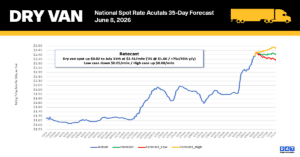

Dry Van Report: Transportation prices just hit an all-time record. The May LMI explains why.

The May LMI recorded Transportation Prices at 96.0 — the highest reading ever posted for any metric in the index’s

The May LMI recorded Transportation Prices at 96.0 — the highest reading ever posted for any metric in the index’s

The produce freight market is quietly unwinding. Florida — the season’s dominant story for weeks — continues its rapid descent,

The April 2026 AEM Farm Equipment Flash report delivered a mixed picture for agricultural machinery demand — and a cautionary

The truckload sector is currently trapped in a tale of two entirely different economies, leaving many carriers dealing with an

The big picture Florida’s Shortage-era rate spike is unwinding — fast. After a two-week surge that sent rates on key

U.S. manufacturing just posted its strongest reading since May 2022. The ISM Manufacturing PMI came in at 54.0% in May

The early forecasts for the 2026 Atlantic hurricane season are pointing toward a near-average or slightly below-average year for storm

The big picture Florida just posted its most dramatic single-week rate swing of the season — and the story isn’t

Freight volumes were essentially unchanged in the first quarter, but what shippers paid to move their goods tells a very

The broader freight market is showing more resilience than the headlines suggest. The ATA’s For-Hire Truck Tonnage Index came in

Data analysis for week of May 28, 2026 for truckload produce shipper, carriers, and brokers The big picture The produce

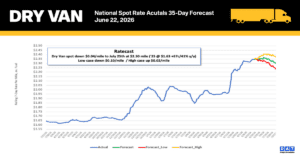

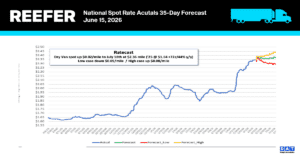

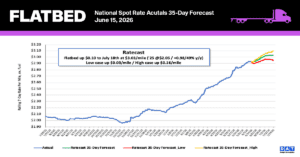

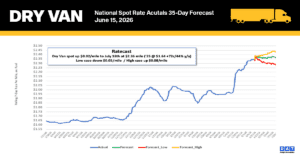

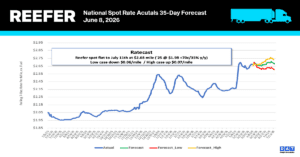

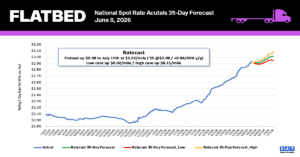

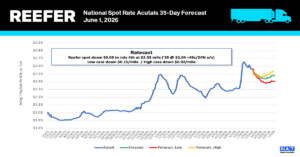

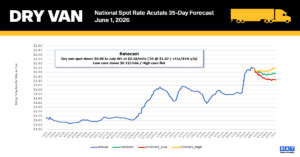

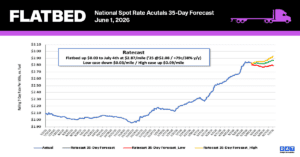

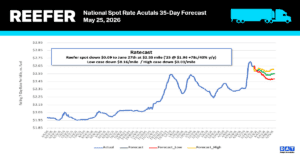

All rates cited below exclude fuel surcharges, and load volume refers to loads moved unless otherwise noted. The rate charts