In all three modes, the DAT® Trucking Freight Barometers are continuing to demonstrate three basic trends:

- Demand that exceeds capacity by a wide enough margin to drive spot and contract prices higher

- Seasonally weaker demand, as is normal during July and August. There is less freight to be moved. Have no fear. Demand for trucking will pick up again in September and continue to be strong through the end of the year.

- Adapting to ELDs, as all modes show clear signs of improved equipment visibility, better shipper and receiver selection, and more drop and hook. Those factors help to offset some of the lost flexibility and productivity due to ELDs.

As is often the case, all three modes are reflective of the general economy, which is strong, but each mode has a different tale to tell.

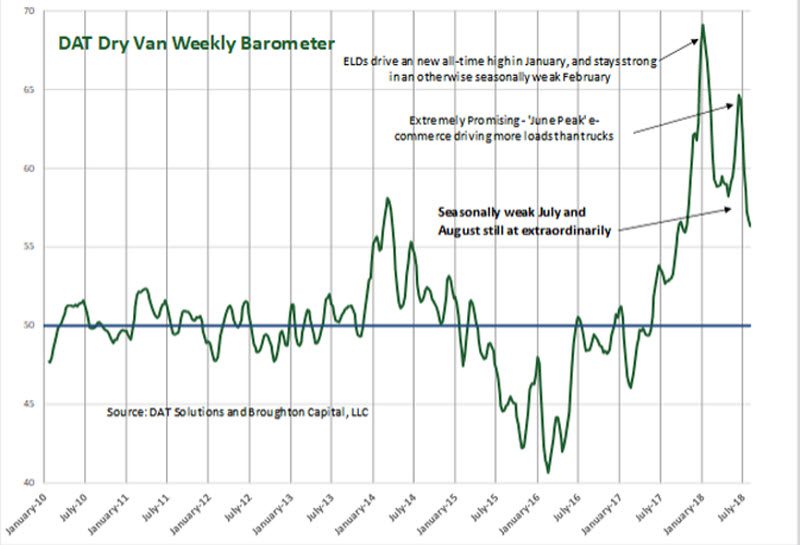

Dry Van – After breaking equilibrium (at 50) sixty weeks ago, the weekly Dry Van Barometer established a succession of ever-higher levels. The current reading of 56.3 is not quite at the extreme levels of capacity tightness experienced in late January and early February (above 65.0), but there are still far more loads than trucks in most lanes in most parts of the country. The Barometer’s high level for this recovery came early in the first quarter of this year, a seasonally weak period for demand. The Barometer began to come down slightly as truckers (mostly small fleets and owner-operators) who had recently adopted ELDs began to optimize their capacity despite the devices. The Dry Van Weekly Barometer continues to predict stronger contract pricing in coming months.

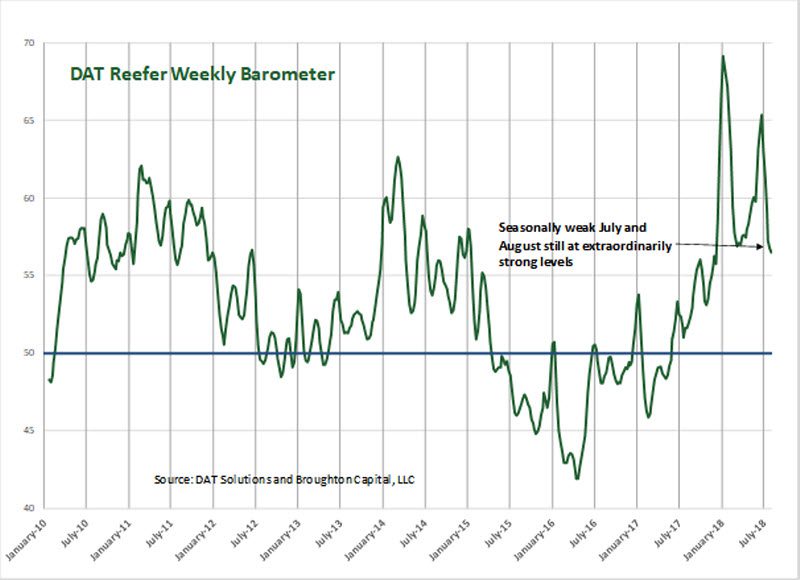

Reefer – At 56.5, the weekly Reefer Barometer is above 50 for the 59th week in a row. As with the dry van segment, the current reading is not at the extreme levels of capacity tightness experienced in late January and early February (above 65.0), but there are still far more loads than trucks in most parts of the country. The latest adoptees of ELDs in the reefer industry are starting to regain some of their lost productivity, but unlike the dry van segment, reefer carriers have fewer choices in managing the use of the trailer. Dry vans are easy to “drop and hook,” but reefer requires some level of driver involvement, and reefer fleets tend to deploy much lower trailer-to-tractor ratios — averaging 1.5 to 1 — than do dry van fleets at 2.5 to 1. Spot rates for reefer will continue to rise and fall seasonally following a June peak, while the current level of DAT Reefer Weekly Barometer is predicting stronger contract pricing in coming months.

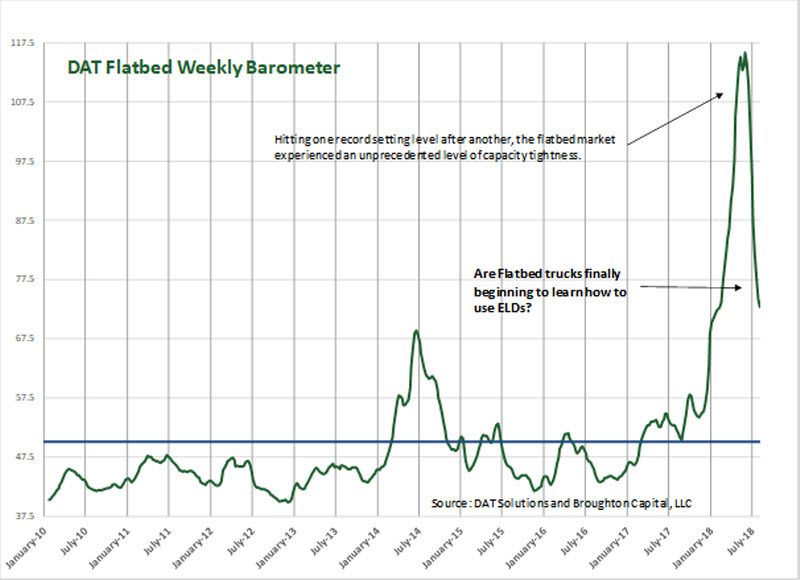

Flatbed – The weekly measure for flatbeds came in at 72.9, pulling back further from a zenith of 115.9 established in the first week of June. The DAT Flatbed Barometer has now been above equilibrium (50) for 72 consecutive weeks. The metric originally broke through 50 in early March of 2017, as crude oil prices rose and remained well above $45 per barrel. Then Hurricanes Harvey and Irma contributed to a strong uptick in building material shipments in 2017, and that strength has been buoyed by an oil price that continues to make fracking profitable in all parts of the U.S. We see the current level of flatbed activity as further evidence that the U.S. industrial economy continues in high gear, but also suggests that flatbed carriers may finally be adapting to the use of ELDs. Contract rates for flatbeds will remain above 2017 levels through the end of this year, but sequential increases will be more moderate.

Donald Broughton, Principal and Managing Partner of Broughton Capital, is a financial analyst with decades of experience in the transportation industry. Contact him at donald@broughtoncapital.com.