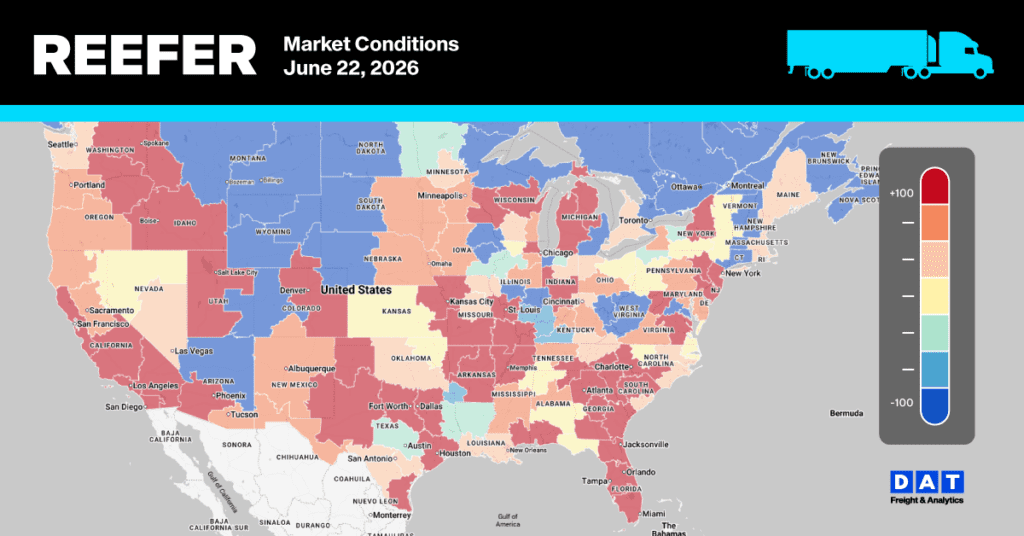

The baton just passed. Central & South Florida files its Last Report of the season, and in the same breath Georgia debuts as a First Report — both districts sitting at full Shortage truck availability. This is the seasonal handoff the eastern produce lanes have been building toward all month, and it arrives with zero rate relief: Georgia (which now folds in West and North Florida) opens at or above the rates Florida closed on across every eastern destination. Capacity east of the Mississippi stays tight.

Underneath the handoff, South Texas is tightening hard — the Laredo-to-Boston lane spiked +19% in a single week — exactly the overflow dynamic you’d expect as Florida’s load pool empties out and eastern demand goes looking for trucks. Vidalia onions firmed across the board after a flat stretch, and California’s navel orange season closed out, with the dedicated South & Central citrus block disappearing as the crop finishes ahead of July 4th. The Western veg districts, meanwhile, went dead flat. With July 4th now ~11 days out, the firming is concentrated in the eastern lanes — the first real sign the pre-holiday pull may finally be showing up in the data.

1. The Florida → Georgia handoff

Central & South Florida — LAST REPORT. Florida exits at Shortage availability with every lane flat on the week, capping a quiet, declining June (rates bled double digits the prior week). The spring shortage spike has fully unwound; the district goes out with tight trucks but soft rates.

Georgia — FIRST REPORT (includes West & North Florida) — tomatoes (incl. cherry, grape, plum) and watermelons, at Shortage availability. No prior-week comparison exists, but the open prices sit at or above Florida’s closing rates on every eastern lane — the handoff comes with no softening.

2. South Texas tightens — Boston lane spikes +19%

Laredo crossings firmed broadly as eastern demand redirected. The standout is South Texas → Boston at +19% — a large single-week move worth a DAT iQ cross-check before external distribution. LA and the Northeast lanes also ran hot.

The directional split is telling: long-haul eastern lanes firming, regional Dallas softening. South Texas absorbing Florida’s exit is the cleanest cross-region read on the board.

3. Vidalia onions firm across the board

After a fully flat prior week, Vidalia woke up — peak summer pack season is in full swing and rates ticked up on nearly every lane, led by the I-95 corridor.

4. California: Western flatlines and the navel orange close

New this week: the dedicated South & Central California citrus block (grapefruit, lemons, oranges) dropped off entirely. Last week it ran as a separate Slight Shortage program across 9 destinations; this week oranges fall out of the basket and the citrus lanes are gone. The driver is the navel orange close — the California navel crop is over 90% harvested and finishing right around July 4th, with the industry transitioning to Valencias and lemons for the summer. Note that grapefruit and lemons remain in the basket, so this is a navel handoff, not a full citrus exit. The vegetable/avocado mix continues at Adequate.

The Western veg districts are essentially frozen — a near-total flatline after last week’s broad declines, with only the Northeast lanes firming a point or two.

- Imperial/Coachella: every lane flat (e.g., → New York $10,900–$11,900, → Boston $11,500–$12,400). Total flatline.

- Salinas-Watsonville: → New York $11,500–$12,500 (+2%); → Philadelphia $11,500–$11,900 (+1%); Baltimore/Chicago flat.

- South & Central CA (veg): → New York $11,300–$12,200 (+2%); → Philadelphia $11,300–$11,800 (+1%); Baltimore/Chicago flat.

- Santa Maria: all lanes flat (→ Boston $10,400–$12,400, → Baltimore $11,000–$11,500). Note: the Santa Maria → New York lane dropped off this week.

- Kern (carrots): → Philadelphia $11,100–$11,600 (+1%); Baltimore/Chicago/NY flat.

- Oxnard: → Philadelphia $11,100–$11,600 (+1%); → Baltimore $10,700–$11,500 (flat).

5. Nogales slides on a commodity-mix shift

Nogales ranges slipped lower across the board, but USDA suppressed the week-over-week % — the basket changed (cucumbers, grapes, and grape tomatoes dropped out; honeydews, mangoes, and round/plum tomatoes remain). Treat these as directional, not as published % moves.

6. Yakima: Flat, cherries rolling

Yakima/Wenatchee held at Slight Shortage with every lane flat. Apple, cherry, blueberry, and pear movement steady. The in-region Seattle haul stays tiny ($950–$1,100). No story here this week beyond stability.

Watch items

- Dallas cooled from multiple origins this week (Nogales → Dallas down to $3,100–$3,300; South Texas → Dallas −7%), undercutting last week’s World Cup host-city firming signal. Not showing in the truck data right now.

- July 4th pull appears to be concentrating in eastern long-haul lanes (South Texas, Vidalia, CA → NY) rather than broadly — the first hint the holiday surge is materializing.

What this means for carriers, shippers, and brokers

Carriers: The money this week is east and long-haul. South Texas → Boston (+19%), → LA (+11%), and → Philly (+6%) are the lanes to chase, and the Florida-to-Georgia handoff means Shortage-tight capacity on Georgia tomatoes and watermelons — you have pricing power on anything moving out of the Southeast into the I-95 corridor. Don’t deadhead into Dallas expecting strength; it softened from several origins. If you’re running California veg, accept that the West is flat — reposition east rather than waiting for Western rates to move.

Shippers: Florida is officially closed; your tomato, pepper, and watermelon capacity now sources from Georgia/North Florida at Shortage availability and higher opening rates than Florida’s exit. Book Georgia lanes early — there’s no slack and no rate relief in the transition. Vidalia onion lanes firmed up to +7%, so lock onion freight now before peak-season demand pushes further. Western veg out of California and Arizona is your one pocket of stability — rates are flat and trucks are Adequate.

Brokers: The arbitrage is in the regional shift. Florida’s empty load pool is pushing eastern demand onto South Texas and Georgia — margin lives in covering the Boston and Northeast spikes before they normalize. Treat the +19% South Texas → Boston move as unconfirmed until you cross-check it against DAT iQ; pricing a customer off a single-week anomaly is risk. California’s flatline gives you a stable baseline to quote against, and with the navel orange crop closing out, lingering CA orange inquiries should redirect to Valencia/lemon programs, imports, or Texas sourcing. Watch the eastern lanes into next week — if the July 4th pull broadens, the Georgia and South Texas firming has room to run.

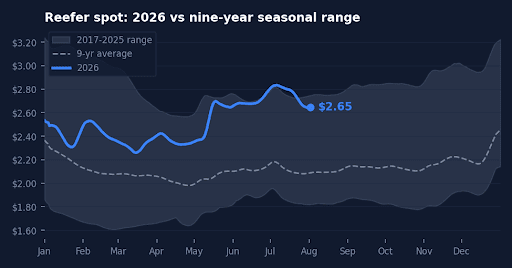

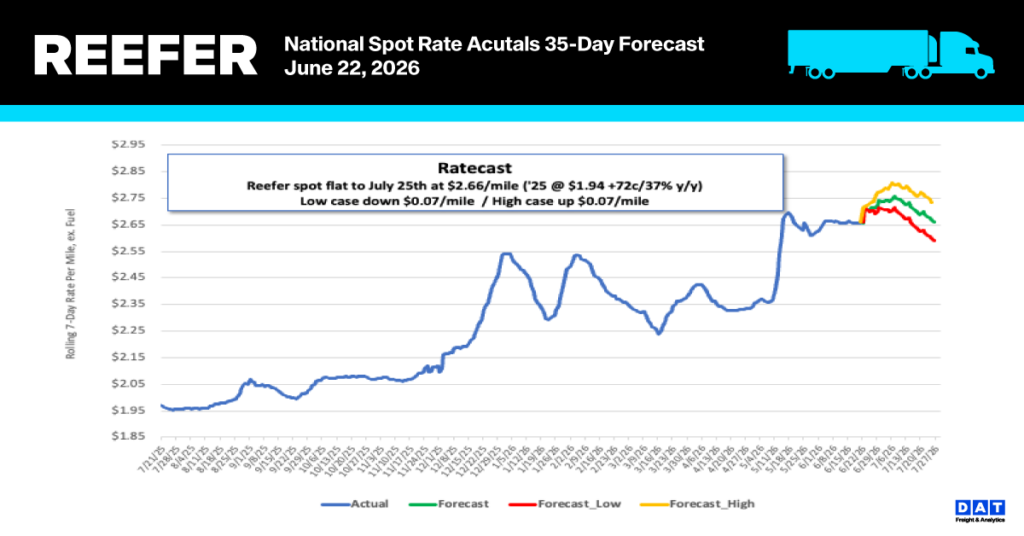

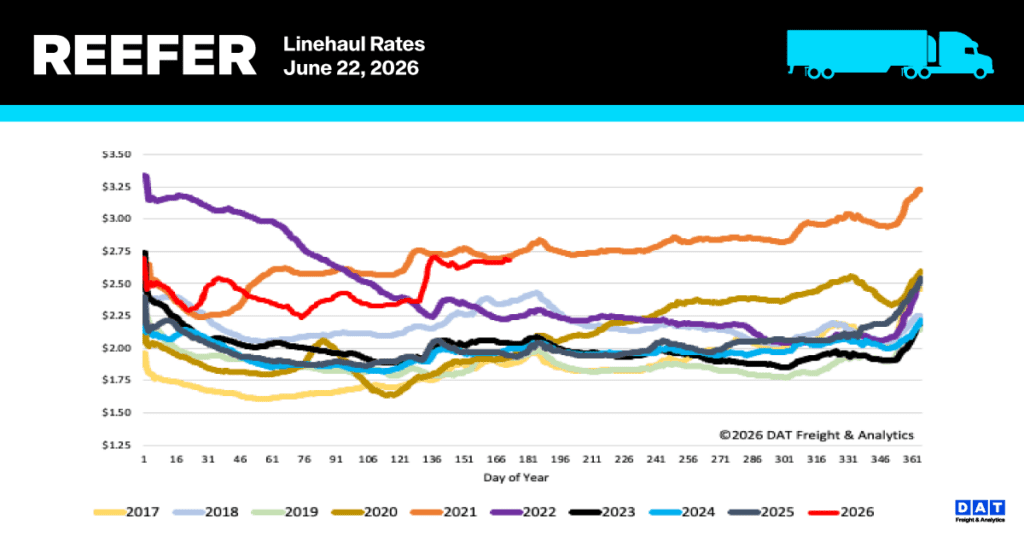

Spot rate trends: national reefer market

National reefer linehaul rates remained stagnant for the third consecutive week, an unusual trend for the period preceding the July 4 holiday. The 7-day rolling average held steady at $2.68 per mile, maintaining the record gains achieved during Roadcheck Week. Present reefer spot rates sit 38% ($0.74) higher than previous year levels and are 26% ($0.70) above the non-pandemic five-year average. Last week’s performance brought the rate within $0.03 of the Week 25 record set in 2021.

- Bellwether States (IL, IN, TX, OH, TN, WI, AR, KY, MO, PA): As capacity restrictions loosened on major routes, rates in this critical 13-state market—which represents nearly 50% of national load volume—dropped by $0.04 to an average of $2.72 per mile. The reefer bellwethers aren’t the big produce states — they’re the year-round food engine rooms: Wisconsin dairy, Arkansas poultry and protein, and the food and beverage processors of the Midwest and Texas. That freight runs all year instead of spiking with a harvest, so it tracks the national reefer market far better than seasonal produce.

Regional produce highlights

In major produce hubs, spot rates for fruits and vegetables currently average $3.98 per mile. While this reflects a week-over-week dip of roughly $0.11, it is still $0.48 higher than the same time last year. California’s produce season is accelerating, with USDA volumes rising 5% last week to match last season’s output. As a result, California truckload rates have reached $1.05 per mile (44%) above last year’s figures.

Reefer Market Conditions

Equipment availability continued to contract last week, with reefer postings falling by 10% as the seasonal demand spike ahead of the July 4 holiday intensified. Current capacity levels are significantly suppressed, trailing last year by 24% and historical averages by 41%. Meanwhile, load volumes rose 2% over the previous week—a 57% year-over-year increase—driving a 13% surge in the load-to-truck ratio to 18.63.