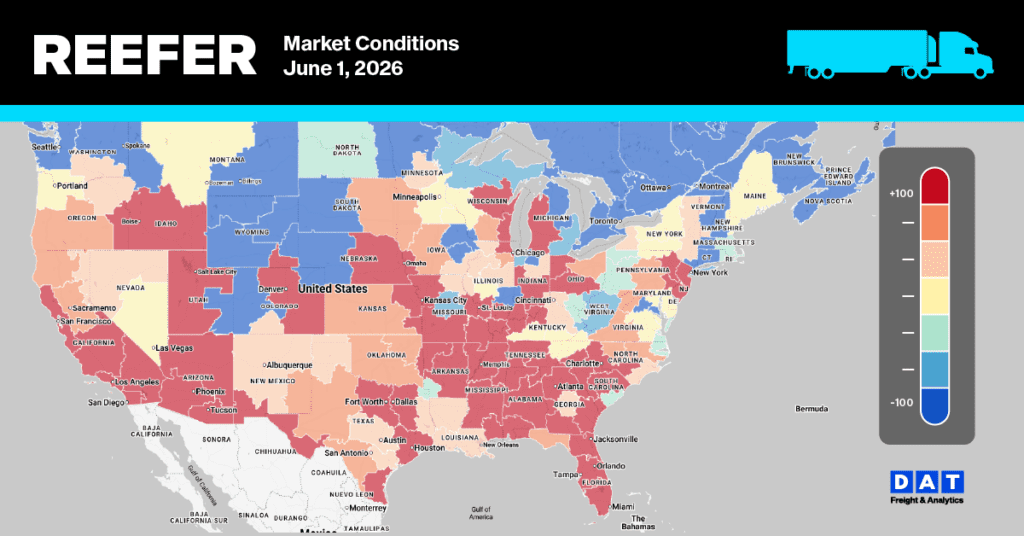

The big picture

Florida just posted its most dramatic single-week rate swing of the season — and the story isn’t over. After a sharp post-Mother’s Day correction last week, Central and South Florida came roaring back this week, with Baltimore surging +43% and New York recovering +10% off last week’s lows. The origin remains on Shortage status, and the commodity mix — watermelons, tomatoes, peppers, cantaloupes — signals we’re deep into the summer transition window. Meanwhile, California districts broadly pushed higher across East Coast lanes, with South District citrus and South Texas stabilizing near flat after last week’s historic collapse. Yakima quietly downshifted from Slight Shortage to Adequate, a signal worth watching as Pacific Northwest cherry season ramps. This is a market where carriers hold pricing power in the Southeast and on California East Coast runs — but the divergence between individual lanes is wide enough that routing decisions made today will matter for weeks.

1. Central and South Florida — Shortage | Watermelons, Tomatoes, Peppers, Cantaloupes

Last week Florida corrected hard after Mother’s Day floral demand evaporated. This week it snapped back — with one lane more than doubling. Shortage conditions persist. The commodity mix is transitioning toward summer field crops: watermelons, cantaloupes, and multiple pepper varieties are listed alongside tomatoes, okra, squash, and corn.

Multi-week arc: Florida is now in boom-bust-boom territory. After posting gains of 14–42% on April 21 and then correcting sharply the week of May 26, this week’s bounce — particularly the NYC lane — suggests sporadic load availability and aggressive spot pricing by brokers working residual Shortage inventory. The season is winding down; every load matters more as the pool shrinks.

2. South & Central District California — Slight Shortage | Citrus, Avocados, Leafy Greens, Brassicas

Citrus lanes had the most significant moves this week. Dallas exploded +20% and Miami and New York each jumped +17%. Leafy green and brassica lanes held mostly flat on the East Coast corridors. Citrus and leafy commodities are shipping from the same district — blood oranges, cherries, lemons, grapefruit alongside broccoli, Brussels sprouts, cauliflower, and leafy greens.

The +17–20% citrus moves on Southern and East Coast lanes are the week’s biggest California story.

3. Imperial/Coachella/Calexico/San Luis — Slight Shortage | Lettuce, Berries, Brassicas, Greens

After going flat across all lanes last week — a rare across-the-board hold — Imperial/Coachella bounced this week. Atlanta led the recovery at +18%. The commodity list is heavy on berries (blackberries, blueberries, raspberries) alongside the full spectrum of leafy greens and brassicas.

4. Santa Maria, California — Slight Shortage | Lettuce, Broccoli, Cauliflower, Celery, Strawberries

Santa Maria had a split week: Boston surged +16% while New York reversed sharply at –10%. The NYC move is a notable outlier given broad East Coast strength and warrants verification. All other lanes posted modest gains of +1% to +9%.

5. Salinas-Watsonville, California — Slight Shortage | Lettuce, Broccoli, Cauliflower, Strawberries

Salinas continued its steady post-transition hold, with small gains on Chicago and New York and flat movement on Baltimore and Philadelphia. This is the dominant East Coast lettuce supply source for the summer season.

6. Mexico Crossings Through South Texas — Adequate | Peppers, Tomatoes, Watermelons, Citrus, Limes

South Texas stabilized this week after posting historically large declines last week (Atlanta -26%, Baltimore -27%, New York -23%, Dallas -41%). This week, virtually all lanes were flat to slightly negative, with the biggest move being just -4% to Los Angeles. Adequate truck availability confirms the supply-demand rebalance is holding.

Multi-week arc: Two weeks ago South Texas was a surge story, absorbing Florida overflow and posting Slight Shortage rates. Last week it corrected violently. This week’s flatline is either a floor forming or a brief pause before further normalization — watch Atlanta and Chicago for directional signal next week.

7. Nogales, Arizona — Adequate | Cucumbers, Grapes, Honeydews, Mangoes, Tomatoes, Watermelons

Nogales bounced broadly this week after last week’s across-the-board declines of -3% to -20%. Chicago and Dallas led the recovery at +17% and +18% respectively. Remains on Adequate status.

8. Vidalia District, Georgia — Adequate | Dry Onions

Vidalia onions continue their steady mid-season pace with modest gains across all lanes. This is peak Vidalia pack window — the season typically runs April through mid-June, meaning we may be approaching the final 2–3 weeks of active shipping.

Seasonal flag: Vidalia onion shipping season typically closes mid-June. Watch for a “last report” designation in the next 1–2 weeks.

9. Kern District, California — Slight Shortage | Carrots

Kern had a mixed week: Baltimore gained +10%, Chicago held near flat (+1%), while New York pulled back –7%. Philadelphia was unchanged.

10. Oxnard District, California — Slight Shortage | Celery, Strawberries, Greens, Kale

Oxnard posted solid gains on both active lanes.

11. Yakima Valley & Wenatchee, Washington — ⬇️ Adequate (from Slight Shortage) | Apples, Cherries, Asparagus, Pears

Status shift: Yakima downgraded from Slight Shortage to Adequate this week. No percentage changes were published, indicating this is likely an initial or revised baseline report. Washington cherry season is beginning to appear in the commodity mix alongside apples, asparagus, and pears.

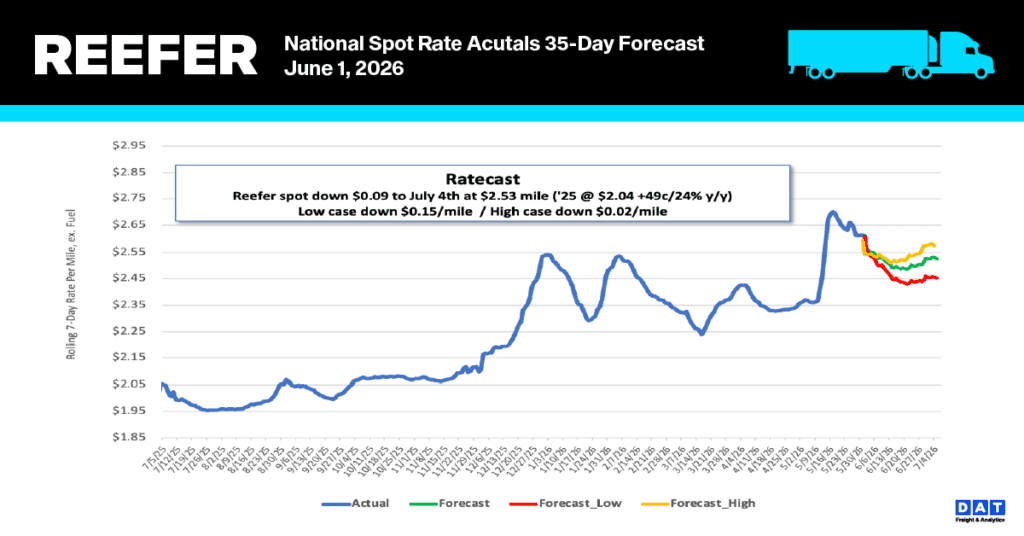

National Reefer Spot Rate Trends

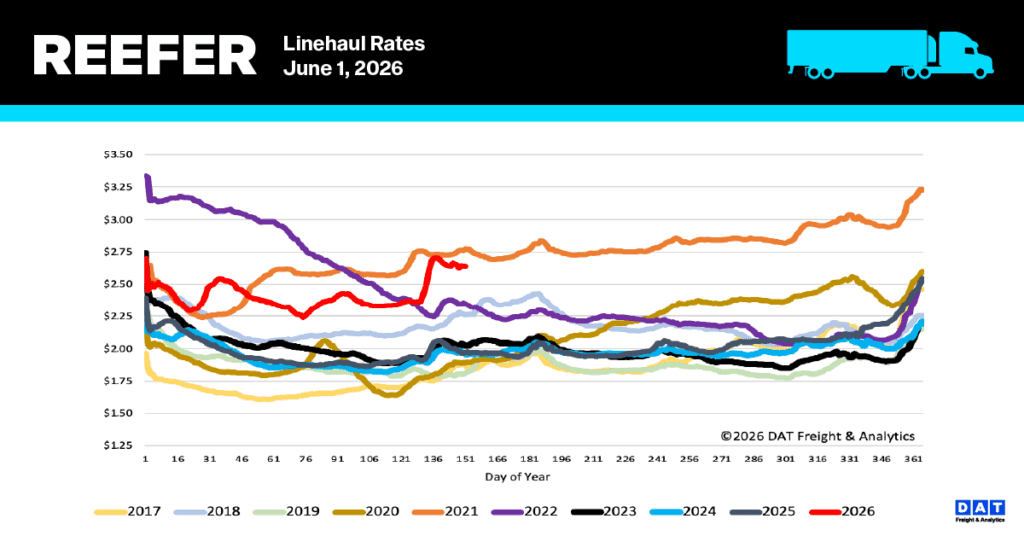

National refrigerated linehaul rates saw a slight reduction of one cent, bringing the 7-day rolling average to $2.64 per mile. Although there was a marginal dip, reefer spot rates—excluding fuel surcharges—persist at record highs across all products and temperature requirements. Market performance continues to be notably strong, sitting 34% ($0.66) higher than last year and 26% ($0.70) above the non-pandemic five-year average. While current spot rates have increased by $0.27 per mile (12%) since before Roadcheck Week, they remain $0.14 under the Week 22 record established in 2021.

In major produce hubs, the average spot rate for transporting fruits and vegetables is currently $3.89 per mile. This figure represents a week-over-week decline of approximately $0.27 per mile, yet it remains $0.42 higher than the rates recorded during the same period in the previous year.

USDA reporting indicates that produce volumes declined by 13% this past week, following a steady month-long climb prior to Memorial Day; however, current levels are nearly on par with the same post-holiday period last year. While national refrigerated truckload capacity remains under pressure from increased enforcement, the produce sector noted a minor reprieve in its persistent capacity deficit, easing slightly from previous weeks.

Reefer Market Conditions

Market capacity in the refrigerated sector is currently stabilizing as equipment returns following the previous holiday-shortened week. While supply is recovering, equipment postings remain 25% below the levels seen during this same period last year, whereas load postings have surged by 53% year-over-year. These dynamics caused the load-to-truck ratio to decrease by 7% to 19.92, which nevertheless stands as a ten-year record for Week 22.