The SCOTUS ruling that invalidated IEEPA tariffs in February didn’t reduce trade uncertainty — it reshuffled it. The administration replaced them with a 10% Section 122 surcharge and signaled more to come, including new Section 301 and Section 232 investigations that could produce longer-duration, higher duties. Stacked on top were sharply rising ocean costs: emergency fuel surcharges of $500–$1,000 per FEU hit transpacific lanes, and Freightos Baltic Index transatlantic rates spiked 50% in a single week. Importers did the math and moved fast. Freightos research chief Judah Levine called it plainly: trans-Pacific peak season is “well underway,” driven by frontloading ahead of the tariff deadline and rising fuel costs.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The Gulf Coast is where that math hit the ground hardest. Gulf Coast container imports surged 14.8% in May, pushing volumes 15.6% above the rolling 12-month average and reaching their second-highest monthly level on record. Port Houston breakbulk tonnage amplified the story — up 3% month-over-month and 23% year-over-year according to DAT data — confirming the surge isn’t just boxes, it’s the heavy project cargo and industrial equipment that goes straight onto flatbeds. Port Houston’s general cargo volumes at multipurpose facilities rose 27% in April and are up 52% year-to-date, driven by machinery, with steel forecasts pointing to a strong May.

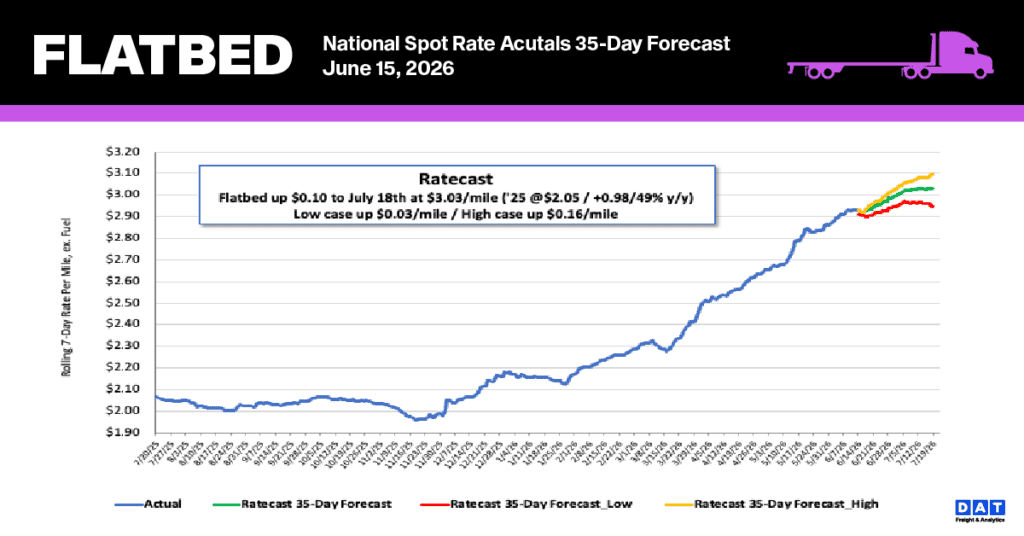

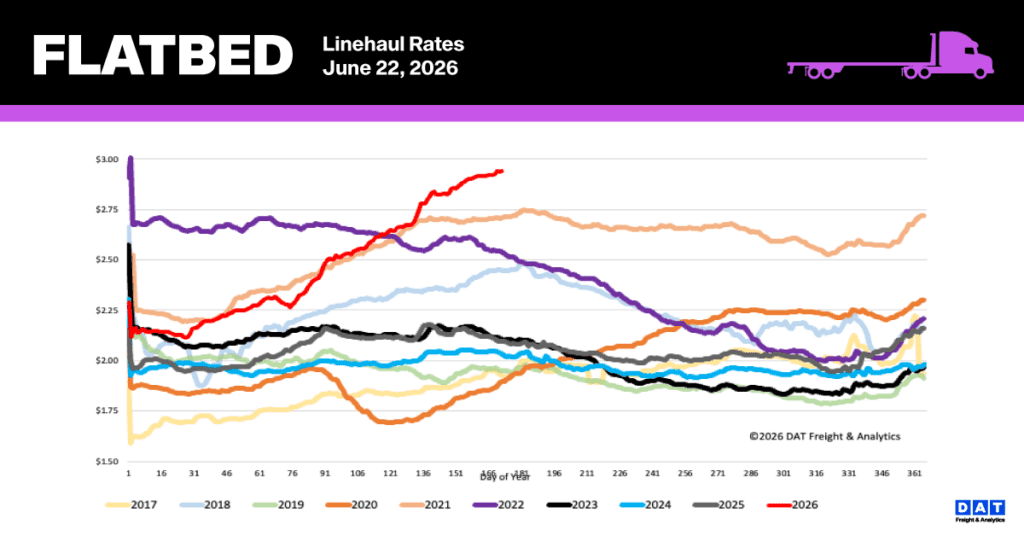

The rate signal says it all. DAT data shows Texas outbound flatbed at an all-time record $3.40 per mile — $0.65 above the previous record set during the 2022 supply crunch. That’s not a hot market, that’s a structural reset. But the clock is ticking: the NRF/Hackett Global Port Tracker sees the pullback arriving fast, with July imports forecast down 8.4% year-over-year and August and September softer still. The borrowed demand driving these rates has an expiration date. Run hard while the window is open.

National flatbed spot rate trends

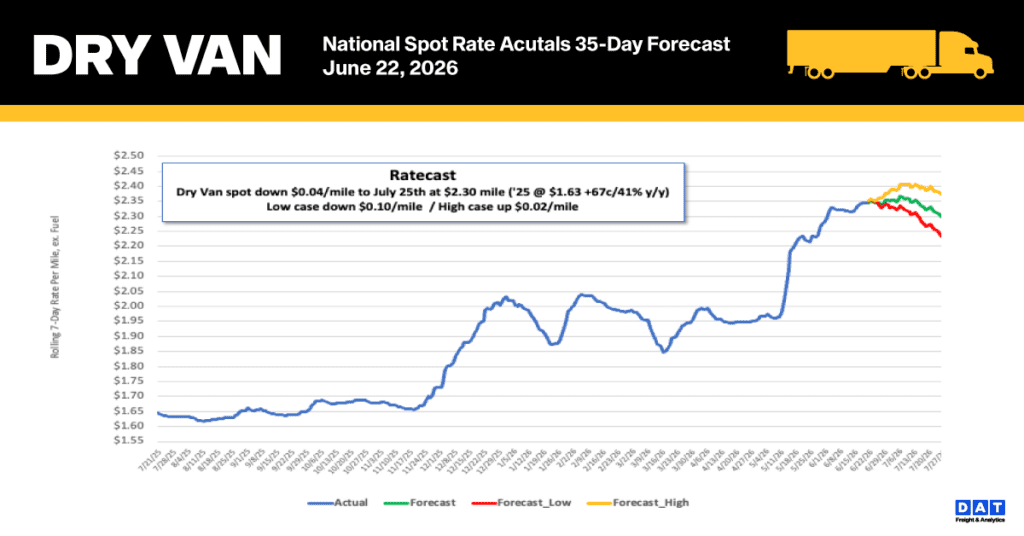

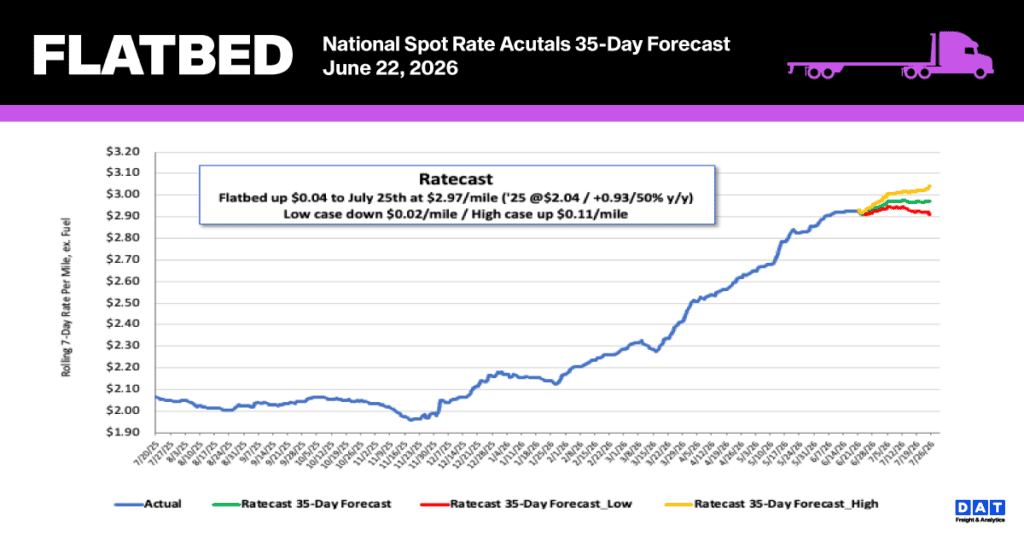

While national flatbed spot rates remain at record-breaking levels, there are signs of a seasonal plateau similar to trends in previous years. Last week, the 7-day rolling average for national flatbed spot rates held steady at $2.94 per mile, a figure that has remained consistent for three weeks. Despite this leveling off, pricing is significantly higher than historical norms—exceeding last year by 40% ($0.84) and the non-pandemic five-year average by 31% ($0.92). Furthermore, current rates are $0.23 per mile (8%) higher than the previous Week 25 record established in 2021.

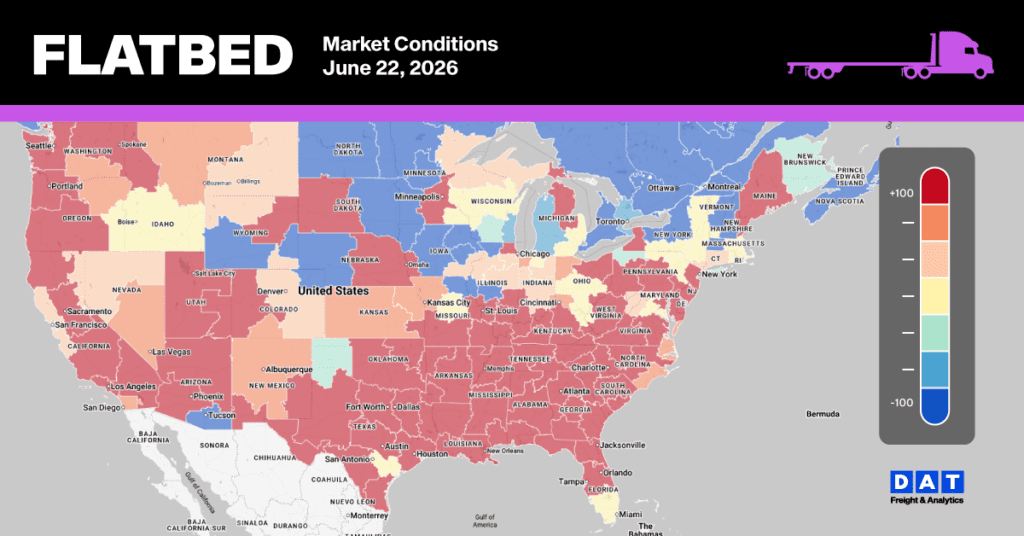

Flatbed Market Conditions

Consistent with seasonal patterns, the flatbed market is showing early signs of a summer plateau. This trend follows a 13% weekly reduction in load postings, contributing to a total decline of 21% over the past month. Despite this recent dip, overall load activity remains robust, surging 70% compared to last year and tracking 22% ahead of long-term historical averages (when excluding the pandemic years of 2021 and 2022). As equipment availability decreased by 5% last week, the flatbed load-to-truck ratio experienced its second consecutive weekly decline, falling 8% to settle at 55.68.