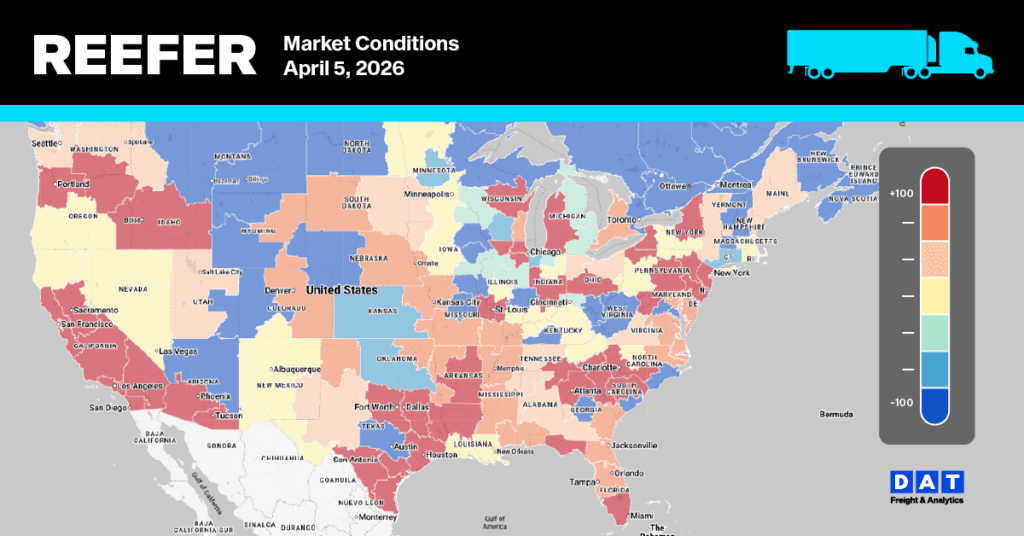

Vidalia Onion pack date has been announced for April 13, marking the official starting line of the 2026 produce season and the spring produce squeeze is on — and it’s hitting everywhere at once. Nogales posted its first Shortage lane of 2026 (Chicago), California’s four-week flatline shattered with every region shifting to Slight Shortage and rates jumping as much as +17%, Florida reversed with double-digit gains after three weeks of range-bound trading, and South Texas held its elevated levels for a third straight week of full Slight Shortage.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The only origins not tightening are Colorado potatoes and New York apples. With the Yuma-to-Salinas lettuce transition now imminent, expanded commodity mixes signaling the spring season is fully underway, and diesel hovering above $5.00/gallon adding cost pressure on every mile, this is the tightest produce freight environment of 2026 — and it’s accelerating.

Nogales is now the tightest origin in the country. For the first time in our 2026 tracking, a Nogales lane has hit full Shortage — Chicago at $5,900–$6,200 (+4%). The remaining seven lanes are all at Slight Shortage, with Boston cracking $10,000 for good ($10,000–$10,600, +4%) and LA surging +21% to $2,200–$2,400. Loads include green beans, sweet corn, cucumbers, eggplant, honeydews, bell peppers, squash (acorn, butternut, grey, kabocha, spaghetti, yellow straightneck, zucchini), tomatoes (round, grape, plum), and watermelons. Every lane posted gains this week:

California’s four-week produce flatline is over. Every California region shifted to Slight Shortage this week — a significant move from Adequate — and rates broke higher across the board. The biggest movers were Oxnard District (celery, cilantro, greens, kale, parsley, strawberries), where Baltimore jumped +17% to $8,600–$9,600 and Philadelphia surged +16% to $8,600–$9,800. Imperial/Coachella and Santa Maria reset to new rate baselines without week-over-week comparisons, suggesting a structural step-up. Note the expanded commodity mix out of Imperial/Coachella — blackberries, blueberries, and bok choy are now listed alongside the usual lettuce, broccoli, and leafy greens. South/Central District produce also reset with an expanded mix that now includes avocados, artichokes, and radishes. Key California lanes:

Note: California citrus lanes are absent from this week’s report. Last week, South/Central CA citrus (blood oranges, grapefruit, lemons, oranges, tangelos) was at full Shortage on all nine destinations. This week, citrus appears to have been folded into the broader South/Central produce commodity listing (grapefruit and lemons are now listed alongside leafy greens and avocados). The separate citrus rate table is gone — likely reflecting the winding down of the citrus season.

Florida reversed hard. After three weeks of range-bound trading, Central and South Florida posted its biggest single-week gains since the February spike. Rates jumped +7% to +18% across all six destinations on loads of beans, broccoli, cabbage, celery, sweet corn, endive, escarole, lettuce, okra, bell peppers, other peppers, radishes, squash (yellow crookneck, zucchini), strawberries, and tomatoes (round, cherry, grape, plum). Truck availability is mixed — Adequate on Atlanta and Chicago, Slight Shortage on the other four.

South Texas remains fully locked up — all nine lanes at Slight Shortage for the third consecutive week on asparagus, broccoli, carrots, cucumbers, peppers (anaheim, bell, habanero, jalapeno, poblano, serrano), tomatoes, watermelons, and other Mexican imports. Rate moves were modest this week (+1% on most lanes, flat on others), suggesting South Texas may be finding a ceiling after five weeks of compounding gains. Outbound McAllen reefer linehaul rates seem to have peaked in the $3.15/mile to $3.25/mile range since early February, but are still 26% higher than this time last year.

Yakima Valley (apples & pears) held completely flat on all ten lanes for the second week, with every lane at Slight Shortage – Pendleton freight market reefer linehaul rates are 14% higher y/y. Colorado potatoes and New York apples remain Adequate and unchanged.

The full weekly wrap can be found here.

National reefer linehaul spot rates

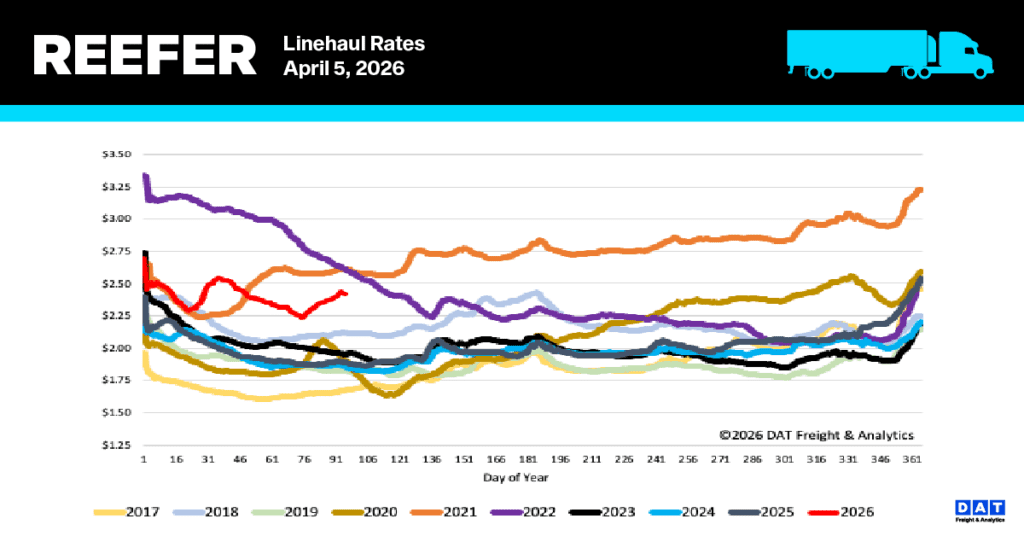

Reefer linehaul rates have climbed to an average of $2.43 per mile, a $0.05 per mile increase, as carriers successfully recover a greater share of the rising fuel surcharge. This rate marks a substantial rise compared to previous years. Specifically, it is $0.53 per mile (28%) higher than the rate for the same period last year. Furthermore, it is $0.56 per mile (23%) above the five-year average, excluding the unusual peak rates observed in 2021 and 2022.

Reefer Market Conditions

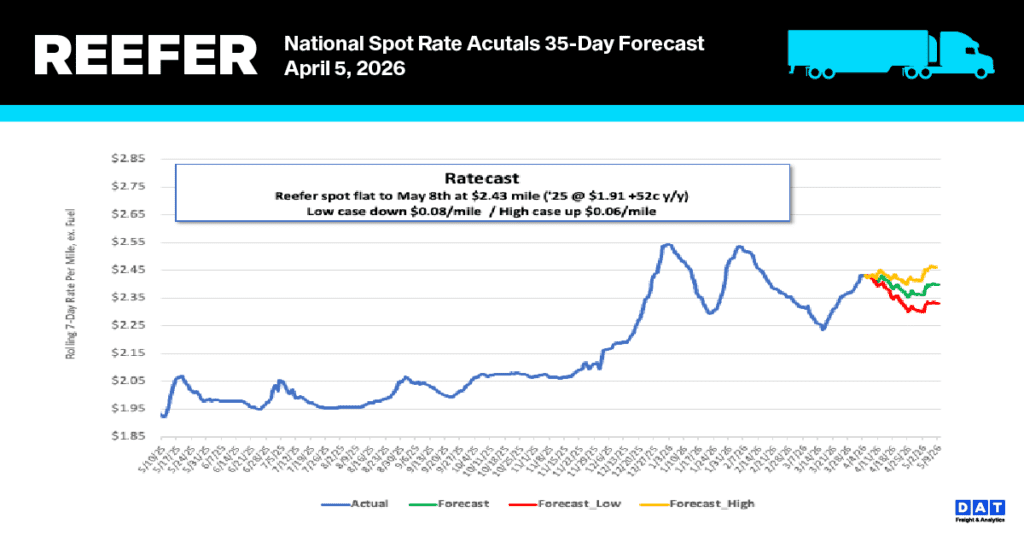

The reefer load-to-truck ratio decreased last week, falling 11% to 16.92. Despite this weekly drop, the ratio is still over 73% higher than the same time last year. This change was due to a 15% decline in load post volumes, which outpaced the 4% decrease in equipment post volumes.