Last week, COVID-19 hotspots erupted both across the country and world, in places that had been declared COVID-free, such as New Zealand, Australia and China.

While businesses and factories remained open, Beijing barred non-essential travel and cancelled thousands of flights. New cases in the U.S. also prompted China to suspend imports of poultry, which will have an impact on freight.

Clearly, very few in the U.S. have an appetite for more shutdowns. As we find ourselves searching for some sort of “new normal,” we’re seeing the reopening process slow in places where new hotspots emerge, but surprisingly, we saw major upticks in dry van loads.

Get access to the most loads and trucks on the DAT One load board network.

Supply and Demand Trends

Dry Van: From a truckload demand perspective, consumers will play a key role in leading the country out of this recession, but unlike in 2009, the fear of catching COVID-19 means most will only shop where they feel safe. This will continue to disrupt traditional supply chains, origin-destination pairings and lane density as more consumers opt to purchase goods online and/or shop at stores where safe protocols are in place.

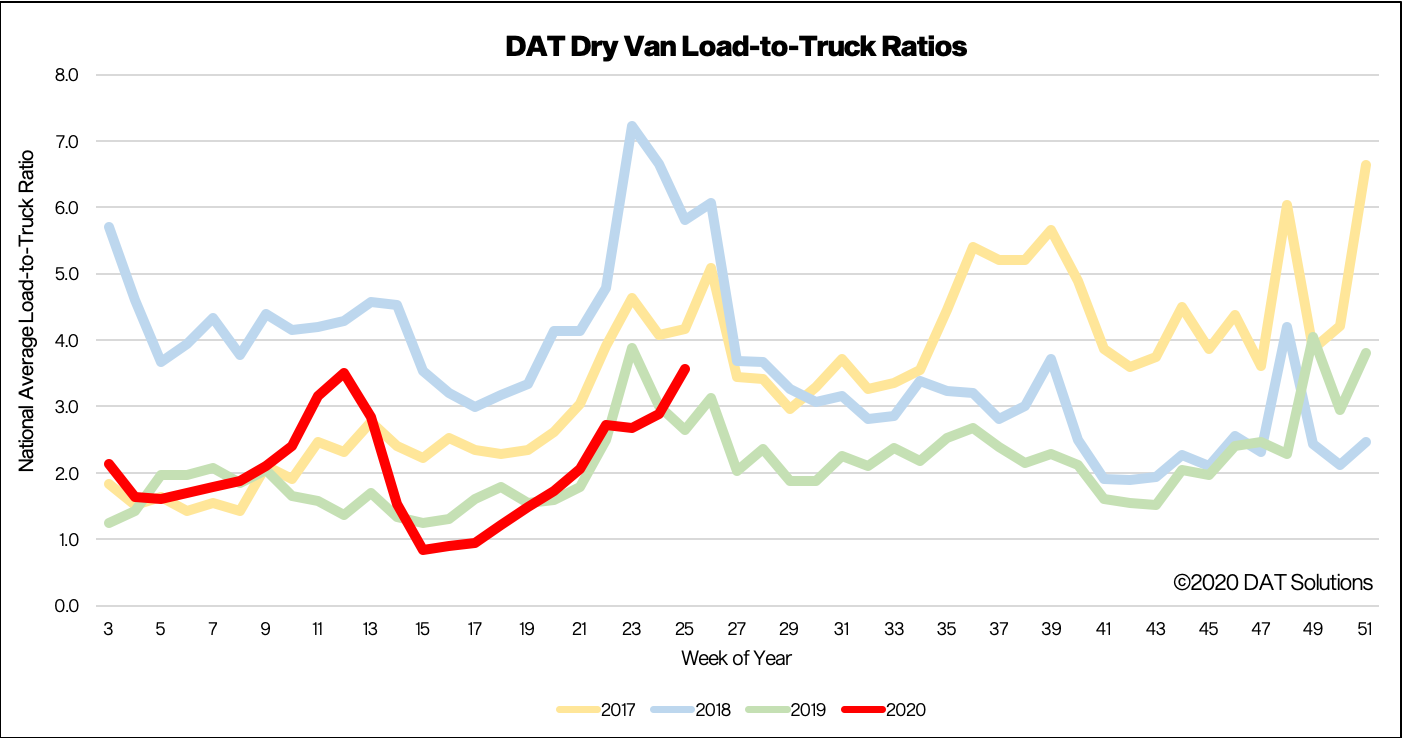

Ahead of July 4, we’ve seen an increase in the dry van Load-To-Truck Ratio (LTR) by 24% to 3.56 last week, driven by a 20% week-over-week increase in spot market load posts, which also puts dry van load volumes up by about the same amount year over year. Capacity tightened as a result, with truck searches down 3% w/w and 8% y/y.

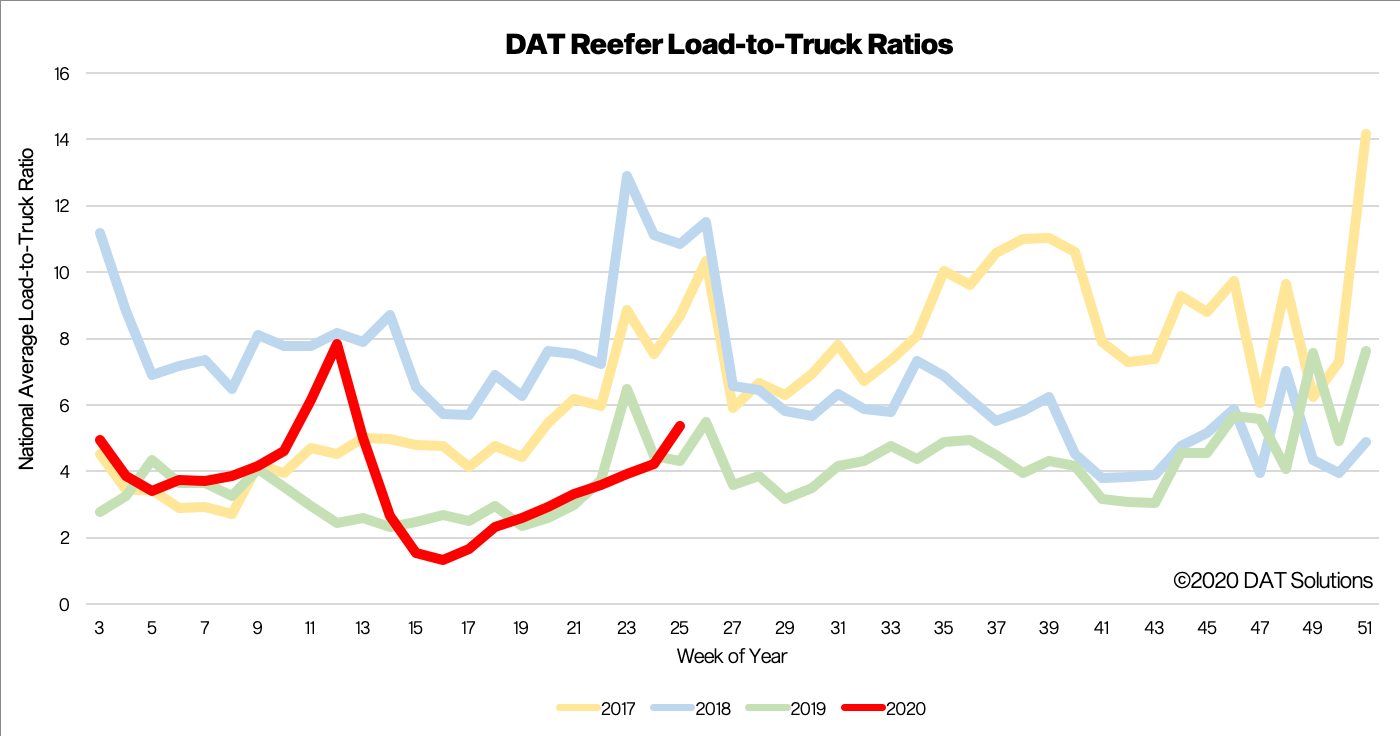

Reefer: A 21% increase in reefer load posts last week drove up the LTR by 27% w/w and 19% y/y to 5.35, with capacity tightening resulting in 5% fewer trucks searching for reefer loads w/w.

Market Conditions Index (MCI)

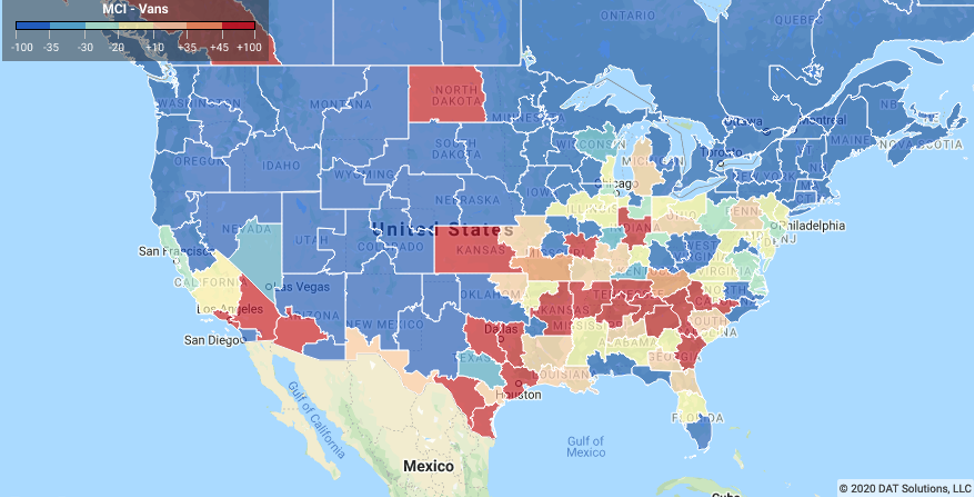

Dry Vans: Volumes remain elevated in states that have reopened, driving up demand for consumer packaged goods. After two months of successive declines, the U.S. Census Bureau reported that May retail sales data increased by close to 17%. Federal stimulus checks, higher unemployment benefits and pent-up demand led consumers on a burst of spending, which has contributed to the 20% increase in dry van volumes this week.

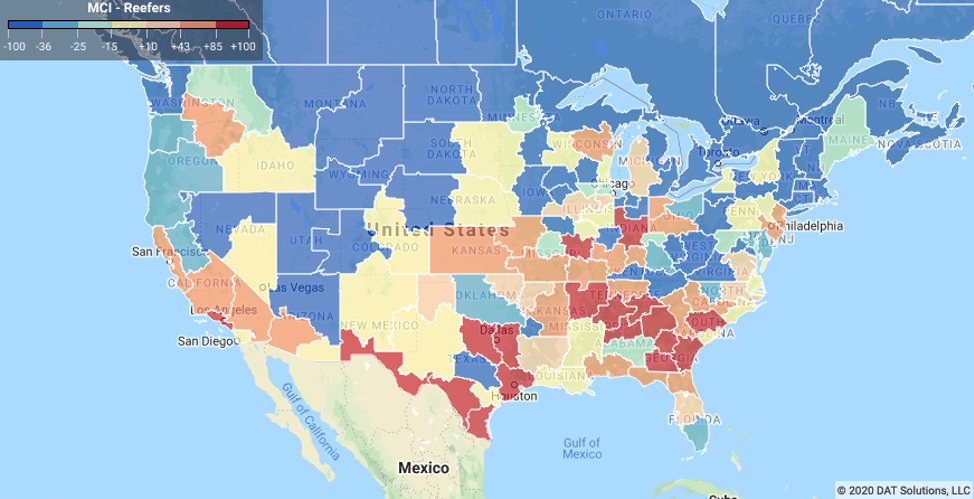

Reefers: Atlantic coast markets including Philadelphia are heating up, as South African navel oranges and clementines arrive by sea for regional distribution (around 200 truckloads per vessel). In the last seven days, the Philadelphia market has posted 10,720 reefer loads with 58% of those loads moving within a 500-mile radius – or a day’s drive – by truck. The top five destinations (Hartford, CT; Boston, Pittsburgh, Harrisburg, PA; and Chicago) accounted for 23% of loads outbound in the last week.

June is also the peak for produce shipments and widely considered “berry season,” with higher volumes of strawberries, blueberries, raspberries and blackberries being shipped out of Georgia, North Carolina, California, Oregon, Washington, British Columbia, Michigan, Texas, Ohio and New Jersey freight markets.

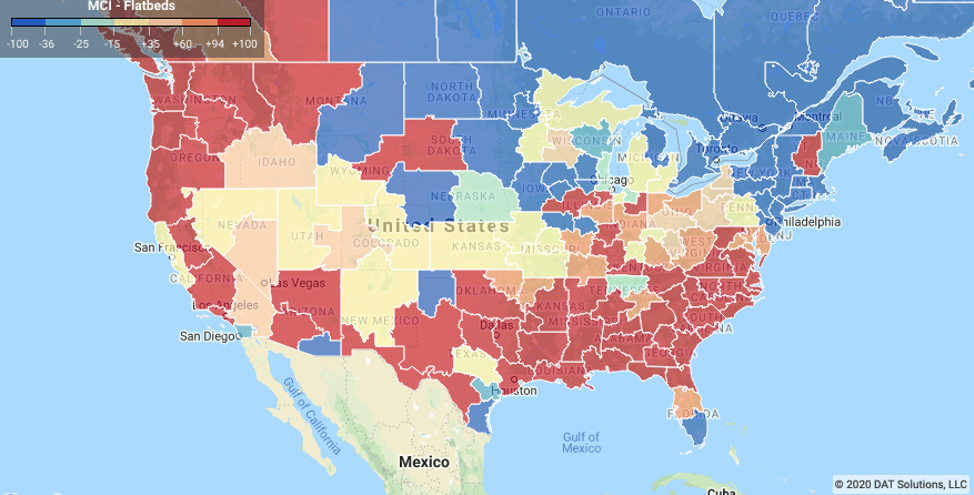

Flatbeds: We’re seeing mixed signals, as East Coast port markets report U.S. machinery imports down by 14% compared to the first five months of 2019, according to IHS Markit. The Port of Baltimore, which is a major construction and agriculture machinery freight market for specialized equipment, has cooled considerably, along with machinery imports being down 18.5% m/m in May and 35% y/y.

There’s better news for flatbed carriers in the home building sector, where the National Association of Home Builders (NAHB) reported that their Housing Market Index jumped up by 21 points in May, the largest ever monthly increase. According to the NAHB, builders are reporting higher demand for families seeking single-family high-tech homes in inner and outer suburbs more suited to the new work-from-home economy. These homes are generally considered “freight intensive,” as they use the widest range of materials to construct.

> Learn more about the Market Conditions Index.

Rate trends

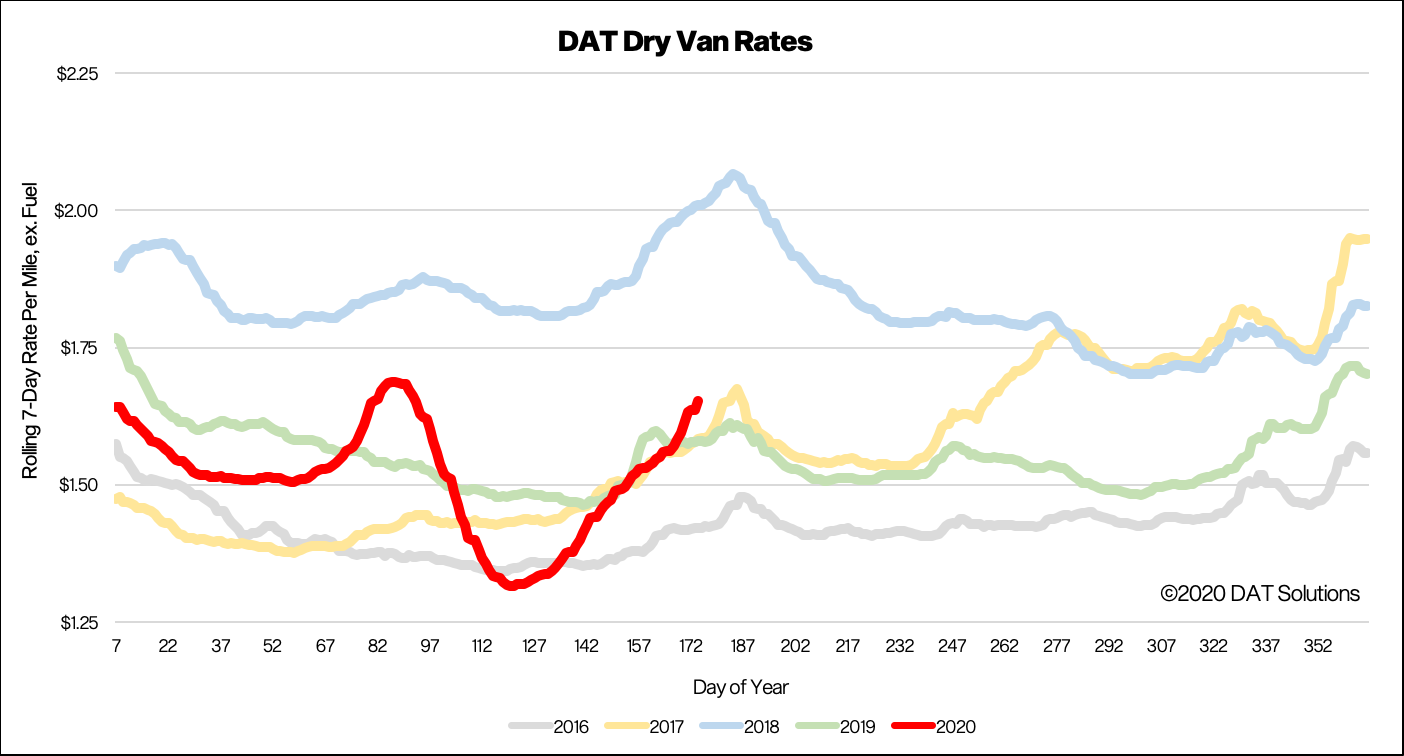

Dry van spot rates are tracking more closely to 2017 after increasing 1% w/w and 4.4% y/y to a national average of $1.65/mile, excluding fuel surcharges. We’re still expecting dry van rates to continue their upward trend right through July 4, and as we suggested last week, we expect capacity to remain in the market this year to make up for lost revenue in Q1 rather than take time off over the holiday break.

If this occurs, then we expect rates to cool off quite quickly next week, which is where the Ratecast model predicts rates will head after peaking a few pennies higher at $1.67/mile, excluding fuel.

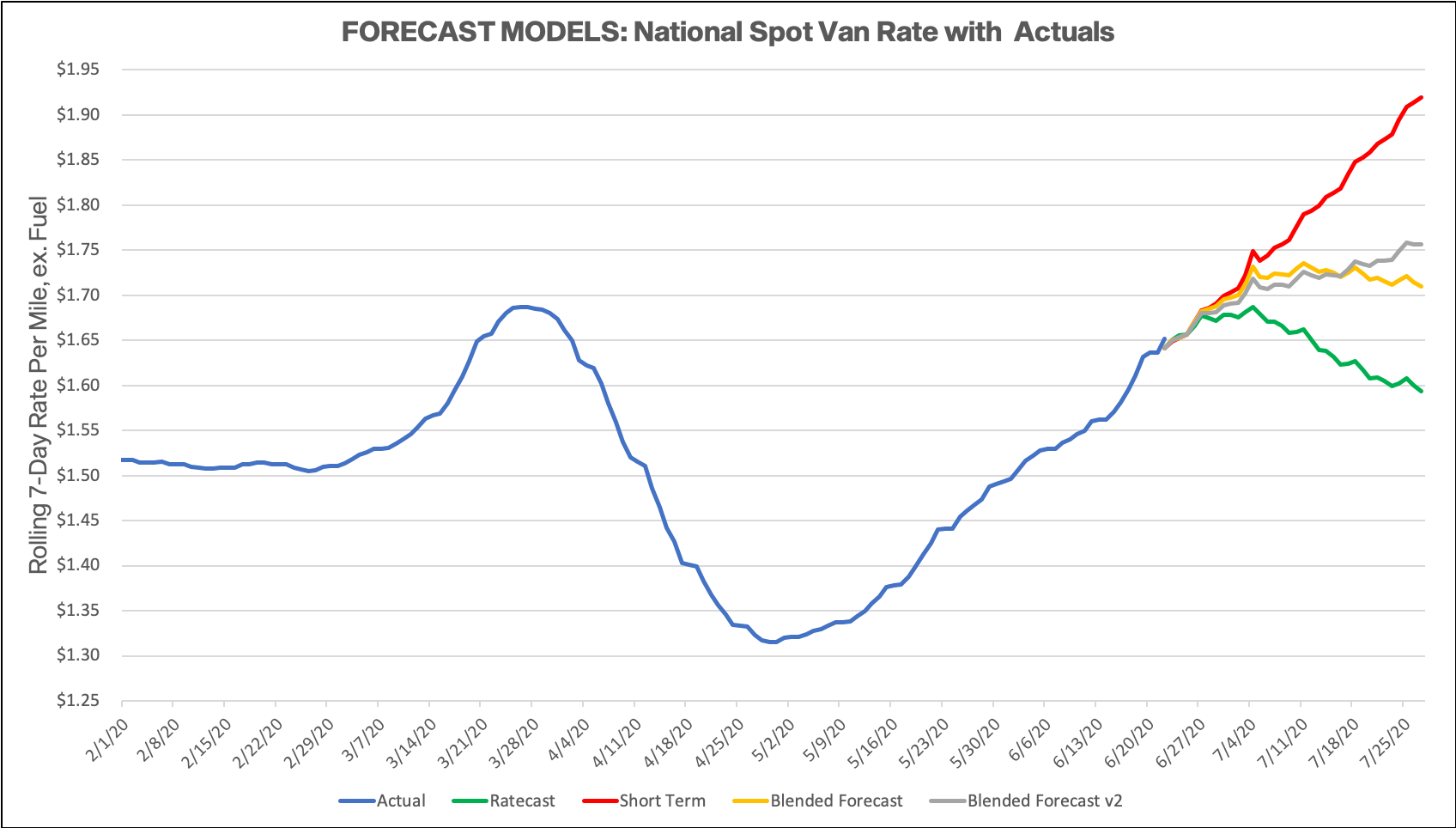

Note: It warrants mentioning that forecasting during this volatile and uncertain time period is difficult. Our team is working diligently to update and adjust the models, but new information becomes available at a rapid pace, which further complicates the issue. DAT would typically not publish these types of preliminary studies, but we feel that the benefit of sharing our observations far outweighs the risk. We ask that you please treat these statements and exhibits as directional and consider them as a variable in your own analyses.

How to interpret the rate forecast

1. Ratecast Prediction: DAT’s core forecasting model estimate showing continued optimism and rate growth.

2. Short Term Scenario: Formerly the pessimistic model that focuses on a more near-term historical dataset.

3. Blended Scenario: More heavily weighted towards the longer-term models.

4. Blended Scenario v2: More heavily weighted towards the shorter-term models.

> Learn more about Ratecast predictions available in RateView.

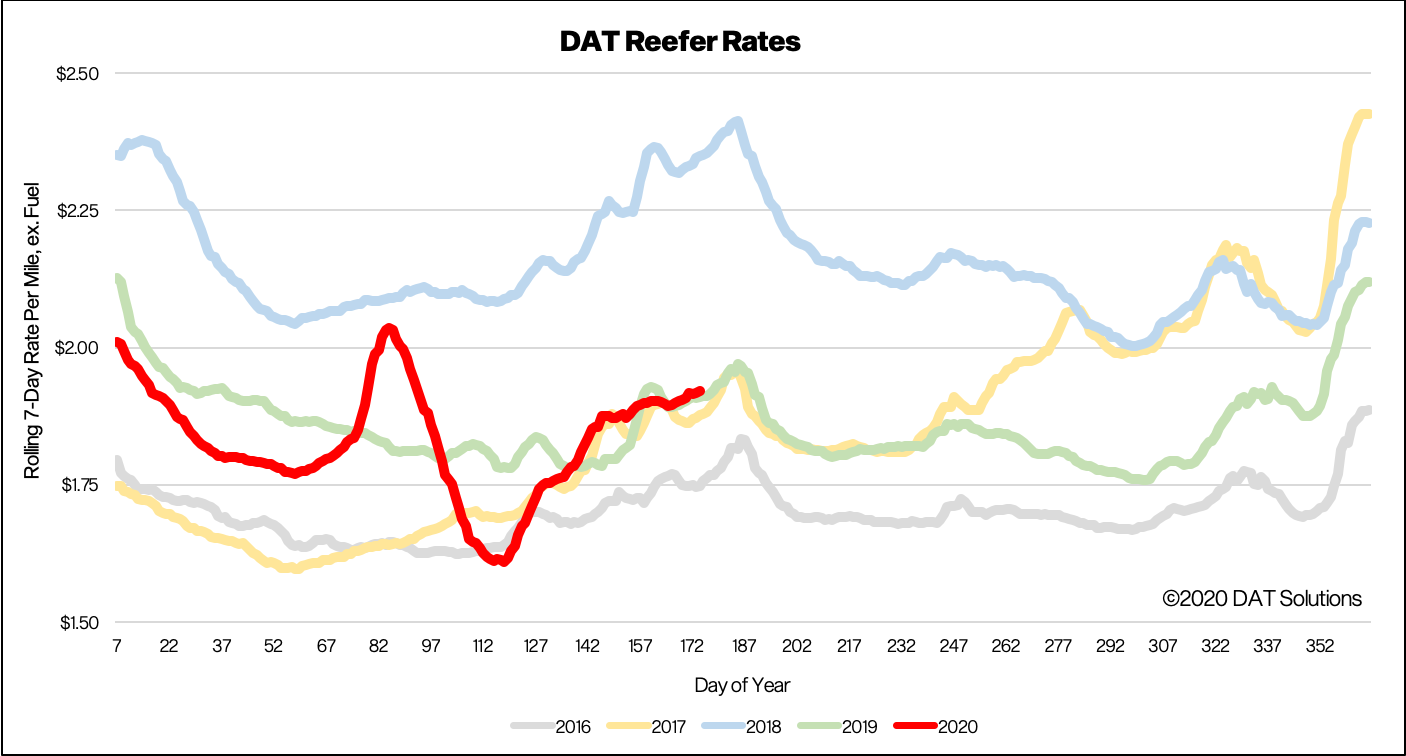

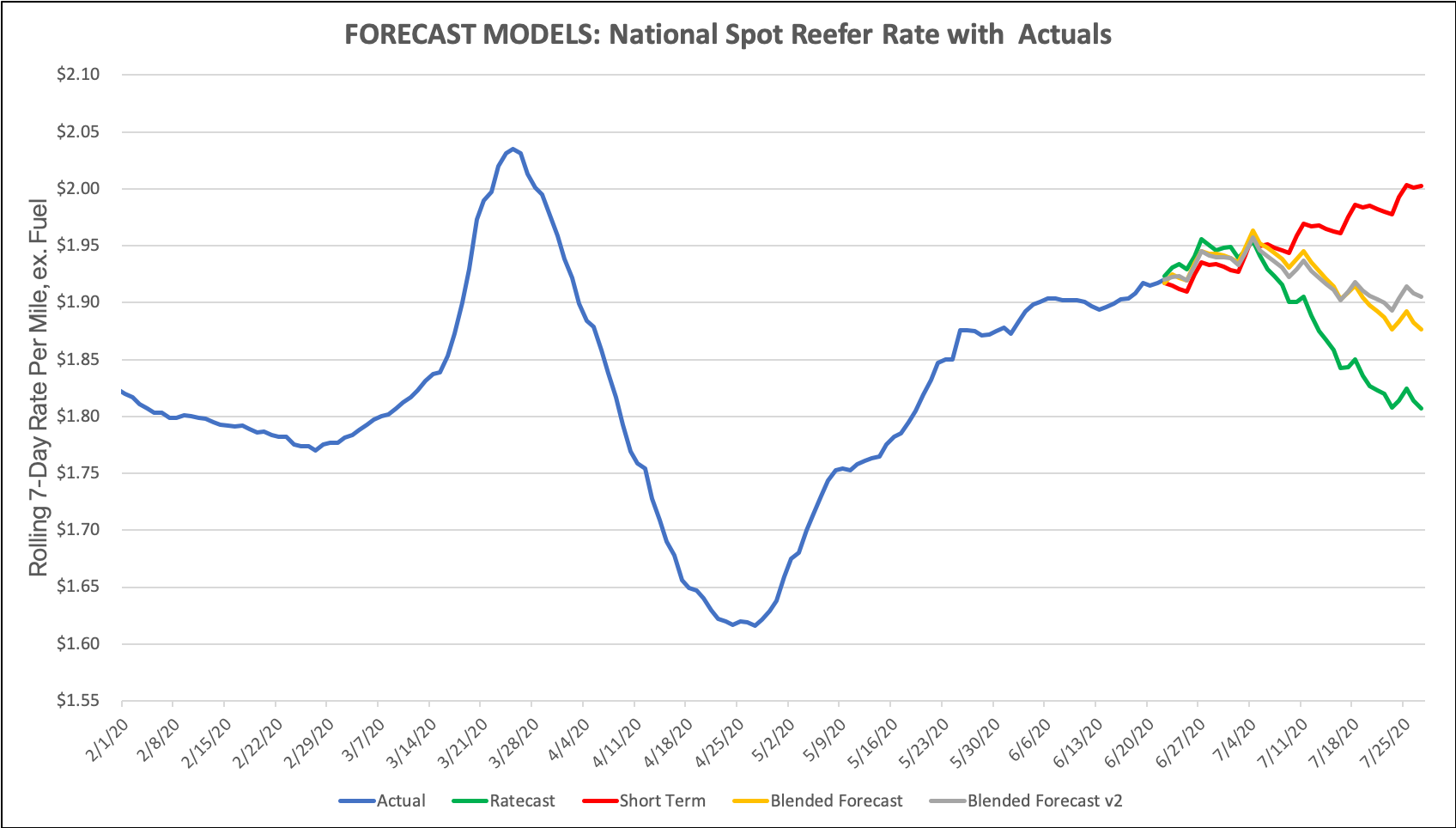

National average reefer rates moved up by close to 1% last week to $1.92/mile excluding fuel, with a 21% w/w surge in spot market load posts. Rates are now tracking very closely to 2017 and 2019 on both the 7-day and 3-day rolling average data views.

Reefer rates typically retreat after July 4th, with our Ratecast model predicting that linehaul rates will peak at $1.95/mile before dropping off quickly. The big unknown this year is whether consumer demand for perishable goods will be sufficient to keep reefer carriers busy. If this week’s COVID-19 outbreaks in Florida, Texas and Arizona derail the economy’s reopening, consumer demand may take another hit and put reefer rates in the 2016 range rather than the healthier rates in 2017 and 2019.

Produce season drives a lot of reefer volume this time of the year, with domestic truckloads of fruit and vegetables up 3% according to the USDA this week. This increase contributed to the higher spot rates last week, with truck capacity tight in Central and South Florida and South Carolina. Domestic shipments increased by 753 loads last week, but imported produce shipments dropped by 11%, or 1,768 fewer truckloads, for a combined drop in national fruit and vegetables truckloads of 1,005 last week.

Note: It warrants mentioning that forecasting during this volatile and uncertain time period is difficult. Our team is working diligently to update and adjust the models, but new information becomes available at a rapid pace, which further complicates the issue. DAT would typically not publish these types of preliminary studies, but we feel that the benefit of sharing our observations far outweighs the risk. We ask that you please treat these statements and exhibits as directional and consider them as a variable in your own analyses.

How to interpret the rate forecast

1. Ratecast Prediction: DAT’s core forecasting model estimate showing continued optimism and rate growth.

2. Short Term Scenario: Formerly the pessimistic model that focuses on a more near-term historical dataset.

3. Blended Scenario: More heavily weighted towards the longer-term models.

4. Blended Scenario v2: More heavily weighted towards the shorter-term models.

> Learn more about Ratecast predictions available in RateView.

Need more information?

Our update will be refreshed next week, or sooner if conditions change materially. Visit dat.com/blog for the latest information. Any questions about this report or market conditions can be emailed to askIQ@dat.com.

We are also making available, free of charge, the DAT iQ Daily 50, which is a daily report of the top 50 lanes by volume with a week’s worth of history and predictions using the Ratecast model. Request access at askiq@dat.com.