Data analysis for the week ending Wednesday, April 14th, 2026 Week 16. All rates cited below exclude fuel surcharges, and load volume refers to loads moved unless otherwise noted. The rate charts exclude 2021 and 2022 years influenced by the pandemic.

The big picture

California is taking over the report as truckload volumes increase 17% y/y.. This week, Kern District, Salinas-Watsonville, and South/Central District all added Chicago and New York lanes for the first time, with Kern carrots to New York opening at $9,700–$10,400 and Salinas lettuce to New York at $10,100–$10,900. California citrus surged again — Chicago +12%, Philadelphia +8%, Baltimore +7% — confirming this isn’t a one-week spike but a sustained tightening as the season winds down. Meanwhile, Yakima’s massive rate surge from last week unwound sharply (Chicago -15%, Dallas -24%) as truck availability eased back to Adequate, Nogales whipsawed again with most lanes falling but Chicago hitting Shortage for the second time (+14%), and South Texas held at elevated levels for a fifth straight week. Florida flatlined. The spring produce season is fully in motion, and California — from Salinas to citrus — is commanding the freight map.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

California is expanding lane coverage and rates are firming. The biggest development this week isn’t a single rate move — it’s the structural expansion of California lanes in the USDA report. Outbound Fresno reefer spot rates are already up 44% y/y as lettuce volumes jump 22% w/w. Three regions added Chicago and New York destinations for the first time, all at Slight Shortage:

- Kern District (carrots):

- Kern → New York: $9,700–$10,400 (first report) – Rateview spot up 45% y/y

- Kern → Chicago: $5,900–$6,600 (first report) – Rateview spot up 26% y/y

- Salinas-Watsonville (broccoli, cauliflower, lettuce, strawberries):

- Salinas → New York: $10,100–$10,900 (first report)

- Salinas → Chicago: $6,300–$7,300 (first report) – DAT load posts up 65% y/y

- Salinas → Philadelphia: $9,600–$10,400 (+3%)- DAT load posts up 48% y/y

- South/Central District (avocados, artichokes, broccoli, cabbage, cauliflower, celery, leafy greens, grapefruit, lemons, radishes):

- South/Central CA → New York: $9,800–$10,400 (first report)

- South/Central CA → Chicago: $6,100–$6,900 (first report)

- Imperial/Coachella (lettuce, broccoli, berries, leafy greens): → Baltimore: $9,000–$9,500 (-1%); → Philadelphia: $9,200–$9,700 (-1%)

- Oxnard (celery, cilantro, greens, kale, parsley, strawberries): → Philadelphia: $9,400–$10,400 (+4%); → Baltimore: $8,500–$9,000 (-3%)

- Santa Maria (broccoli, cauliflower, celery, lettuce, strawberries): → Philadelphia: $9,000–$9,500 (+1%); → Baltimore: $8,600–$9,400 (-2%)

California citrus surged again. South/Central CA citrus (blood oranges, grapefruit, lemons, oranges, tangelos) remained at Slight Shortage on all nine destinations with rates climbing on every lane:

- South/Central CA → Chicago: $6,100–$6,400 (+12%)

- South/Central CA → Philadelphia: $8,900–$9,500 (+8%)

- South/Central CA → Baltimore: $8,600–$9,200 (+7%)

Nogales whipsawed again — mostly down, but Chicago hit Shortage for the second time

- Nogales → Chicago: $6,100–$6,300 (+14%)

- DAT spot from Nogales to Chicago are up 50% y/y. .

South Texas held steady for the fifth consecutive week

Florida flatlined. Rates were essentially unchanged across all six lanes. Truckload produce volumes have tanked – down 9% w/w and 58% y/y. Outbound Lakeland reefer spot rates are also dropping, down just 2% w/w and 8% in the last month.

The complete produce wrap can be found here or at DAT.com/blog

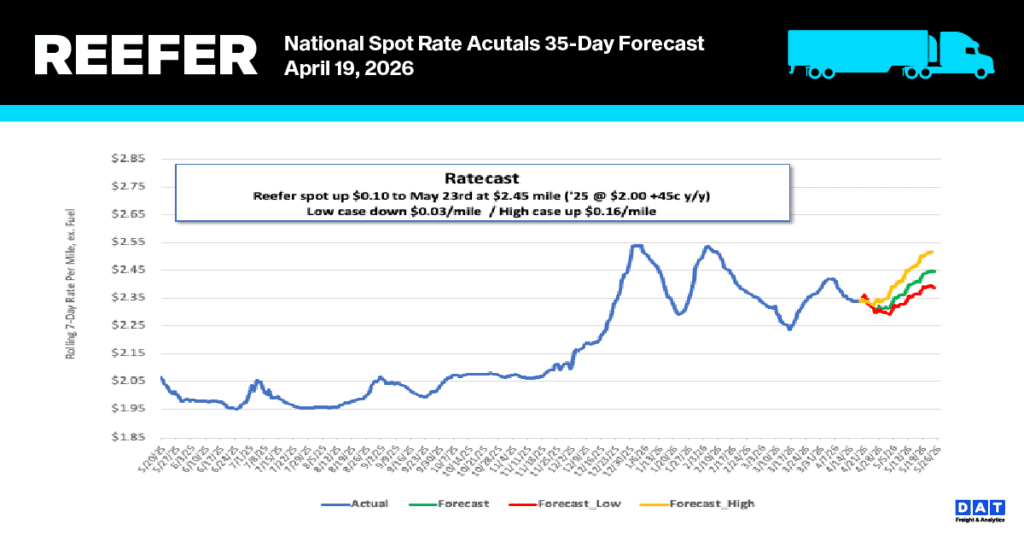

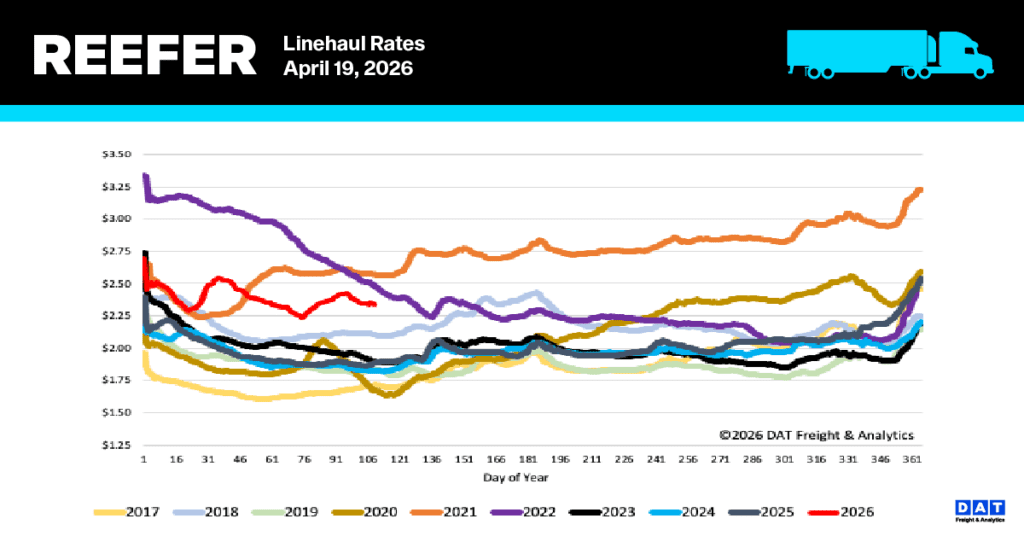

National reefer linehaul spot rates

Reefer linehaul rates dropped by another $0.04 per mile last week, settling at an average of $2.35 per mile. Even with this recent two-week decline totaling $0.06 per mile, reefer spot rates (excluding fuel) are significantly higher than in past years. Specifically, they currently stand $0.45 (25%) above last year’s rate and $0.52 (22%) above the five-year average, excluding the notably high-rate periods of 2021 and 2022.

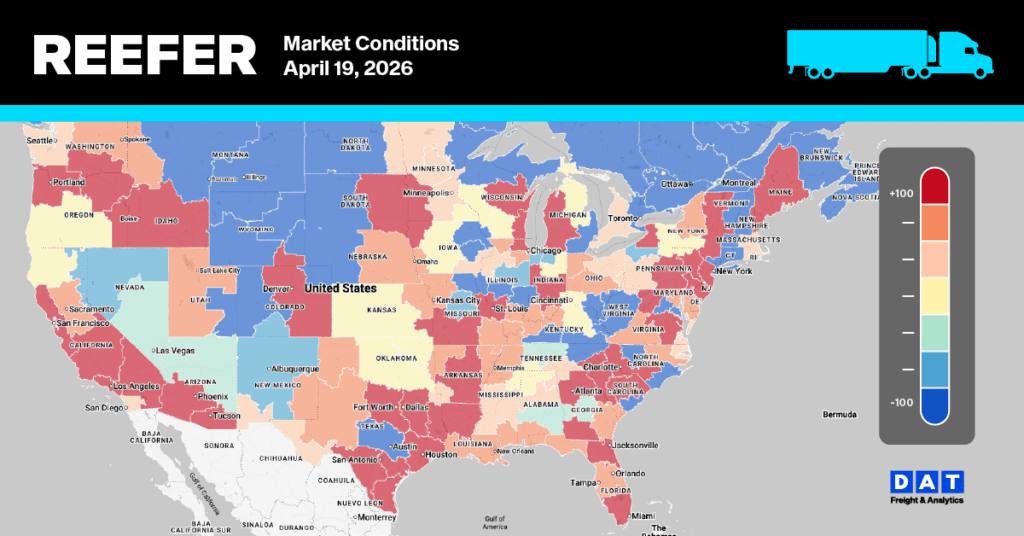

Reefer Market Conditions

The reefer market experienced a notable weekly softening, with the load-to-truck ratio dropping 4% to 12.84. This decline was largely a result of a 9% reduction in the volume of load posts. Despite this recent dip, current load volumes remain strong, exceeding last year’s figures for the same period by over 35%. Furthermore, reflecting a broader tightening of truckload capacity, equipment posts also saw a 5% decline last week, reaching their lowest level for Week 16 in ten years.