July isn’t just the heart of summer; it’s National Hot Dog Month and the absolute peak of America’s grilling season. As millions of consumers stock up on burgers, hot dogs, condiments, and cold beverages for backyard barbecues, food manufacturers and retailers aggressively ramp up shipments. This massive surge in temperature-controlled grocery freight directly collides with the peak produce shipping season across California, the Pacific Northwest, and the Midwest. With massive volumes of fresh fruits and vegetables coming out of the ground simultaneously, demand for refrigerated (reefer) transportation hits a boiling point, dramatically tightening reefer capacity and driving spot rates sharply upward.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

However, the impact of this summer boom isn’t contained to temperature-sensitive trailers—it creates a massive ripple effect across the dry van market as well. During quieter months of the year, many reefer carriers routinely haul non-perishable dry goods to keep their wheels turning. When July hits and high-paying produce and grilling lanes open up, these carriers quickly abandon the dry market to chase the premium refrigerated rates. This sudden “equipment migration” creates a severe capacity vacuum for standard dry van shippers, reducing the pool of available trailers and effectively pushing dry van spot rates up alongside their refrigerated counterparts.

For carriers and shippers alike, July is a high-stakes balancing act of capacity and timing. Reefer operators can capitalize on some of the highest spot rates of the year, though as noted by Uber Freight, they must contend with strict delivery windows, rigid temperature monitoring, and increased wear and tear on equipment. Meanwhile, dry van carriers benefit from the secondary capacity crunch, seeing unexpected rate lifts even on lanes completely unrelated to agriculture. Ultimately, whether you are hauling hot dogs, heads of lettuce, or dry retail goods, July requires forward-thinking capacity management and strategic lane planning to navigate the summer freight squeeze without getting burned.

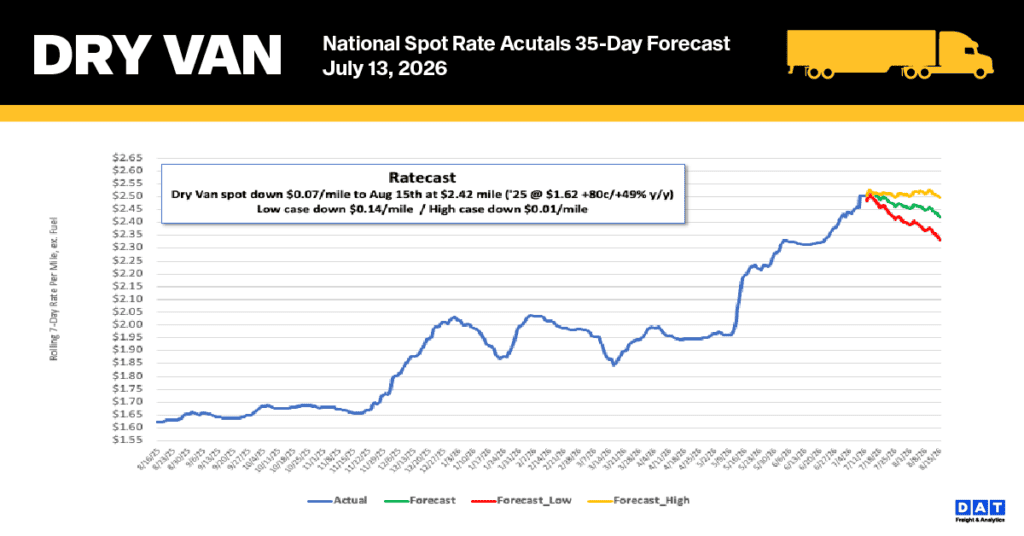

Spot rate trends

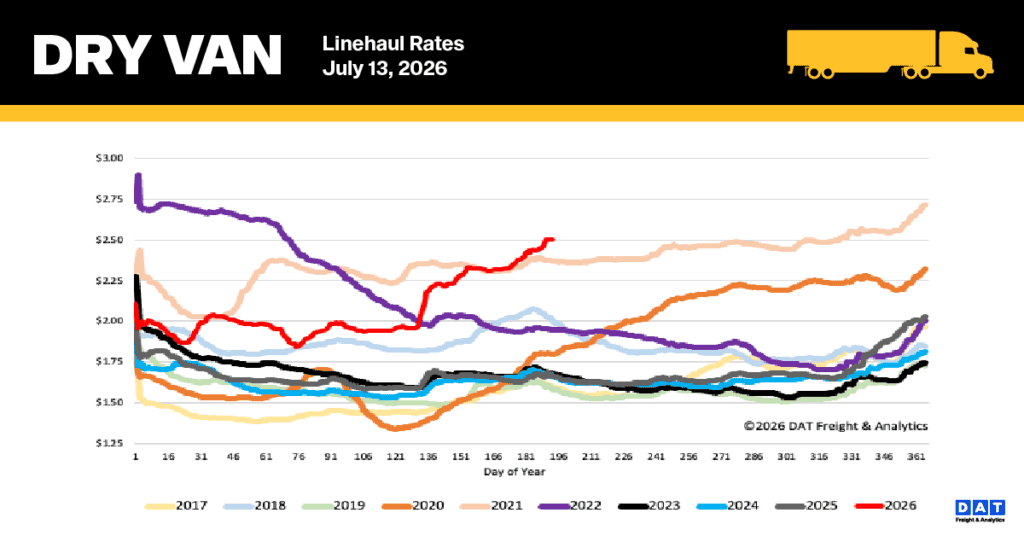

Last week, the national 7-day rolling average linehaul rate neared its seasonal peak, ticking up by less than a cent to settle at a seasonally historic $2.50 per mile. Spot market rates for dry vans have surged 28% compared to pre-Roadcheck Week levels. Additionally, they stand 51% ($0.84) higher than last year and 33% ($0.82) above the typical five-year cyclical average.

Analysis of lanes and regions

- Top-tier volume lanes: Rates across DAT’s 50 highest-volume lanes held steady at $3.06 per mile.

- Key bellwether markets (IN, IL, KY, TN, MO, OH, NC, VA, MI, MS): Outbound rates within this crucial 10-state corridor—which generates 40% of the nation’s total volume—rose by $0.07 to an average of $3.05 per mile. Serving as the country’s manufacturing and automotive backbone, these states contain the factories and logistics hubs that drive consumer goods distribution, meaning fluctuations here frequently foreshadow wider shifts across the national dry van landscape.

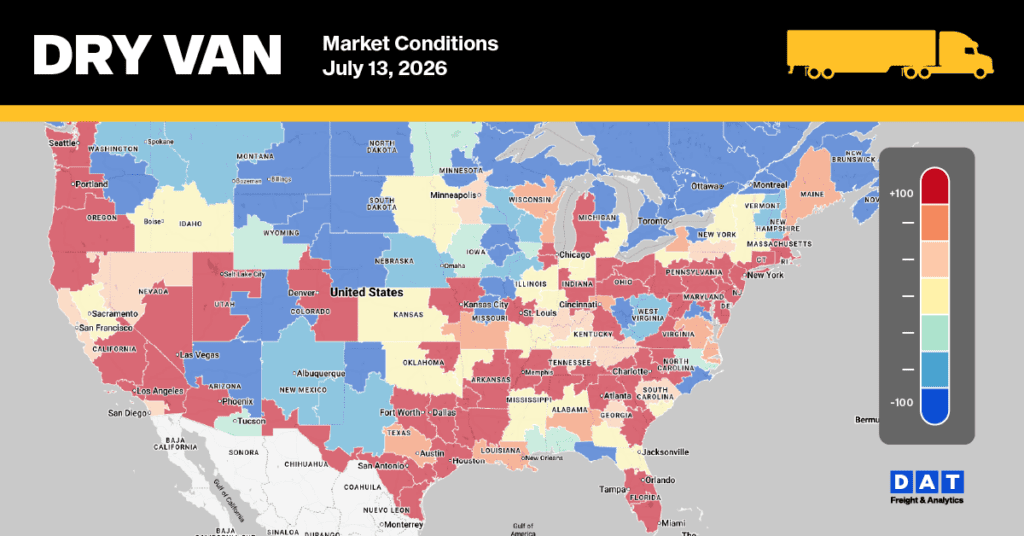

Market conditions

During the first full five-day workweek following the July Fourth long weekend, load post volumes declined by 11% compared to the week preceding the break, though they remained roughly 21% higher year-over-year. Truckload capacity historically recovers at a slower pace after public holidays, and Independence Day was no exception. With equipment post volumes dropping by approximately 6% from pre-holiday levels, the national dry van load-to-truck ratio experienced a 12% increase, rising to 12.11.