The broader freight market is showing more resilience than the headlines suggest. The ATA’s For-Hire Truck Tonnage Index came in unchanged in April following a 1% gain in March — and that flatline is actually good news. As ATA Chief Economist Bob Costello noted, the index has climbed a cumulative 4.7% since the end of 2025 and hasn’t declined once this year, putting tonnage back at levels last seen in the fall of 2022. For flatbed operators who lived through the long freight recession of 2023–2024, that’s a meaningful shift in the baseline.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The year-over-year comparison tells a similar story. April’s seasonally adjusted index registered 117.8 — up 3.5% from April 2025 — and through the first four months of 2026, tonnage is running 2.6% ahead of the same period last year. That matters for flatbed specifically because tonnage gains in this part of the cycle tend to reflect the industrial and construction activity that drives flatbed demand — steel, lumber, building materials, and heavy equipment. A market holding at three-year highs heading into the summer construction season is a supportive backdrop for rates, though DAT spot rate data will tell us whether that demand is actually translating to the floor.

One caveat flatbed carriers should keep in mind: the ATA index is dominated by contract freight rather than spot market activity, so it captures the broad directional trend better than the week-to-week rate swings flatbed operators feel in real time. What the April reading confirms is that the demand foundation isn’t cracking — tonnage is steady at a high watermark, capacity is still under structural pressure from ongoing regulatory headwinds, and the seasonal construction window is open. For carriers running steel, aggregates, or machinery lanes, the macro setup continues to favor disciplined rate holding through mid-summer.

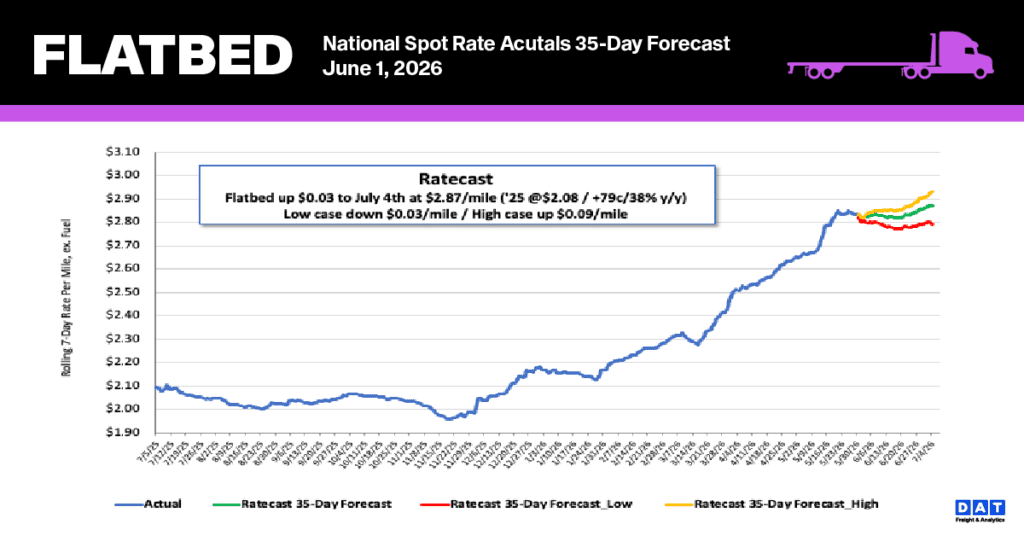

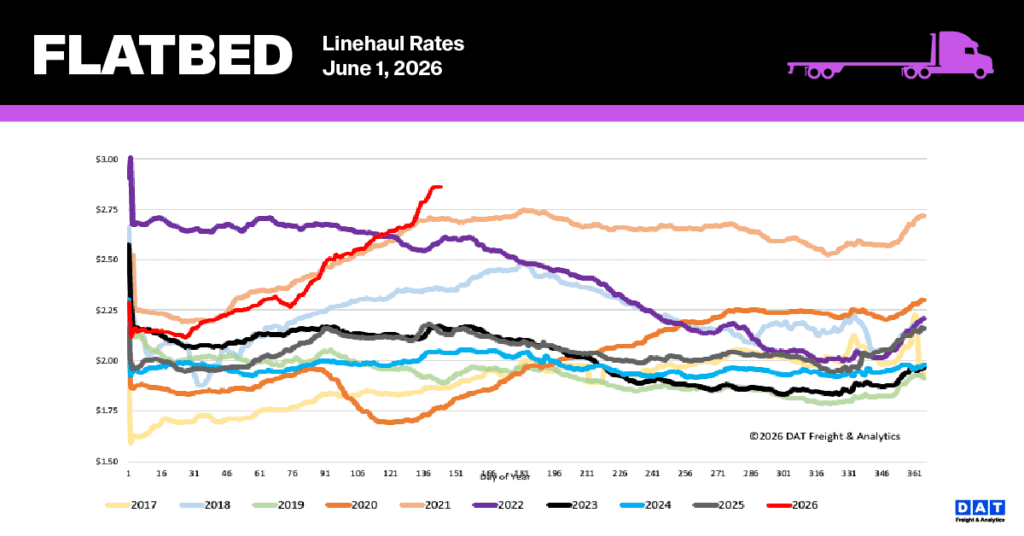

National Flatbed Spot Rate Trends

Driven by persistent capacity constraints, national flatbed spot rates hit a new peak of $2.89 per mile last week, representing a $0.02 week-over-week gain. This record comes after an eleven-week growth streak where rates surged by 21% ($0.58 per mile), eventually exceeding the June 2021 record by $0.14.

Pricing remains exceptionally high relative to historical trends, currently standing 34% ($0.73) above last year’s levels and 30% ($0.88) higher than the five-year average when adjusted for pandemic volatility. These record highs underscore a continuing trend of tightening flatbed capacity within the national 7-day rolling average.

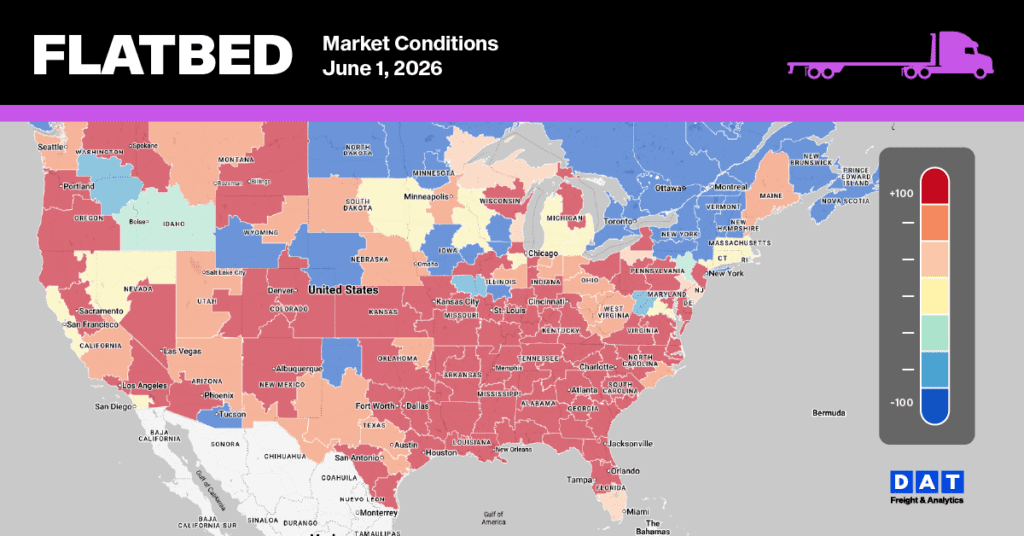

Flatbed Market Conditions

Capacity in the flatbed market continues to be restricted, even with the shortened workweek following Memorial Day. Shifting dynamics in supply and demand caused the flatbed load-to-truck ratio to climb by 12%, ending the week at 76.71. Load postings showed significant growth, rising 83% year-over-year and exceeding the long-term average (which excludes pandemic-impacted years 2021 and 2022) by 50%.