Data analysis for week of May 28, 2026 for truckload produce shipper, carriers, and brokers

The big picture

The produce reefer market just snapped back — hard. After last week’s dramatic rate surge across California growing districts (Salinas to New York up +36%, Santa Maria to New York up +66%, South Texas to Baltimore up +27%), this week delivered a near-universal correction. South Texas — which was the hottest origin in the country just seven days ago under Shortage conditions — flipped to Adequate truck supply and saw rates crater by 21%–41% depending on destination. Nogales also softened, dropping from Slight Shortage to Adequate, with rates off 3%–20%. California’s leafy green corridors (Salinas, Santa Maria, South/Central) held flat after last week’s spike, suggesting those elevated rates may be finding a new floor rather than collapsing. Florida remains the structural weak spot — still rated Shortage, and while rates are mixed week-over-week, the season is winding down fast. Yakima Valley stabilized after prior-week gains, moving from Adequate to Slight Shortage with flat rates. The week’s defining story: a two-week whipsaw in South Texas that gave and then largely took back a surge in reefer rates from a key border crossing.

1. South Texas — The week’s biggest story

Last week’s Shortage conditions reversed sharply as truck availability normalized. Rates fell across the board — some lanes by more than 40%. Two-week arc: The Dallas lane went from ~$3,900 (May 12) → ~$4,000 (May 19, Shortage) → $2,500 (May 26, Adequate) — a round-trip spike and collapse in 14 days. The cumulative net move is essentially flat, but carriers who covered last week locked in peak rates while this week’s loads are back near multi-month lows.

2. Nogales, Arizona — Softening After Prior Tightness

3. California leafy greens — Flat after last week’s surge

The California districts that saw 25%–66% rate spikes last week are now flat across the board — a consolidation at elevated levels rather than a reversal. This is the pattern to watch: do these rates hold, or do they follow South Texas lower?

- Salinas-Watsonville — Flat after 26%–36% spike last week

- Santa Maria — Flat (most lanes)

- South & Central District California — Partial pullback

4. Kern District, California — Carrots pulling back on key lanes

5. Oxnard District, California — Flat

6. Central & South Florida — Season winding down, rates mixed

Florida’s Shortage rating persists but the load pool is clearly shrinking. Florida → Baltimore dropped from $4,500–$4,700 last week to $3,400–$3,600 — a $1,100 decline in one week, continuing the structural unwind as the South Florida season winds toward its end. The short Atlanta haul ($1,700–$1,900) remains the lowest-rate lane in the entire report.

7. Vidalia District, Georgia — Flat and adequate

8. Yakima Valley & Wenatchee, Washington — Tightening

Truck availability tightened this week (from Adequate to Slight Shortage) but rates held flat across all lanes. Worth watching — availability tightening without rate movement often precedes rate increases in following weeks.

What This Means for Carriers, Shippers & Brokers

For reefer carriers

South Texas’ collapse is the warning signal of this week. The Shortage-to-Adequate flip in one week — with rates down 25–40% — illustrates the volatility of border crossings when immigration enforcement actions, weather, or volume shifts alter the supply/demand balance overnight. Rethink positioning equipment to South Texas based on last week’s rates. The Yakima availability tightening (Adequate → Slight Shortage, flat rates) is a setup worth watching for next week — that’s a classic leading indicator before rates move. California leafy green lanes are holding at elevated post-spike levels; these could be defensible if the Salinas transition volume ramps in the coming weeks. Florida is in structural wind-down although watermelons are solid this week.

For shippers

California origin shippers locked in last week’s elevated rates are sitting well — the flat-to-modest pullback this week means the California corridor has found a new (higher) floor. South Texas shippers who held out from last week’s spike are rewarded with rates 25–40% cheaper this week. Florida shippers: the Baltimore lane drop ($1,100 in one week) reflects a shrinking load pool; contract coverage on remaining Florida volume becomes more important as spot availability grows. Vidalia shippers have stable, predictable rates — take advantage while adequate truck supply persists.

For brokers

The South Texas whipsaw is a margin management story this week. Brokers who covered last week at Shortage rates are now carrying loads at above-market cost against a softened spot market — verify your exposure on any open positions from last week. The Yakima Slight Shortage flag (no rate move yet) is where to pre-position coverage: the pattern of tightening supply ahead of rate movement gives you a narrow window to lock in capacity before rates follow availability. Watch the California leafy green corridors for direction — if Salinas/Santa Maria rates hold flat another week, that’s a stabilized market; if they follow Nogales and South Texas lower, California rates have further to fall.

National reefer spot rate trends

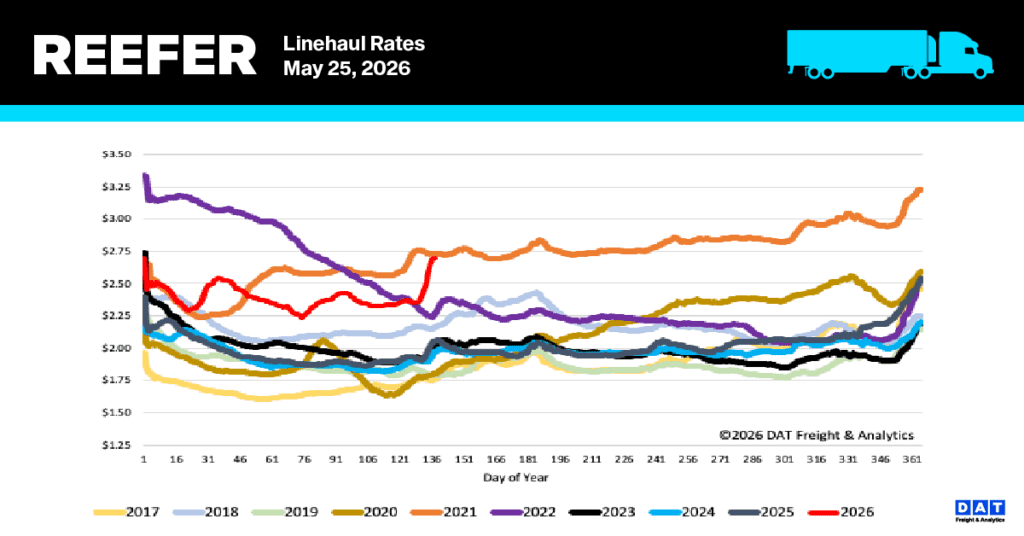

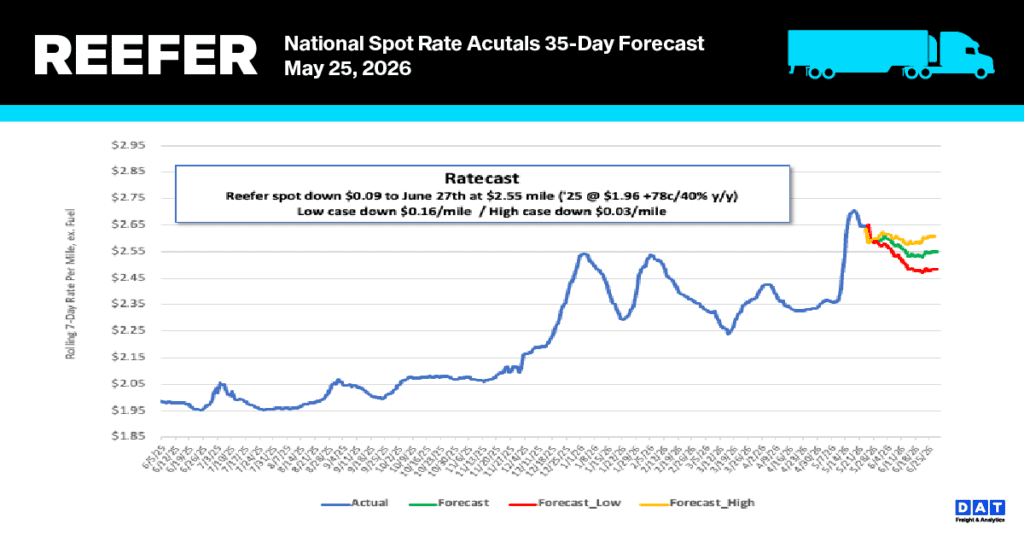

Market capacity eased slightly last week following a record $0.32 per mile spike during Roadcheck Week. The 7-day national rolling average for refrigerated linehaul rates adjusted downward by $0.03, settling at $2.65 per mile. Despite this minor softening, reefer spot rates remain at historic levels across all temperature ranges and products, excluding fuel surcharges. Current performance is significantly elevated compared to historical norms, tracking 32% ($0.65) above last year’s figures and 27% ($0.71) higher than the non-pandemic five-year average.

Reefer spot rates for fruit and vegetable transport in major produce hubs currently average $4.16 per mile. This reflects a notable week-over-week increase of roughly $0.17 per mile and stands $0.67 above the rates from the same time last year. These levels have not been seen in nearly four years, since the market began retreating from the record highs triggered by pandemic-era disruptions.

According to USDA data, produce volumes have seen a consistent four-week rise, including an 11% increase last week that positioned volumes 9% higher than the previous year. As truckload capacity continues to tighten, the produce sector has maintained a slight shortage (4) for the second consecutive week.

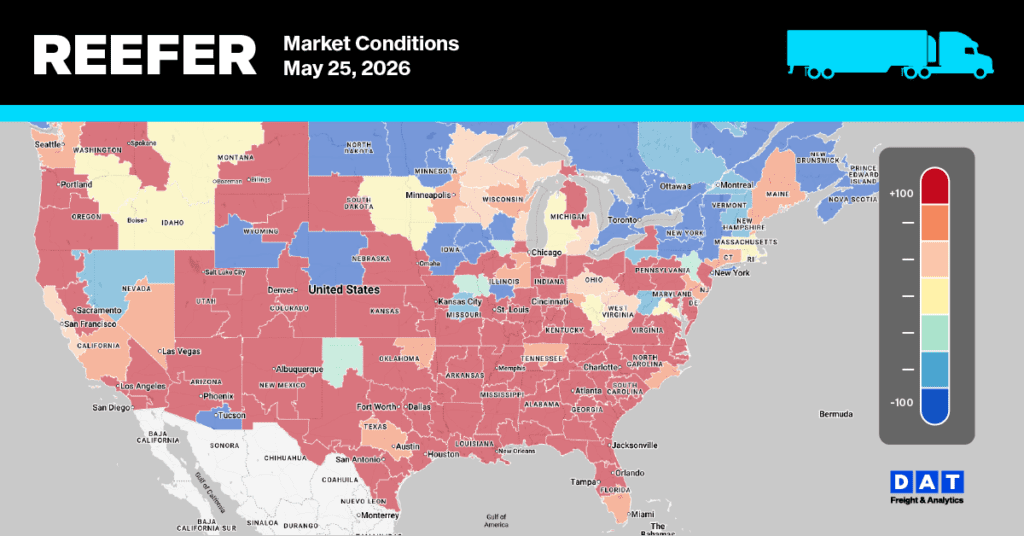

Reefer Market Conditions

Reefer capacity largely stabilized in the wake of the Roadcheck Week safety blitz. After a slight 1% dip in equipment posts last week, availability is now just 4% shy of pre-Roadcheck levels. As supply constraints eased, the load-to-truck ratio fell by 14% to 22.94. Despite a 13% weekly decline in load post volumes, demand remains 74% higher than the previous year. Conversely, equipment posts have dropped 26% year-over-year, reinforcing a tight reefer market as the industry approaches the July 4 seasonal peak.