of the holiday freight season. Upside for truckers: If the weather is warm in the Southern band of states this winter, as expected, there may be a lot more demand than usual for flatbeds to help with off-season rebuilding and other construction in Texas and Florida.

What’s Next for Rates?

At least two of the Four Es will continue to affect freight volume, capacity and rates in 2018. On the demand side, economic growth appears to be accelerating, rather than slowing, with much of the growth happening in sectors that generate more freight. On the capacity side, we have yet to see the full impact of the ELD mandate. More drivers and owner-operators may well choose to quit trucking between now and April 1, when out-of-service penalties kick in for non-compliant truckers.

Two milestones are ahead: the first is in mid-February, which is usually the slowest time of the year for freight transportation. If demand and rates fall at that time, and capacity loosens up, we can expect a return to normal — or the new normal — in time for the spring freight season. If there are repeated, extreme snowstorms or other disruptive events in February, or if there’s atypical, off-season demand, we could be in uncharted territory.

The second milestone is April 1, when the ELD mandate grows serious teeth. It will be the moment of truth for carriers who barely muddled through the first few months, and for those who are didn’t install ELDs yet and are just hoping not to get caught. If a big percentage of drivers and owner-operators exit the industry, it will be difficult to replace the missing capacity. Plus, the drivers who are new to ELDs are expected to be less productive, logging fewer miles per truck, between now and the end of March. Again, this could all sort itself out in a few months, but if not, it’s a whole new ball game.

Stay current on fast-changing rates for 65,000 point-to-point lanes, with DAT RateView, or get rates in your load board, with DAT Power, and DAT TruckersEdge Pro.