The agriculture equipment sector hasn’t found its floor yet. According to the Association of Equipment Manufacturers’ February 2026 report, total farm tractor retail sales fell 12.2% year-over-year for the month, with the steepest declines hitting the large-horsepower segment hardest — 100+ HP 2WD tractors dropped 25.8% in February and are down 25.9% on a year-to-date basis. That matters for flatbed carriers because large ag equipment — combines, row crop tractors, tillage implements — represents some of the highest-value, highest-cube loads in the segment. Self-propelled combine sales also declined 12.6% in February, extending a soft stretch heading into what should be pre-season restocking territory.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

For flatbed demand, the read-through is straightforward: fewer equipment sales mean fewer shipments moving from OEM plants and dealer distribution centers to farms. Beginning inventory for 2WD farm tractors stood at over 90,000 units at the end of February, signaling that dealers are still working through elevated stock rather than pulling fresh orders. Until that inventory normalizes, the freight pull from ag equipment manufacturing is likely to remain muted. Carriers running Midwest equipment corridors — Indiana, Illinois, Iowa — should expect continued softness in this freight vertical through at least mid-2026 barring a meaningful shift in farm income or commodity prices.

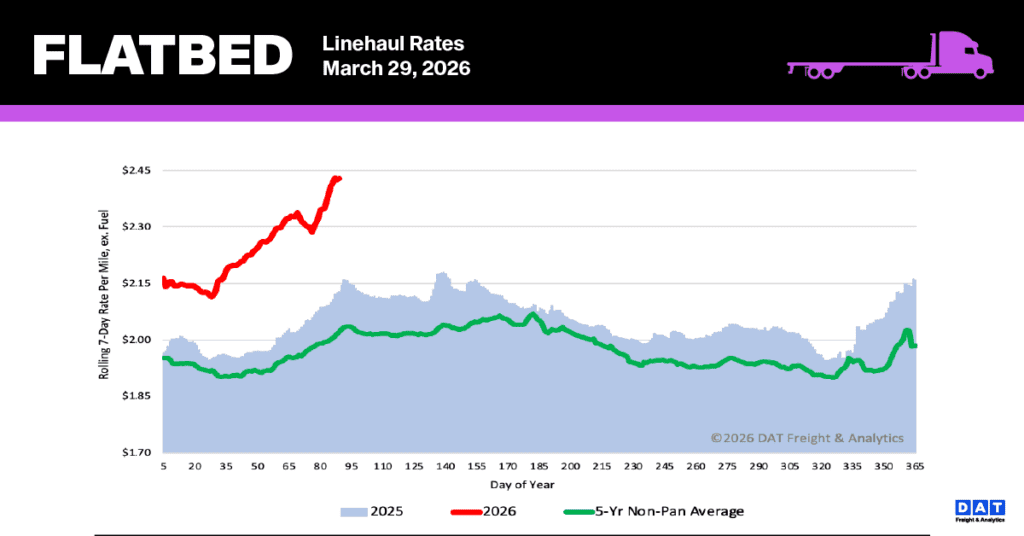

National flatbed linehaul spot rates

The national average spot rate for flatbed linehaul saw a significant increase last week, jumping $0.09 to reach $2.44 per mile. This current rate is notably higher than in previous years: it is $0.30 (14%) above the rate from the same time last year and exceeds the five-year average (when excluding pandemic years) by $0.42 (17%).

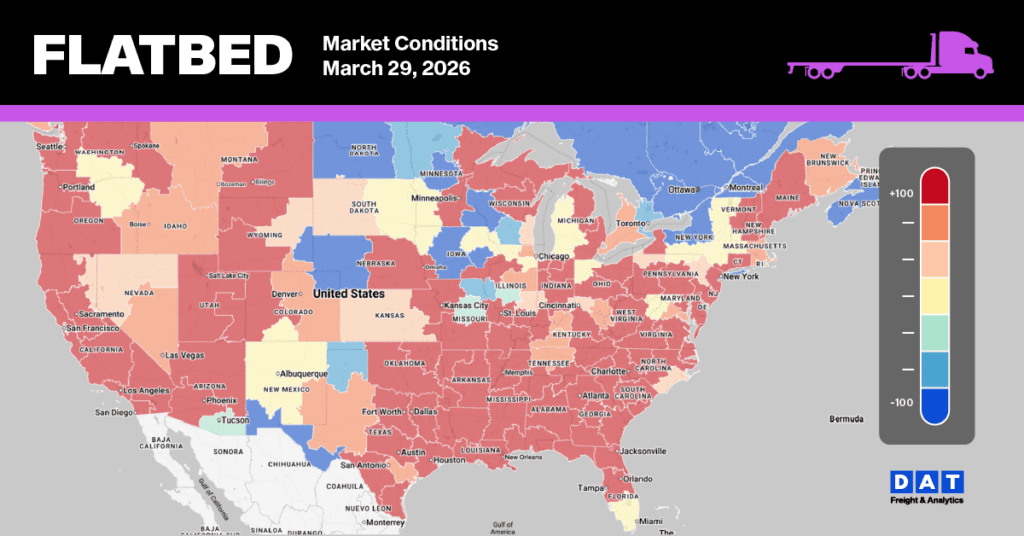

Flatbed Market Conditions

The flatbed market tightened significantly last week, with the load-to-truck ratio rising 10% to 83.75. This surge was due to a 3% week-over-week increase in flatbed load posts, reaching the highest weekly volume for Week 13 in four years. Flatbed equipment posts, however, remained unchanged last week.