U.S. manufacturing just posted its strongest reading since May 2022. The ISM Manufacturing PMI came in at 54.0% in May — up 1.3 points from April and its highest level in four years, marking the fifth consecutive month of expansion. For trucking, this is a demand signal worth watching: when factories are buying more, making more, and building backlogs, freight follows. New Orders surged to 56.8%, Production held at 54.3%, and the Backlog of Orders index ticked up another 0.8 points to 52.2% — all pointing to sustained industrial activity heading into summer.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The supply chain picture adds texture for carriers and shippers. Supplier Deliveries registered 60.6% for the second straight month — the highest level since May 2022 — signaling that vendor lead times are stretching across the board. That kind of congestion typically translates to more expedited freight and tighter scheduling windows. Meanwhile, customer inventories remained deep in “too low” territory at 42.7%, which historically is a green light for continued production and restocking shipments. On the cost side, freight showed up directly in the data: trucking services were cited among commodities up in price, and panelist comments flagged rising fuel and diesel costs as a direct margin threat.

The geopolitical overhang is the wildcard. The Iran conflict was mentioned in 42% of panelist comments, with 57% flagging pricing volatility as an active concern for their companies. Diesel fuel appeared among commodities rising in price for a third consecutive month, driven by oil market pressure from the Middle East conflict — a direct headwind for carrier operating costs even as demand strengthens. The net read for trucking: industrial freight demand is the best it’s been in four years, but margin management matters more than ever with input costs climbing on multiple fronts.

Bottom line: factories are busy but anxious — strong orders, stretched supply chains, and a cost environment that’s getting harder to pass through to customers.

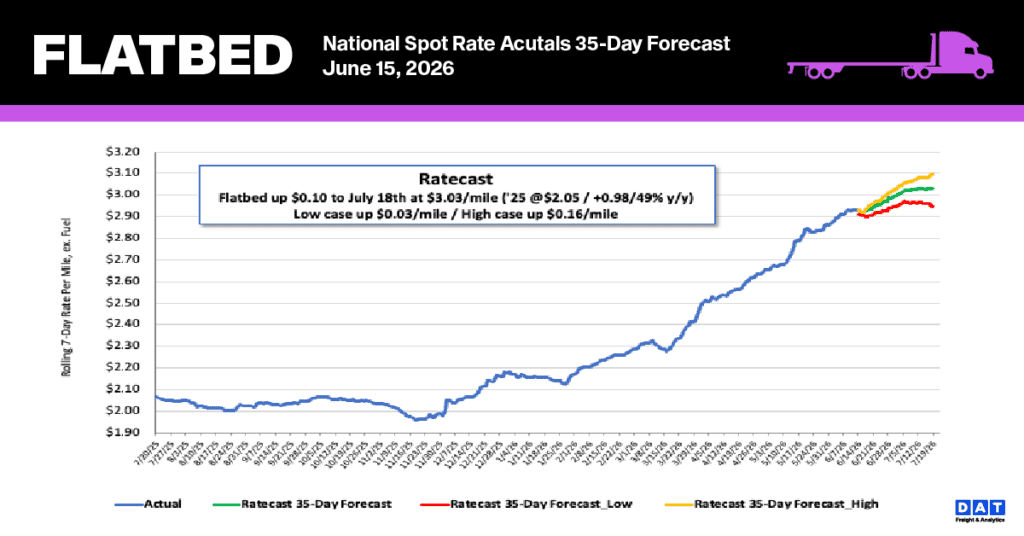

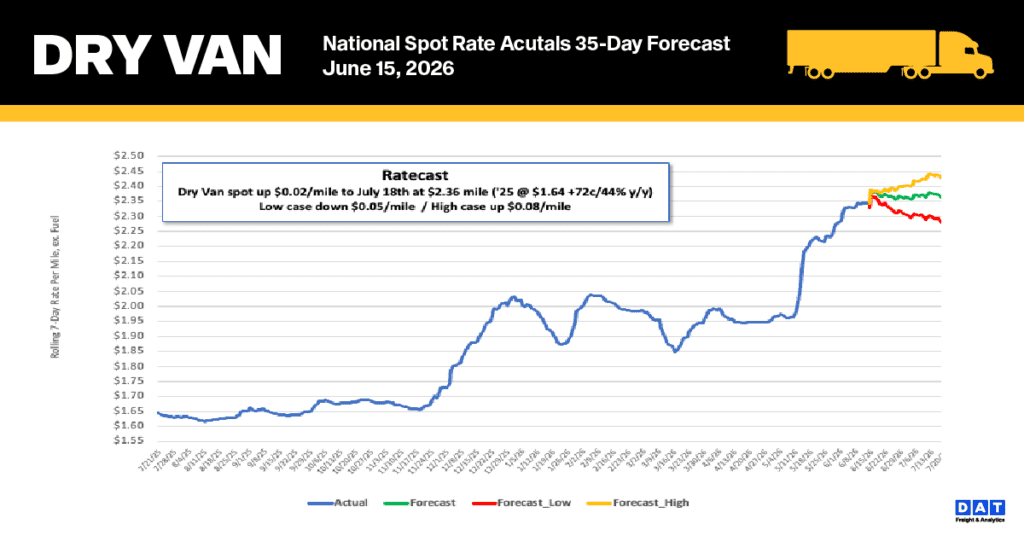

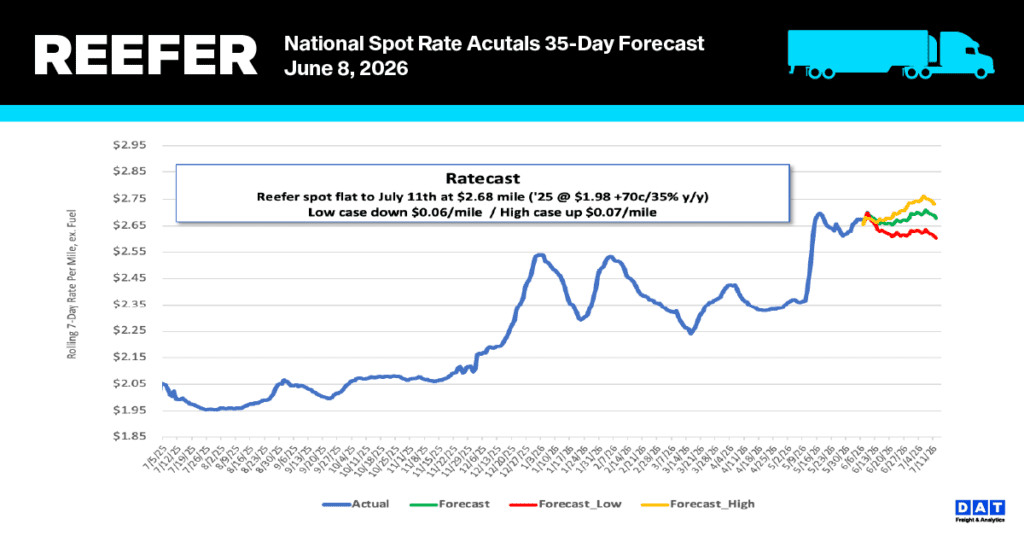

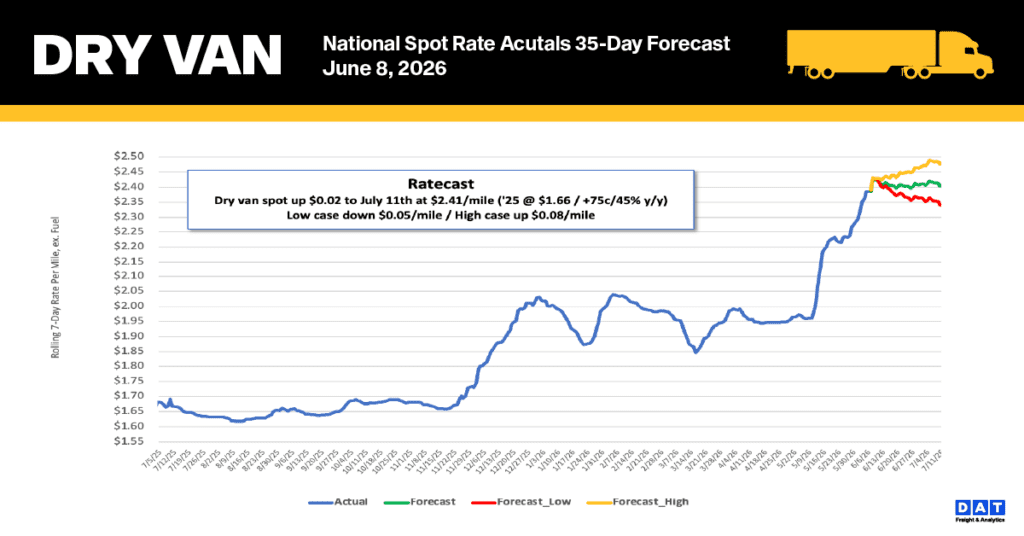

National spot rate performance

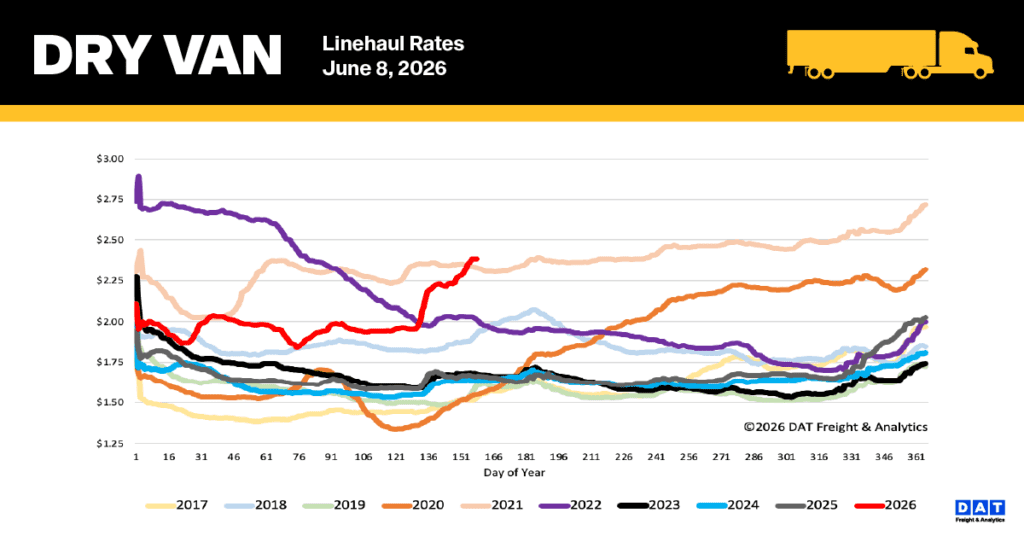

National dry van spot rates maintained an upward trajectory at the beginning of the shipping month, even as volumes softened. Linehaul rates increased by $0.07 per mile, bringing the 7-day national average to $2.39 per mile.

This current average is $0.72 (43%) above last year’s levels and $0.76 (32%) higher than the non-pandemic five-year average. Furthermore, rates have surged by $0.38 per mile (19%) since the period before Roadcheck Week, eclipsing the previous Week 22 record from 2021 by $0.05 per mile.

Regional and segment highlights

- Midwest Region: As a critical indicator for the broader economy handling nearly 50% of national load volume, this 13-state area saw average rates climb $0.16 per mile to $2.83, reflecting sustained strength in its major freight corridors.

- High-Volume Lanes: The average rate across DAT’s top 50 monitored lanes rose by $0.12 per mile to reach $2.87, which is $0.48 above the 7-day national average.

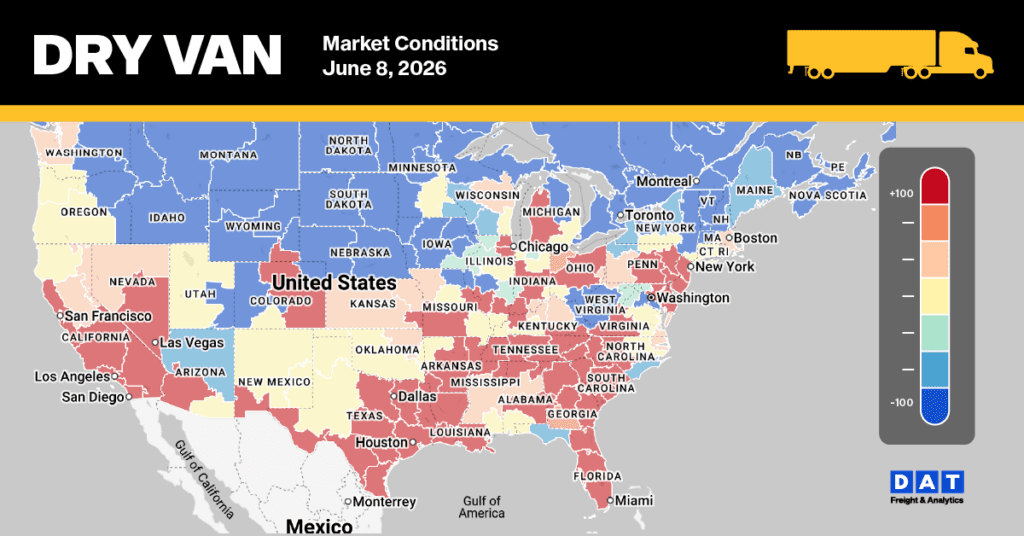

Dry Van Market Conditions

Following the conclusion of Memorial Day and Roadcheck Week, the market is experiencing a slow recovery in capacity, which contributed to the national dry van load-to-truck ratio dropping 20% to 10.54 this past week. Load postings saw a 4% week-over-week decrease; however, overall volume continues to trend significantly higher, sitting at 55% above the levels recorded during the same period last year. Furthermore, when excluding pandemic-related data from 2021 and 2022, available equipment remains 62% below the long-term average established since 2017.