Data ending week of April 21, 2026 for truckload produce carriers & brokers

The big picture

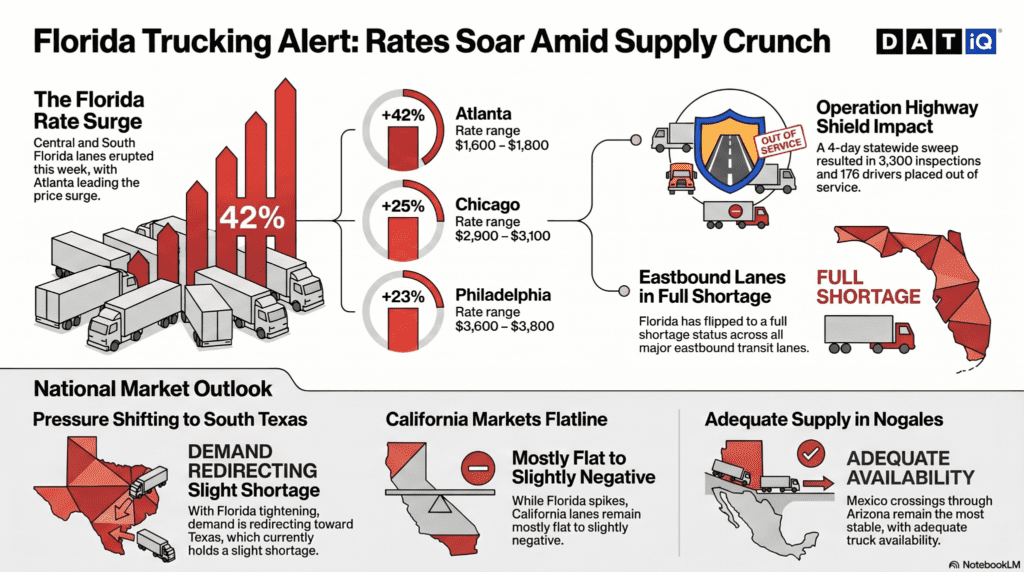

Florida just broke. Central and South Florida flipped to full Shortage status across every eastbound lane this week — the most significant single-week market move in this report so far in 2026. Rates didn’t creep higher; they erupted. Atlanta jumped 42%. Chicago climbed 25%. Philadelphia surged 23%. Baltimore gained 17%. New York added 14%. This is what a late-season supply crunch looks like in real time: the Florida produce window is narrowing fast, loads are concentrating, and trucks have better options elsewhere. When a market goes from Adequate or Slight Shortage to full Shortage in a single week, it’s not a blip — it’s a signal that the season is ending earlier than capacity planned for.

The recent Florida Department of Law Enforcement (FDLE) 4-day statewide sweep called Operation Highway Shield is a warning sign of what’s to come in May. It resulted in 3,300 inspections, 176 drivers placed out of service, and 35 arrests. Key issues found included 54 drivers with language deficiencies and 42 referrals to ICE.

The ripple effect to watch is South Texas. Already sitting at Slight Shortage with northbound lanes ticking higher on Atlanta (+2%) and Chicago (+4%), South Texas is the logical destination for demand that can no longer be filled out of Florida. If Florida’s load pool continues to shrink over the next two to three weeks, expect South Texas rates to follow with meaningful upward moves. California, meanwhile, is holding steady in Slight Shortage territory across most coast districts, but rates are drifting slightly negative — a sign that spring supply is catching up to demand. No single California market is breaking out. The story this week is entirely east of the Mississippi.

Central & South Florida — Shortage

Florida’s commodity mix remains broad heading into the season’s final stretch: beans, broccoli, cabbage, celery, corn, lettuce (romaine and other), okra, peppers, squash, strawberries, tomatoes of all types, and watermelons. That’s a deep load pool — which makes the Shortage designation more striking, not less. This isn’t a thin market running dry. It’s a tightening market where trucks are pricing their optionality.

- Florida → Atlanta: $1,600–$1,800 (+42%) load posts +17% w/w, reefer spot +10% w/w

- Florida → Chicago: $2,900–$3,100 (+25%) reefer spot +25% w/w

- Florida → Philadelphia: $3,600–$3,800 (+23%) load post +33% w/w

- Florida → Baltimore: $3,300–$3,500 (+17%)

- Florida → New York: $3,900–$4,100 (+14%) load posts +34% w/w, reefer spot +24% w/w

- Florida → Boston: $4,500–$4,700 (no change reported)

Mexico crossings through South Texas — Slight Shortage

South Texas is running a full commodity slate: asparagus, broccoli, carrots, cucumbers, grapefruit, limes, oranges, peppers across every variety, pineapples, tomatillos, tomatoes, and watermelons. Slight Shortage conditions are holding firm, and the market is showing early signs of building pressure. Atlanta and Chicago — the two lanes most likely to absorb redirected Florida demand — both moved higher this week. The rest of the board held flat. That’s not stagnation; that’s a market that knows something is coming.

- South Texas → Atlanta: $5,400–$6,200 (+2%)

- South Texas → Chicago: $5,400–$5,800 (+4%)

- South Texas → Baltimore: $8,200–$8,600 (+2%)

- South Texas → Boston: $8,800–$9,200 (flat)

- South Texas → New York: $8,600–$9,000 (flat) reefer spot +47% y/y

- South Texas → Philadelphia: $8,400–$8,800 (flat)

- South Texas → Dallas: $2,600–$2,800 (flat)

- South Texas → Los Angeles: $4,600–$5,200 (flat) reefer spot +52% y/y

- South Texas → Miami: $6,000–$6,400 (flat)

Salinas-Watsonville, California — Slight Shortage

Salinas continues its Slight Shortage status as the spring coast season builds. Commodity mix includes broccoli, cauliflower, all varieties of lettuce, and strawberries. Rates softened modestly across all four reported lanes this week — the Yuma-to-Salinas lettuce transition is underway, and supply is keeping pace with demand for now. The New York lane continues to brush against the $10,000 threshold at the top of its range, which is worth watching as the season progresses.

- Salinas → New York: $9,800–$10,500 (-3%) reefer spot +45% y/y

- Salinas → Chicago: $6,000–$7,300 (-2%) reefer spot +43% y/y

- Salinas → Baltimore: $9,000–$10,100 (-2%) reefer spot +46% y/y

- Salinas → Philadelphia: $9,500–$10,400 (-1%) reefer spot +41% y/y

Kern District, California — Slight Shortage

Kern is a single-commodity story this week: carrots. Slight Shortage conditions persist, and rates were flat across three of four lanes. The Philadelphia lane pulled back 5%, the only meaningful move in the region.

- Kern → New York: $9,700–$10,400 (flat)

- Kern → Chicago: $5,900–$6,600 (flat)

- Kern → Baltimore: $8,500–$8,900 (flat)

- Kern → Philadelphia: $8,600–$9,500 (-5%)

Oxnard District, California — Slight Shortage

Oxnard is shipping celery, cilantro, greens, kale, parsley, and strawberries under Slight Shortage conditions. The Baltimore lane pulled back 8% this week — the steepest single-lane decline in the California region — while Philadelphia was essentially flat. Two lanes aren’t enough to call a trend, but a move that size on a Slight Shortage market is worth flagging.

- Oxnard → Baltimore: $7,900–$8,200 (-8%)

- Oxnard → Philadelphia: $9,400–$10,200 (-1%)

Santa Maria, California — Slight Shortage

Santa Maria’s mix — broccoli, cauliflower, celery, lettuces, and strawberries — held at Slight Shortage with rates essentially unchanged. The Baltimore lane edged up 1%; Philadelphia was flat. One of the quieter markets in this week’s report.

- Santa Maria → Baltimore: $8,700–$9,400 (+1%)

- Santa Maria → Philadelphia: $9,000–$9,500 (flat)

South & Central District California + Imperial/Coachella Valleys — Slight Shortage

The broadest California commodity region — artichokes, avocados, broccoli, Brussels sprouts, cauliflower, celery, citrus (grapefruit, lemons, oranges), greens, kale, lettuces, radishes, spinach — is holding at Slight Shortage with rates largely unchanged. The New York lane slipped 1%; everything else flatlined. California citrus lanes reported this week without percentage changes, suggesting stable conditions as the citrus season continues its gradual wind-down.

- South/Central CA → New York: $9,800–$10,200 (-1%)

- South/Central CA → Chicago: $6,100–$6,900 (flat)

- South/Central CA → Baltimore: $9,400–$10,000 (flat)

- South/Central CA → Philadelphia: $9,400–$10,000 (flat)

Mexico crossings through Nogales, Arizona — Adequate

Nogales is moving beans, cucumbers, eggplant, honeydews, peppers, all varieties of squash, tomatoes, and watermelons under Adequate truck supply — the loosest conditions of any produce origin this week. The board was mixed: Chicago dropped 6%, Boston fell 3%, but Dallas jumped 6% and Los Angeles gained 5%. The divergence between northbound softening and southbound/westbound gains likely reflects seasonal routing shifts as summer produce volumes begin their directional realignment.

- Nogales → Chicago: $5,600–$6,000 (-6%) reefer spot +31% y/y

- Nogales → Boston: $9,000–$9,200 (-3%)

- Nogales → New York: $8,600–$8,800 (-1%) reefer spot +43% y/y

- Nogales → Baltimore: $8,000–$8,300 (-1%)

- Nogales → Dallas: $4,000–$4,200 (+6%) reefer spot +43% y/y

- Nogales → Los Angeles: $1,900–$2,300 (+5%)

- Nogales → Atlanta: $5,200–$5,400 (+2%)

- Nogales → Philadelphia: $8,500–$8,700 (+2%)

Yakima Valley & Wenatchee, Washington — Slight Surplus

Yakima and Wenatchee are running apples, asparagus, pears, and rhubarb under Slight Surplus conditions — the only true oversupply situation in this week’s report. Every lane came in flat with no percentage change reported. Truck supply is outpacing load demand here, which creates a backhaul opportunity for carriers already positioned in the Midwest or Pacific Northwest.

- Yakima/Wenatchee → Chicago: $5,200–$5,700 (flat)

- Yakima/Wenatchee → New York: $8,100–$8,700 (flat)

- Yakima/Wenatchee → Atlanta: $7,200–$7,800 (flat)

- Yakima/Wenatchee → Dallas: $5,800–$6,300 (flat)

- Yakima/Wenatchee → Miami: $8,600–$9,200 (flat)

- Yakima/Wenatchee → Baltimore: $7,900–$8,500 (flat)

- Yakima/Wenatchee → Philadelphia: $7,800–$8,500 (flat)

- Yakima/Wenatchee → Los Angeles: $2,500–$2,800 (flat)

- Yakima/Wenatchee → Boston: $8,600–$9,200 (flat)

- Yakima/Wenatchee → Seattle: $1,100–$1,200 (flat)

San Luis Valley, Colorado + New York — Adequate

Colorado potatoes (Atlanta, Baltimore, Boston, Dallas) and New York apples (Atlanta, Boston, Miami, New York, Philadelphia) both reported flat rates week-over-week under Adequate truck supply. No movement, no story — steady background markets.

What this means for carriers, shippers, and brokers

Carriers: Florida is your rate story this week, and it demands action. Shortage conditions mean you have negotiating leverage. Mother’s Day floral volumes begin next week and after the recent safety and immigration blitz, trucks are going to be more scarce than usual in Miami. South Texas is quiet but building; if you have flexibility on positioning, getting into the South Texas market ahead of the Florida overflow could pay off over the next two to three weeks. California’s mild rate softening in most Slight Shortage markets is a sign that spring supply is catching up — don’t expect California to carry the week the way Florida is right now. And avoid deadheading into Yakima; Slight Surplus means trucks are already competing for loads there.

Shippers: If you’re moving produce out of Florida, book capacity now. The market went to full Shortage in one week, and it is not going to get easier as the season winds down. Waiting for rates to soften is not a strategy right now — it is a risk. California shippers across Salinas, Santa Maria, Kern, and Oxnard have a window: supply is keeping up with demand and rates are flat to slightly lower. Use that stability to lock in capacity before summer volumes hit. South Texas shippers should start factoring in upward rate pressure; if Florida’s load pool keeps shrinking, the redirected demand has to land somewhere.

Brokers: Florida to northeast lanes are where you need to recalibrate immediately. If you’re holding committed capacity at last week’s rates, your margin structure just changed — the market moved 14% to 42% in a single week. The recent Florida Department of Law Enforcement (FDLE) massive 4-day statewide sweep is a warning sign of what’s to come ahead of Roadcheck Week and Mother’s Day – Operation Highway Shield conducted 3,300 inspections, 176 drivers placed out of service, and 35 arrests. Key issues found included 54 drivers with language deficiencies and 42 referrals to ICE. South Texas outbound is steady for now, but the Atlanta and Chicago signals (+2% and +4%) suggest that the market is aware of what’s coming. Build your positions accordingly. California is in a mild retreat; don’t lock in forward capacity at current levels if the softening continues. Yakima Slight Surplus gives you a card to play if you have Midwest-positioned carriers looking for backhaul loads out of the Pacific Northwest.

Source: DAT iQ | USDA AMS Specialty Crops National Truck Rate Report, April 22, 2026. Rates represent open (spot) market per-load prices including broker fees for 48–53 ft. refrigerated trailers. Percentage changes vs. April 14, 2026.