USDA Specialty Crops National Truck Rate Report | Week of May 13, 2026

The Big Picture

The baton has been passed — and South Texas grabbed it with both hands. After weeks of Florida dominating the rate narrative on the strength of Mother’s Day florals, RoadCheck-thinned capacity, and a tightening late-season load pool, this week’s report makes clear the market’s center of gravity has shifted south and west. South Texas posted the most dramatic rate moves in the entire report, with lanes surging +19% to +59% week-over-week — Boston cracked $13,000, Dallas hit $4,200–$4,600 after sitting below $3,000 just two weeks ago, and Los Angeles posted a +36% jump. The district is now at Shortage on every lane. Meanwhile, Florida held Shortage conditions for a third consecutive week with continued upward pressure, and the seasonal calendar delivered a meaningful structural shift: Santa Maria issued its first report of the season, officially broadening the California supply corridor as Salinas-Watsonville ramps volume. Nogales remained at Shortage with a Boston lane holding above $10,500. California overall was Adequate across all districts. The stage is set: South Texas is now the most expensive, highest-friction origin in the country, and any carrier not already positioned there is looking at significant repositioning costs.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Mexico Crossings Through South Texas — 🔴 Shortage (All Lanes)

This is the headline of the week. South Texas didn’t just tighten — it detonated. Every single lane is at Shortage, and the rate increases are the kind that make dispatchers stop and recalculate. The Boston lane at $13,000–$14,000 is a market-defining number. Dallas, which typically benefits from proximity, still jumped +57%. The Los Angeles lane — a westbound backhaul option for many carriers — surged +36% to $5,800–$6,400.

Two factors are driving this. First, Florida’s late-season load pool is contracting, and freight that previously originated in Florida is now routing through South Texas as the growing calendar shifts north. Second, the broader spring surge of Mexican commodity exports (watermelons, peppers, cucumbers) is hitting its peak volume window, creating a demand spike that available truck supply cannot absorb.

Central & South Florida — 🔴 Shortage (All Lanes)

Florida is now in its third consecutive week of Shortage conditions, and the USDA is reporting rate increases again after last week’s flatline — a signal that the ceiling established by the Mother’s Day floral cycle wasn’t the top. Rates are up modestly across all lanes, with Chicago posting the biggest jump at +15% and Atlanta adding +14%. The commodity mix is shifting toward watermelons and summer vegetables as the season winds toward its close. The critical question for next week: does the Florida load pool begin contracting materially as we pass mid-May, or does the region hold volume into late May before the traditional handoff to the Southeast?

Mexico Crossings Through Nogales, Arizona — 🔴 Shortage (Most Lanes)

Nogales held Shortage conditions across its major Northeast and Midwest lanes, with rates unchanged from the prior week — a flatline under tight conditions that typically signals the market is absorbing what it has rather than releasing. Dallas moved to Slight Shortage. No week-over-week percentage changes were published for most lanes, consistent with how USDA handles Shortage-condition pricing.

🆕 Santa Maria, California — FIRST REPORT of the Season | Adequate

Santa Maria’s first report of the 2026 season is a meaningful structural marker. This district — positioned between Oxnard to the south and Salinas-Watsonville to the north — fills in the California coastal corridor and adds supply-side depth at a moment when demand from the Northeast and Midwest is strong. Rates are Adequate and competitive, with no prior-week baseline to compare against on most lanes. Baltimore and Philadelphia, which have existing week-over-week data, came in at +8% and +4% respectively.

The Santa Maria opening, combined with Salinas-Watsonville ramping and Imperial/Coachella at full volume, means California is now running on all cylinders. For shippers in the Northeast, this broadens sourcing options heading into the early summer period.

Imperial/Coachella Valleys, Central & Western AZ, Calexico/San Luis — Adequate

Imperial/Coachella posted across-the-board gains with some of the more notable moves coming on East Coast lanes. Seattle jumped +35% — a standout in a region that’s been quiet — while Boston climbed +16% and Chicago +13%. The district remains Adequate, and the commodity mix (heavy on leafy greens and specialty items) is well-suited to the current Northeast demand profile.

Salinas-Watsonville, California — Adequate

Salinas posted mixed results this week — gains on the Northeast seaboard, softness on Chicago and Baltimore. New York jumped +13% and Philadelphia +9%, reflecting continued demand pull from the Northeast. Chicago fell -12% and Baltimore slipped -2%, consistent with a market where supply is meeting or exceeding demand on those lanes. No availability concerns — the district is firmly Adequate and well into its production ramp.

South & Central California — Adequate

Vegetables | Commodities: Anise, artichokes, avocados, bok choy, broccoli, Brussels sprouts, cabbage, cauliflower, celery, cilantro, grapefruit, greens, kale, lemons, lettuce (green leaf, iceberg, red leaf, romaine), radishes, spinach

Northeast lanes continued to strengthen — New York +11%, Philadelphia +12% — while Chicago softened by -10%. This pattern (Northeast strengthening, Midwest softening) has persisted across multiple California districts this week and reflects the demand geography of the current market.

Citrus lanes were broadly positive with Philadelphia leading at +12% and Boston up +6%. Chicago and Dallas held flat. The citrus mix now includes cherries — a seasonal arrival worth noting for shippers sourcing from this district.

Oxnard District, California — Adequate

Oxnard’s two reported lanes both posted gains — Baltimore +11%, Philadelphia +1%. The district continues to supply steady strawberry and specialty volumes into the Northeast corridor without any availability friction.

Kern District, California — Adequate

A mixed week for Kern: Baltimore posted +7% and New York +3%, while Chicago gave back -12%. The Chicago lane softness mirrors the pattern seen across California districts this week.

Vidalia District, Georgia — Adequate

Vidalia is in the heart of its pack season and rates are ticking higher across the board — every lane was up +2% to +7%, with New York leading at +7%. Atlanta held flat as a local near-haul. Los Angeles, the longest lane in the district, pushed to $5,000–$6,000 (+4%). The Vidalia season typically runs through late May; shippers sourcing for early summer should be pricing now.

Yakima Valley & Wenatchee, Washington — Adequate

Commodities: Apples, asparagus, pears, rhubarb

Yakima was the quietest origin in the report — nearly all lanes flat, with New York adding +2% and Miami +1%. The district remains a steady, low-friction supply source for the Pacific Northwest and Midwest corridors. No availability concerns.

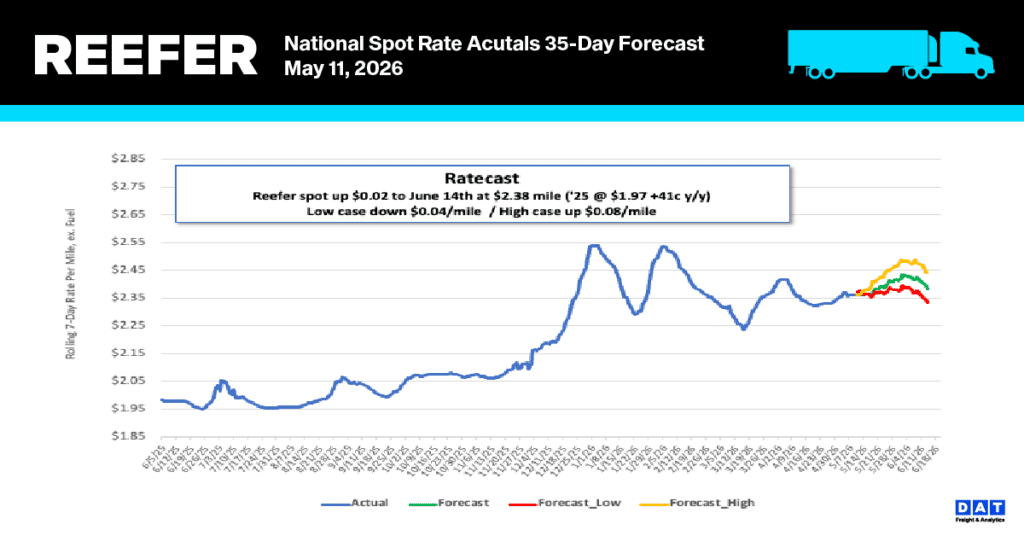

National reefer linehaul spot rates

For the past month, reefer linehaul rates have remained remarkably stable, fluctuating by no more than a cent and maintaining an average of $2.36 per mile last week. These spot rates for refrigerated transport remain at historically high levels across all temperature settings and products, even when fuel surcharges are excluded. Current figures show a significant increase compared to historical data, standing at 23% ($0.44) above last year’s rates and 20% ($0.47) higher than the five-year average, excluding the 2021-2022 pandemic peaks.

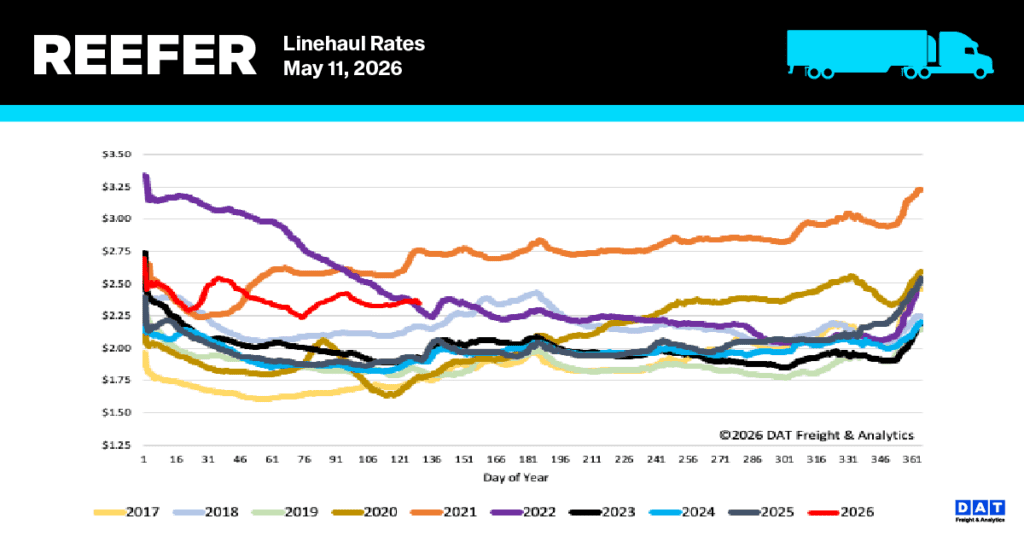

Truckload rates for fruit and vegetable shipments in key produce regions are averaging $3.55 per mile. This reflects a decrease of nearly $0.30 per mile over the past week, bringing rates to a level almost identical to the $3.56 per mile seen in early May of last year. According to the USDA, volumes have increased by 3.4% since last week and are currently about 6% higher than last year’s levels. Truck capacity has also stabilized, moving from a minor shortage to an adequate supply, mirroring conditions from the same period last May.

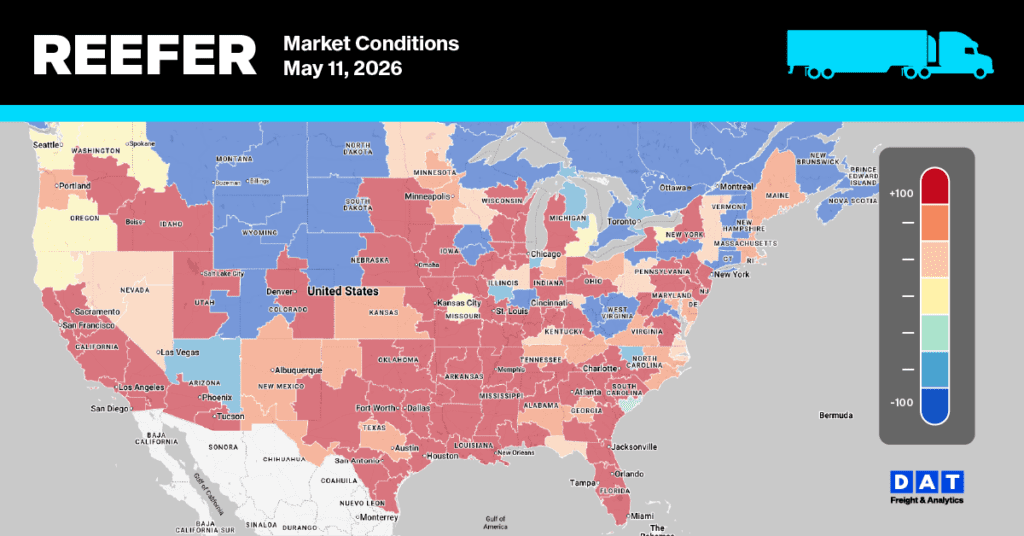

Reefer Market Conditions

Driven by a 3.4% rise in USDA produce volumes, reefer load posts increased by roughly the same amount last week as capacity tightens in anticipation of Mother’s Day and next week’s Roadcheck event. Conversely, equipment posts plunged by 10%, the lowest level this year leaving availability 30% below previous-year levels and 36% under the Week 19 long-term average as carriers face mounting regulatory and enforcement pressure. These shifting dynamics pushed the load-to-truck ratio up by 8% to 16.42.