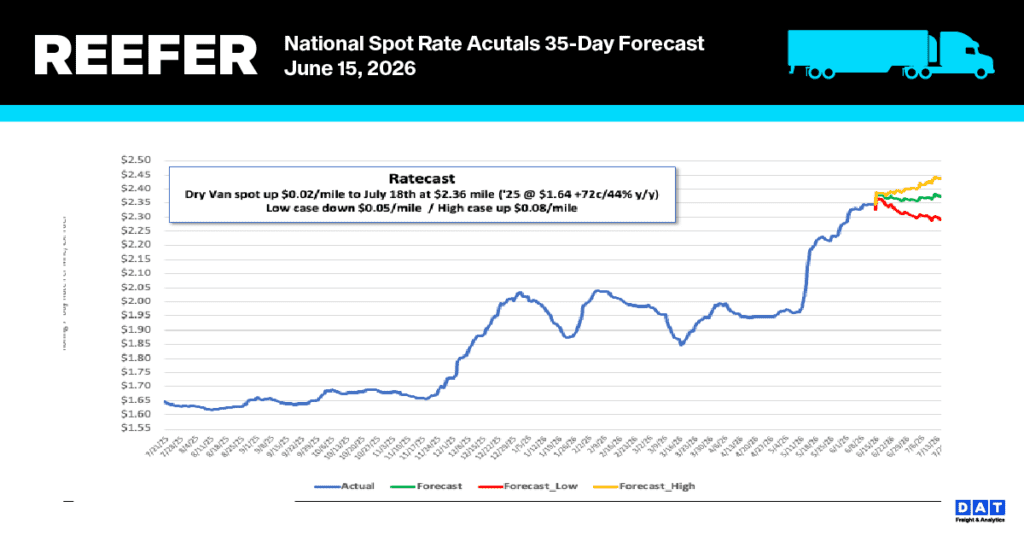

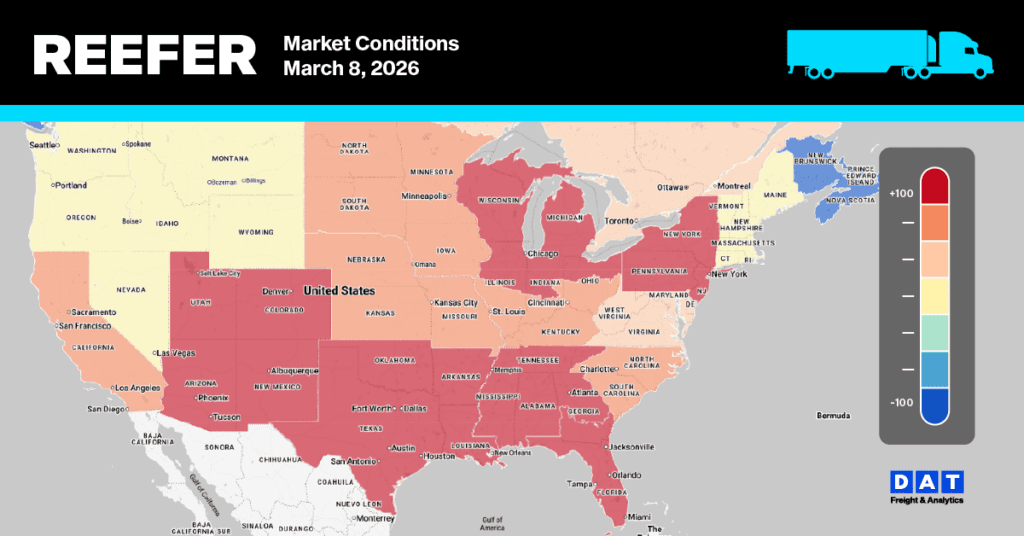

The Big Picture

For the first time in weeks, every single origin in the USDA report is showing Adequate truck availability. No Shortages. No Slight Shortages. The capacity tightness that defined California, Florida, and South Texas over the past month has fully unwound. Florida rates continue falling — now in their fourth consecutive week of declines — while Nogales flipped higher on key lanes, South Texas firmed modestly, and California settled into a stable holding pattern. The produce reefer market just hit a reset.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Florida: Fourth straight week of declines

Central and South Florida’s slide shows no signs of stopping. Truck availability has eased to Adequate (down from Slight Shortage last week), and rates dropped again across every destination.

That Lakeland, FL to Atlanta lane at $1,050–$1,250 is remarkably soft, but still paying carriers around $100 per load more than a year ago based on DAT 7-day rolling average rates. Reefer load posts to Atlanta also dropped 12% this week.

For context, this lane was $2,100–$2,300 just four weeks ago. The weather-damaged crop supply continues to shrink the available load pool faster than capacity can tighten — fewer loads, lower rates, even as product scarcity deepens. DAT Rateview 7-day average outbound Lakeland, FL reefer rate to all destinations, dropped $0.12 per mile (7.4%) last week, but remained 14% higher than last year.

Nogales: The bounce-back

After three weeks of softening, Mexico crossings through Nogales posted a mixed-to-higher week — led by a +15% surge to Atlanta ($5,700–$5,900). Dallas also firmed +3%. Meanwhile, Baltimore (-3%), Chicago (-4%), and Philadelphia (-3%) continued to ease. Boston ticked up +1%, and LA held flat.

The Atlanta spike is notable — this was the weakest Nogales lane just two weeks ago at -7%. Likely reflects repositioning dynamics as carriers pull away from soft Florida loads and shift toward Nogales freight. Loads paying carriers $5,700-$5,900 last week are around $1,000 higher than a year ago, based on DAT Rateview data. Reefer load posts on this lane are also up, increasing by 37% this week.

South Texas: Modest firming, broad commodity mix

South Texas rates firmed slightly on most lanes after last week’s tightening. Truck availability eased back to Adequate across the board (down from Slight Shortage on five lanes last week), but rates held or inched higher, up $0.05 per mile last week to an average of $2.91 per mile in McAllen.

The recent 14% surge on the McAllen to Los Angeles lane appears to be holding, with reefer load posts up 17% this week and rates remaining between $4,400 and $4,800. Carriers operating this lane have been earning approximately $1,200 more than they did last year at this time, a trend that began in September following increased immigration enforcement activities along the southern border. This enforcement has resulted in California-based carriers, which supply much of the westbound capacity, becoming increasingly hesitant to leave their state for loads near the border.

California: All adequate, stable rates

The big shift: every California region moved to Adequate truck availability this week, completing the transition from Shortage → Slight Shortage → Adequate over the past three weeks. Rates are stable to slightly higher (+1% on most eastbound lanes), reflecting a market that has found its level.

California citrus showed continued softening: Atlanta -4%, Dallas -5%, Baltimore -4%. Boston and Chicago held flat. Seattle ticked up +3%. The citrus market remains well-supplied with no capacity pressure.

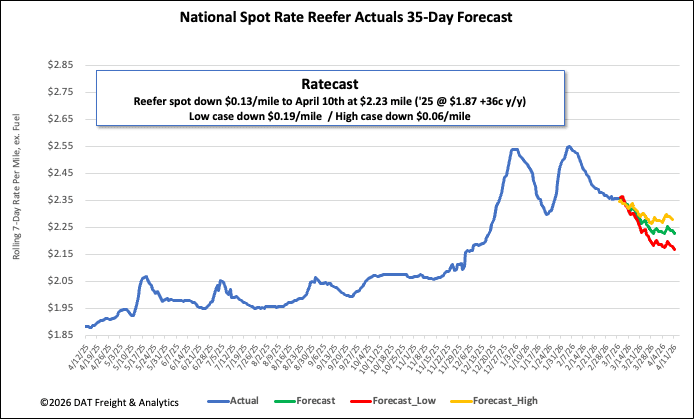

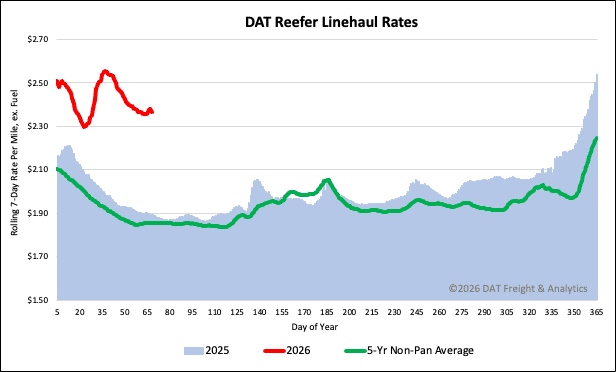

National reefer linehaul spot rates

The national average reefer spot rate (excluding fuel) has dropped to $2.38 per mile, a $0.03 per mile decline from last week. This recent drop brings the rate perilously close to erasing all the gains realized during last months Winter Storms Fern and Gianna. Despite marking the fourth consecutive weekly decrease for a total drop of $0.19 per mile, the current average reefer linehaul rate remains significantly elevated compared to the same time last year, sitting $0.47 per mile (25%) higher. Furthermore, the rate is $0.51 (22%) above the five-year average, excluding the years of 2021 and 2022.

Reefer Market Conditions

Despite reefer volumes remaining 60% higher than last year, the sector is cooling, evidenced by a 10% drop in load posts during the first shipping week of March. This decreased demand, coupled with a 7% decline in reefer equipment posts, resulted in a 3% drop in the load-to-truck ratio, which is now 14.87.