The April 2026 AEM Farm Equipment Flash report delivered a mixed picture for agricultural machinery demand — and a cautionary signal for flatbed carriers who haul it. U.S. combine sales rose 3.4% year over year in April, while Canadian combine sales surged 42.7% above April 2025 levels — a bright spot in an otherwise soft report. The headline, however, belongs to tractors: both U.S. and Canadian agricultural tractor sales fell 11.3% year over year in April 2026. Since large tractors and combines move almost exclusively on flatbed trailers, back-to-back monthly declines in tractor shipments translate directly into fewer loads on key ag equipment corridors running out of the Midwest manufacturing belt.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

“The April sales results of farm tractor and combine sales show the lingering softness in the equipment market,” said Curt Blades, senior vice president at AEM. “These reflect the lingering challenges and uncertainty in the Ag economy. The progress on a US farm bill is encouraging and creates hope for more long-term growth.” The farm bill optimism is real — congressional momentum has picked up — but until a bill is signed and farmers feel confident committing capital to major equipment purchases, dealers are unlikely to place the large restock orders that fill flatbed trailers heading out of facilities like AGCO’s Hesston, Kansas plant or John Deere’s Waterloo, Iowa complex.

For flatbed carriers, the practical implication is straightforward: ag equipment lanes aren’t generating the load density that offsets weakness elsewhere in the flatbed market. DAT flatbed spot rates have been holding up better than dry van in 2026, supported by construction and industrial demand, but the agricultural equipment segment — historically a meaningful contributor to Midwest-origin flatbed volume — remains a drag rather than a tailwind. Watch the June and July AEM reports for early signs of a turn.

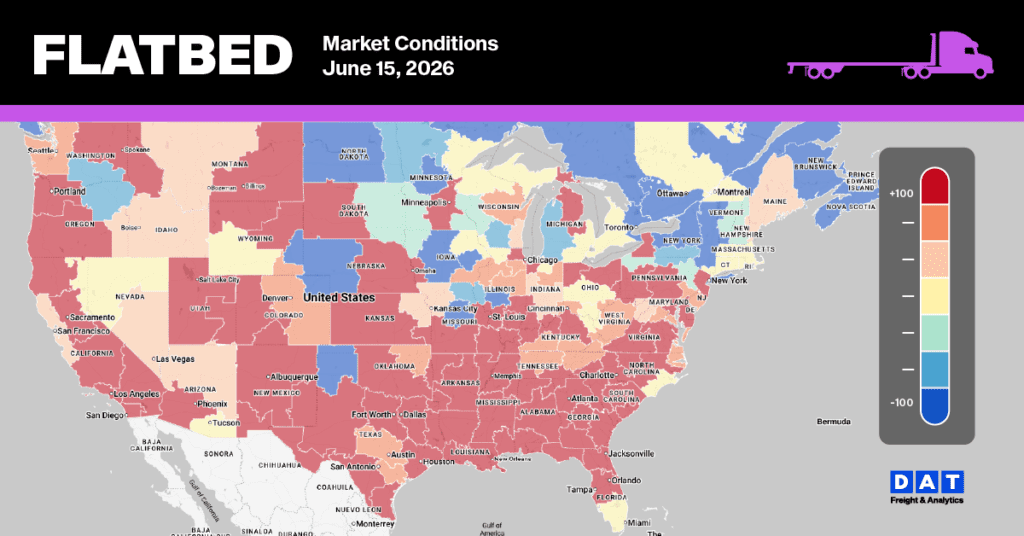

National flatbed spot rate trends

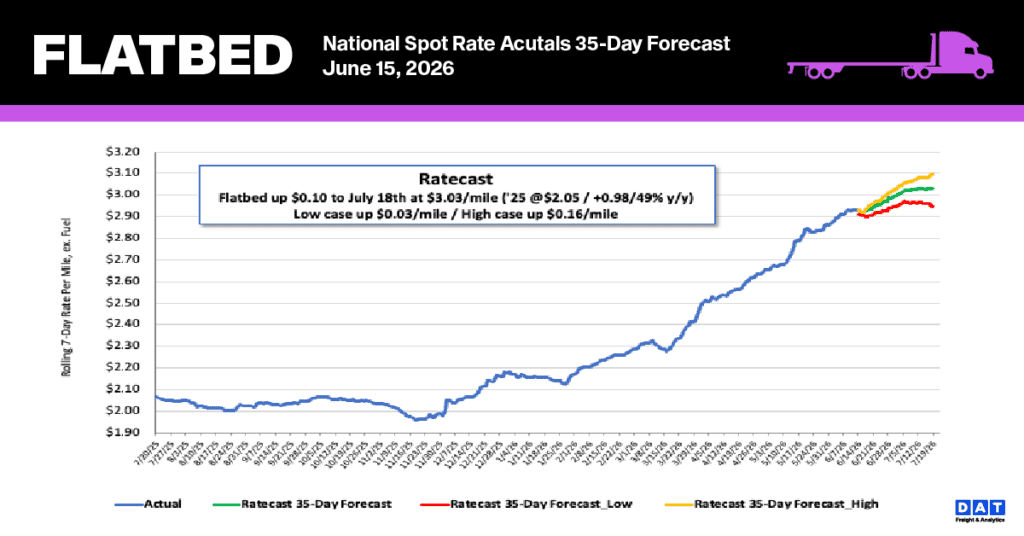

National flatbed spot rates established new benchmarks as they continued their upward trajectory. For Week 24, the 7-day rolling average rose by one cent to hit a record $2.94 per mile. This achievement marks the thirteenth straight week of growth, a period during which rates surged 25% (an increase of $0.63 per mile), ultimately exceeding the previous June 2021 record by $0.18.

Market pricing remains well above historical averages, sitting 38% ($0.82) higher than last year and 31% ($0.90) above the non-pandemic five-year norm. This sustained capacity tightening is evident in both the spot and contract sectors; specifically, new contract rates entering routing guides have climbed 6% year-over-year, ending a nearly four-year period of negative rate growth.

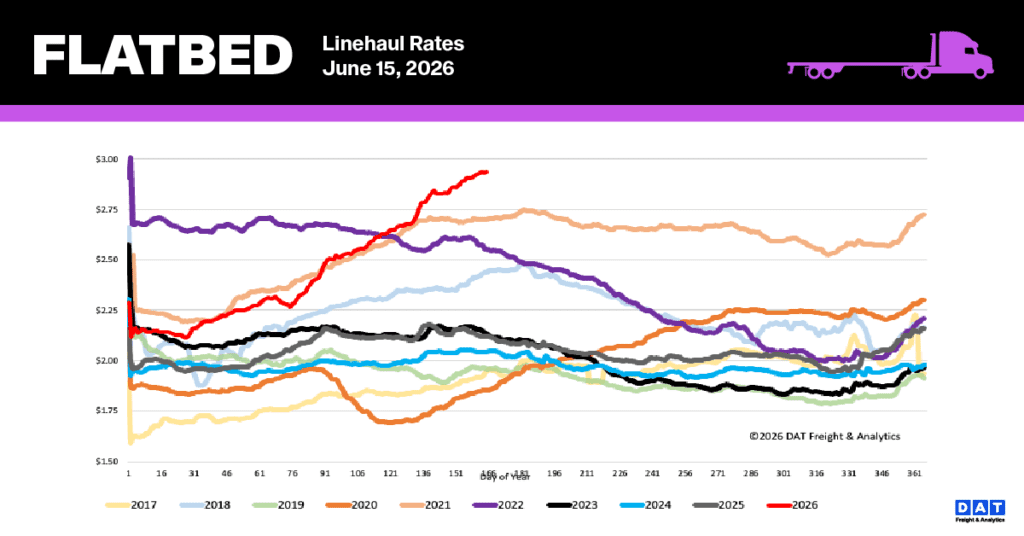

Flatbed Market Conditions

The flatbed sector continues to tighten as the open deck market approaches its peak season. Total load postings have surged 87% year-over-year and currently stand 32% above the historical long-term average (excluding the pandemic-impacted years of 2021 and 2022). Despite a 2% weekly uptick in equipment availability, postings remain 29% lower than last year’s levels. Consequently, shifting supply-demand dynamics resulted in an 8% weekly decline in the flatbed load-to-truck ratio, which finished the period at 62.38.