The ATA For-Hire Truck Tonnage Index edged up 0.4% in January to a seasonally adjusted reading of 113.0, following a 0.2% decline in December. While that modest gain continues a gradual climb off the October bottom, it’s worth keeping in perspective: January tonnage was still 1.3% below the 2025 peak set in August, and the full-year 2025 index came in flat compared to 2024. Year-over-year, January was up just 0.5% — incremental progress, but not the kind of momentum that signals a broad demand-side inflection.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

For carriers and brokers watching the DAT load boards, this report reinforces what the rate data has been showing for months — the freight market’s improvement story is largely being written on the supply side. As ATA Chief Economist Bob Costello noted, the carriers still in the game are benefiting from reduced overall capacity, not a surge in freight volumes. That dynamic matters for how you price and position heading into spring. If demand-driven volume growth doesn’t materialize to complement the capacity reductions already baked in, rate recovery will remain grinding and uneven. Watch for whether produce season and import activity in Q2 can add a demand catalyst to what has so far been a supply-driven setup.

National flatbed linehaul spot rates

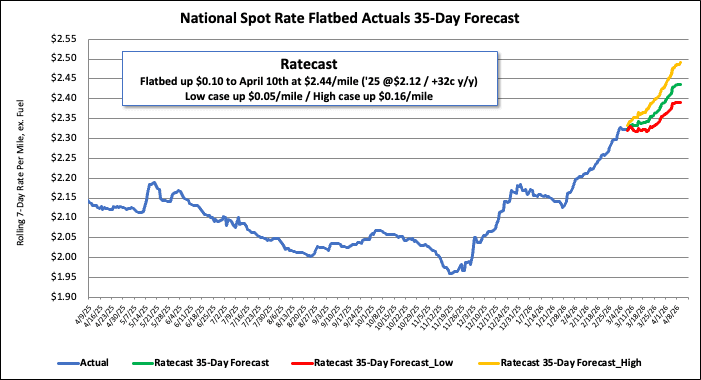

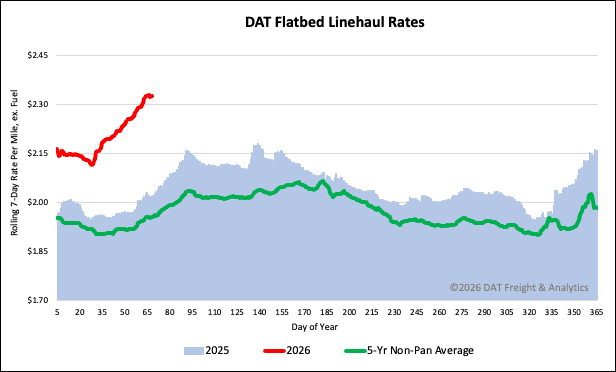

The national average spot rate for flatbed linehaul reached $2.33 per mile last week, marking the fifth consecutive week of increases in the $0.03 to $0.04 per mile range, including a $0.04 rise last week. This rate is significantly higher than previous years: $0.29 per mile (15%) above the rate from the same time last year, $0.16 per mile higher than the 2018 rate, and $0.37 per mile (16%) greater than the five-year average (excluding pandemic-impacted years).

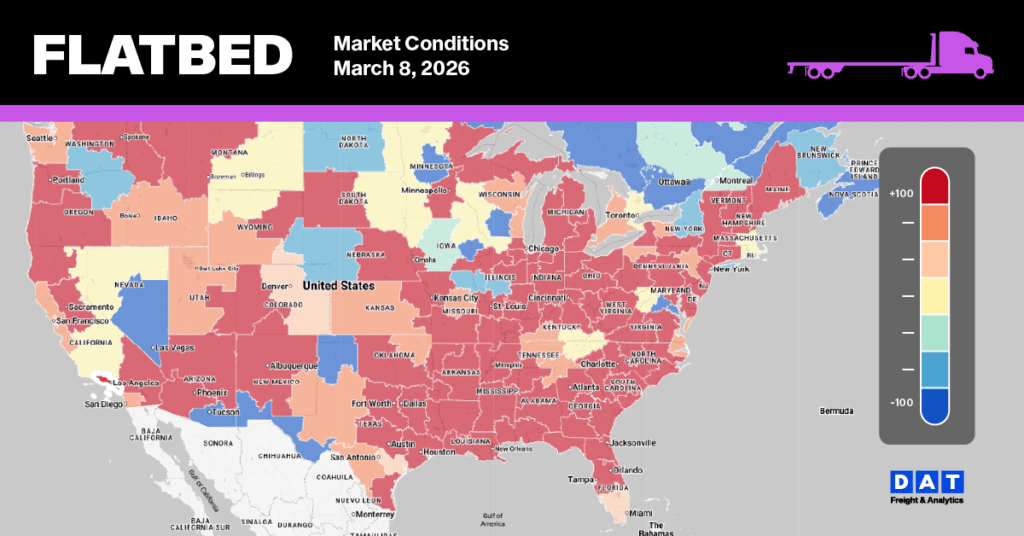

Flatbed Market Conditions

The flatbed spot market is experiencing continued capacity tightening. Last week, flatbed load post volumes grew by 4%, building on the 10% jump seen the week before at the end of February. Current volumes are now nearly 47% higher than they were this time last year. Despite flatbed equipment posts remaining mostly flat, the flatbed load-to-truck ratio rose by 3% last week, reaching 70.97.