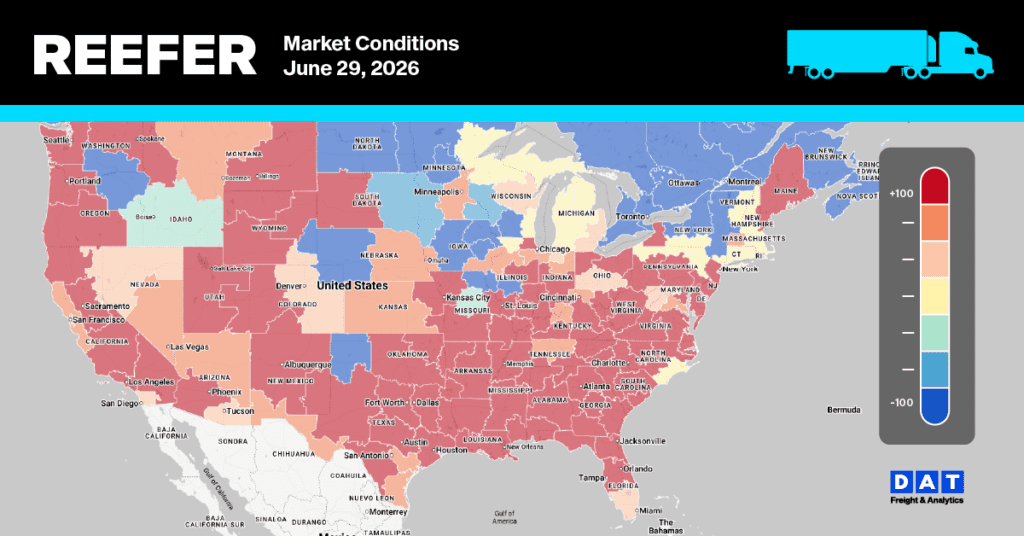

Florida is officially in the rearview mirror. This week’s report drops Central and South Florida from the availability table entirely, leaving Georgia to carry the Southeast tomato and watermelon basket alone under continued Shortage conditions — and rates there are still climbing (+4% to +17%). Right on schedule, Mexico Crossings through South Texas flipped from Adequate to Slight Shortage, confirming last week’s forecast that South Texas would absorb Florida’s departing volume. The South Texas → Boston lane, which spiked +19% last week, held flat this week at $8,400–$8,800 — a plateau, not a reversal. Meanwhile, California’s South and Central District split into two distinct markets: general row-crop and lettuce business stays Adequate, but a new citrus-specific line (grapefruit, lemons, oranges) debuted at Slight Shortage, the clearest data confirmation yet of the navel orange close tightening the last of the state’s citrus capacity. Santa Maria’s general market also lit up, with the Atlanta lane jumping +47%. The lone loosening signal came from Nogales, which eased to Slight Surplus as Mexican cross-border volume broadens.

Georgia (Standalone) — Florida’s exit confirmed

Central and South Florida no longer appears in this week’s availability table — last week’s “Last Report” designation has run its course, and Georgia now carries the Southeast tomato and watermelon trade on its own under continued Shortage conditions.

Vidalia’s onion district, by contrast, is dead flat across the board — a stable Adequate market sitting right alongside the tightening tomato trade:

Mexico crossings through South Texas — The absorption materializes

South Texas flipped from Adequate to Slight Shortage this week — the overflow-absorption pattern flagged last week is now showing up in the availability designation, not just the rate data.

Note: the Boston lane’s flat reading this week is itself notable given last week’s +19% jump — the market appears to be holding the new, higher level rather than reverting. In DAT RateView, reefer spot rates for all trailer temperature zones and commodities were also flat last week but holding 44% higher than last June.

California — Citrus splits off as navel season closes

South and Central District California now carries two distinct availability designations — a first this cycle. General row crops and lettuce stay Adequate, but a new grapefruit/lemon/orange line debuted this week at Slight Shortage, consistent with the navel orange close tightening the last of the season’s citrus capacity (Valencias and lemons continue through summer).

Santa Maria’s berry and lettuce market also moved sharply, led by an outsized jump on the Atlanta lane. Salinas-Watsonville held mostly steady with a modest broad-based lift.

Imperial/Coachella/Central-Western Arizona also firmed broadly, with double-digit gains on several lanes. Kern (carrots) and Oxnard (celery, cilantro, greens, kale, parsley, strawberries) both ticked up modestly, staying comfortably in Adequate territory.

Mexico crossings through Nogales — The lone loosening lane

Nogales eased from Adequate to Slight Surplus, the only district moving toward looser capacity this week, on a honeydew/mango/tomato basket.

Yakima Valley & Wenatchee, WA — Steady Slight Shortage

Washington’s tree fruit and berry district holds at Slight Shortage, with modest increases across most lanes.

What this means for carriers, shippers & brokers

Carriers: South Texas is now the tightest capacity story in the Southeast — Florida is gone from the board, and this district’s Adequate-to-Slight Shortage flip means better leverage on outbound lanes, particularly Boston, which is holding its recent gains rather than giving them back. Georgia’s tomato/watermelon lanes remain Shortage-rated and worth prioritizing if you’re running reefer capacity through the Southeast. On the West Coast, the new citrus-specific Slight Shortage line out of South/Central California is a signal to watch grapefruit/lemon/orange loads more closely as navel season winds down.

Shippers: Budget for continued rate pressure on Georgia and South Texas lanes into early July — neither market shows signs of easing. If you’re moving California citrus, expect the new Slight Shortage designation to translate into firmer pricing on those specific loads even as general California lettuce and row-crop business stays Adequate. The Santa Maria → Atlanta jump (+47%) could be a one-ff with the World Cup this week.

Brokers: Two items need cross-checking before you quote off this report. First, Santa Maria → Atlanta’s +47% move is an outlier versus the rest of that district’s lanes – worth more analysis before pricing loads off it. Second, the South Texas → Boston lane’s flat read this week — after last week’s +19% spike — suggests the market has repriced rather than reverted; treat $8,400–$8,800 as the new working range rather than expecting a pullback. Nogales is your one loosening lane this week if you need a counterbalance on the West Coast/Southwest side.

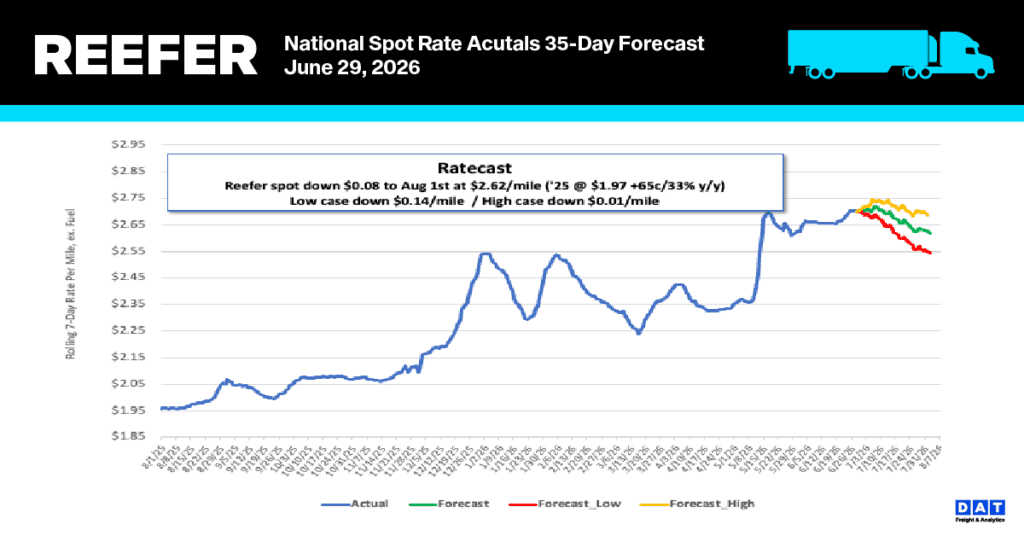

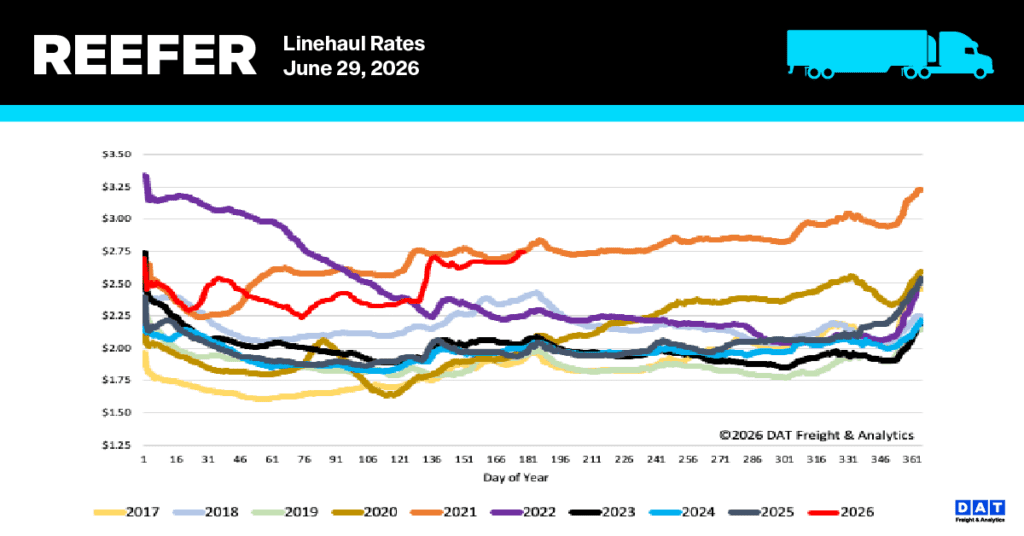

National reefer market: spot rate analysis

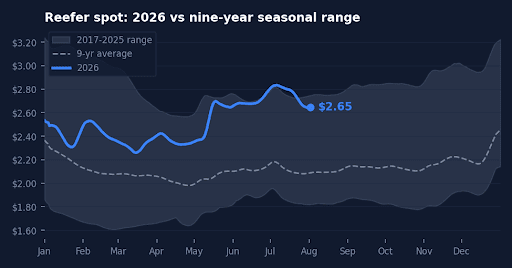

Mirroring dry van patterns, national reefer linehaul rates climbed by $0.06 per mile last week, reaching $2.74 as the July 4 holiday approaches. This 7-day rolling average sustained the peak performance seen during Roadcheck Week, finishing 16% ($0.38) above early May levels. Current spot pricing for reefers is 40% ($0.78) higher than last year and 27% ($0.74) above the non-pandemic five-year norm, matching the Week 26 record established in 2021.

- Bellwether Performance (AR, IL, IN, KY, KY, MO, OH, PA, TN, TX, WI): Rates in this 10-state “food engine room” market — accounting for 43% of national volume — rose $0.04 to $3.10 per mile as capacity loosened. Unlike seasonal produce hubs, these states rely on year-round staples like dairy, poultry, and processed foods, providing a more consistent barometer for the national reefer market.

Produce sector trends

Spot rates in primary produce hubs rose by $0.05 last week to an average of $4.03 per mile, remaining $0.45 higher than the prior year. While USDA reports show volumes have declined for three consecutive weeks—down roughly 21% year-over-year—a late-season surge is possible as Independence Day data is finalized. Tight West Coast capacity, influenced by immigration enforcement, has driven California reefer rates (including frozen) to $1.13 per mile (48%) above last year’s levels despite the lower overall volumes.

Reefer Market Conditions

Reefer capacity saw further tightening last week, as equipment postings dropped 12% amid an intensifying seasonal surge prior to the July 4 holiday. Load volumes climbed 21% week-over-week—marking a 39% rise compared to last year—which pushed the load-to-truck ratio up by 37% to 24.89, nearly twice the level seen a year ago. Current availability remains acutely restricted, sitting 27% below last year and 48% under historical norms.