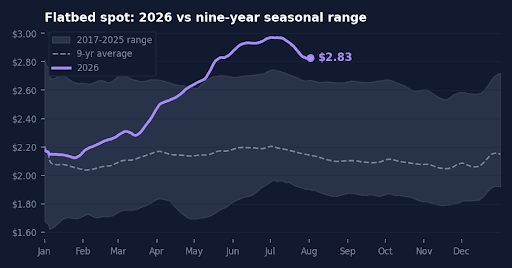

The construction backlog tells carriers and brokers where the freight is heading, and right now it points at data centers. Associated Builders and Contractors reported its Construction Backlog Indicator climbed to 9.1 months in May, a nearly three-year high, up 0.3 months from April and 0.7 months from a year ago. The driver is concentrated and clear: contractors with data center work under contract are sitting on 11.6 months of backlog, compared with 8.6 months for everyone else. That gap is the freight story. Data center projects move on flatbeds and step decks loaded with structural steel, rebar, switchgear, transformers, generators, and precast concrete, and that work is booked well into next year.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Residential construction is moving the other way. Single-family starts fell to an 882,000 annual rate in May, down 6.7% from a year earlier, with year-to-date starts off 6.3%. Single-family homes under construction dropped 5.9% year over year, and completions fell 16.8%. The National Association of Home Builders points to high interest rates, rising construction costs, and ongoing labor shortages as the weight on builders. That matters for flatbed freight because single-family construction is one of the most material-intensive sources of building-products loads, from lumber and shingles to drywall and roofing. Fewer starts and fewer homes under construction mean fewer of those dispersed residential lanes to cover.

The takeaway is a shift in where demand concentrates. Residential building products spread freight across thousands of local lanes, while data center work pulls heavy, high-value loads into a smaller number of project sites, with the South holding the longest backlog of any region. Carriers willing to position around industrial and data center corridors can find steadier work than the housing-driven lanes that are thinning out. Brokers covering those projects should expect tight capacity, and they’ll want current lane-level rate data to quote with confidence as the freight mix keeps tilting toward the build-out.

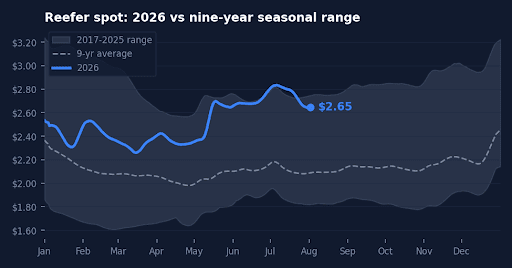

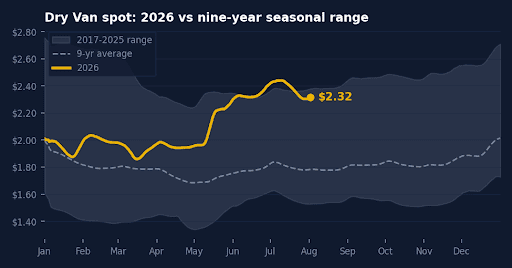

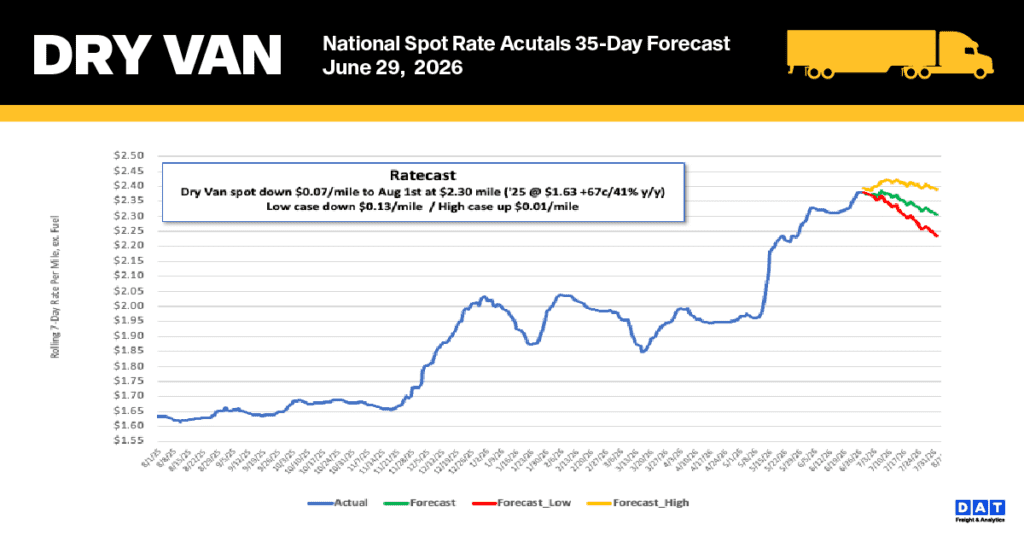

National dry van spot rate performance

Driven by a pre-July 4 volume surge and the resulting contraction in capacity, the national 7-day rolling average linehaul rate climbed $0.05 last week to reach $2.43 per mile. Dry van spot rates have risen 21% since the period preceding Roadcheck Week, establishing a new record for Week 26 that exceeds the 2021 pandemic-era high by $0.08. Market pricing remains elevated, sitting 46% ($0.79) above last year’s figures and 31% ($0.75) beyond the five-year average for non-pandemic cycles.

- Top-Tier Lanes: Rates across DAT’s 50 most-monitored lanes increased by $0.06 to reach $2.93 per mile.

- Bellwether States (IN, IL, KY, TN, MO, OH, NC, VA, MI, MS): As capacity restrictions tightened on major routes, rates in this critical 10-state market—which represents 40% of national load volume—increased by $0.04 to an average of $2.85 per mile. The van bellwethers are the auto-and-manufacturing heartland — Indiana, Michigan, Ohio, Illinois and the mid-South — the plants churning out vehicles, appliances and consumer goods, plus the distribution hubs moving retail freight in every direction. When their van rates turn, the national dry van market is turning too.

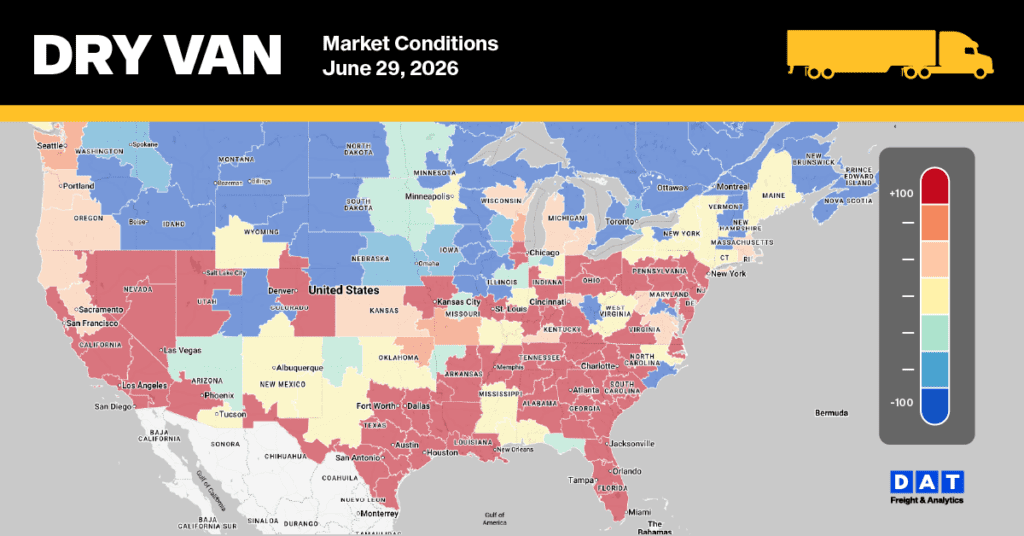

Dry Van Market Conditions

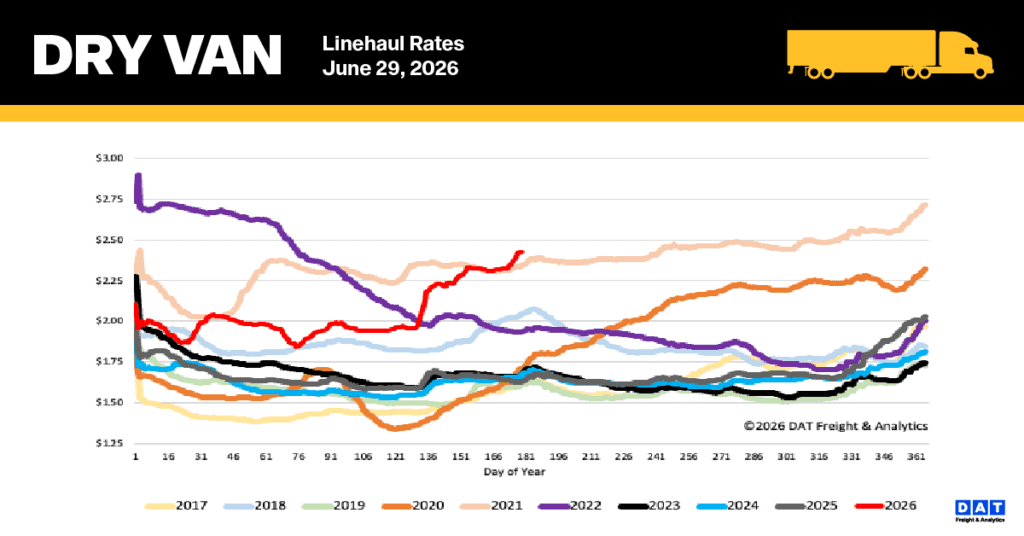

Last week, a clear pre-holiday volume spike occurred alongside a significant year-over-year reduction in truck availability. Following a period of stagnation, load postings jumped by 16% weekly and are now 44% above last year’s levels. Simultaneously, equipment postings on the DAT Load Board fell by more than 16%, representing a 27% decrease from the previous year. This supply contraction propelled the national dry van load-to-truck ratio up by 40% to 13.09, nearly doubling the figure recorded a year ago.