The Big Picture

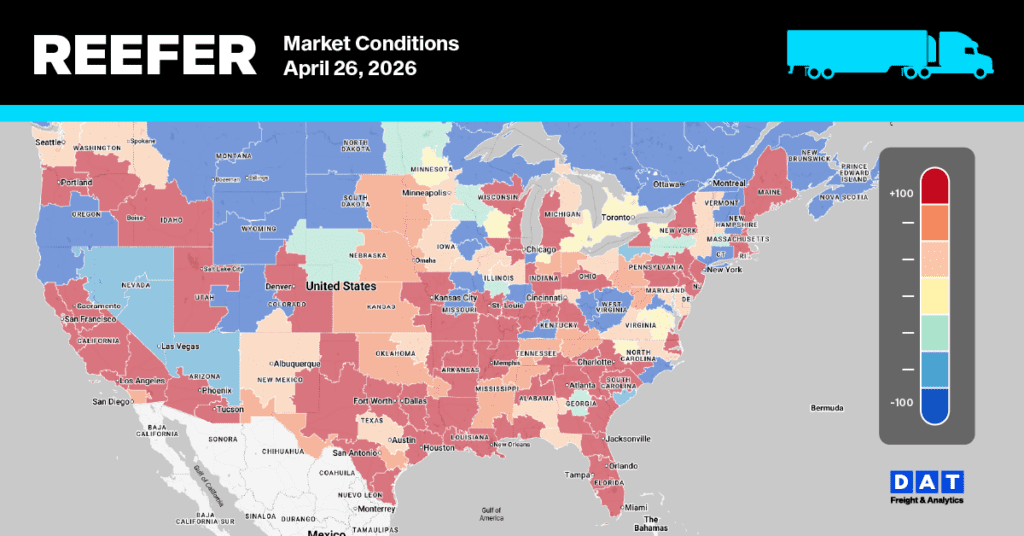

Florida didn’t cool off — it doubled down ahead of Mother’s Day. Central and South Florida remained at full Shortage for the second consecutive week, and this week the New York lane exploded 35%, pushing to $5,300–$5,500. Boston jumped 20%. Chicago gained 13%. Philadelphia surged 19%. Baltimore added 12%. Atlanta, already the highest-percentage mover last week at +42%, added another 6% on top. Two straight weeks of Shortage conditions with accelerating rates on key northbound lanes is no longer a signal — it’s a trend, and the Florida season has weeks left to run.

The surprise this week is South Texas, which moved in the wrong direction — and USDA import volume data explains why. Mexico import volumes were down 6% last week and are running 6% below the YTD pace. South Texas specifically saw volumes fall 11% week-over-week. Avocados led the drop at 47% w/w. Fewer loads crossing the border meant trucks had more options, and rates on long-haul lanes fell hard: Boston down 28%, Baltimore down 16%, Philadelphia down 14%, New York down 11%, Miami down 13%. The Slight Shortage designation held, but the rate board is telling a volume story, not a capacity story. The key question for next week is whether Mexico import volumes — and avocados specifically — recover. If they do, South Texas rates can firm just as fast as they fell.

Three seasonal milestones hit this week. The Vidalia District in Georgia filed its first report of the season — Vidalia onions are officially at market under Adequate truck supply. And New York apples filed their last report of the season, closing out the storage apple chapter. Meanwhile, Imperial/Coachella Valleys filed their first report of the spring season at Slight Shortage across all lanes — a new origin coming online with immediate tightness. The California coast continues its Slight Shortage flatline. Nogales loosened, with several lanes shifting to Slight Surplus. Yakima improved from Slight Surplus to Adequate. The board is rotating.

What this means for carriers, shippers, and brokers

Carriers: Florida is now a two-week Shortage with accelerating rates — and the New York lane at $5,300–$5,500 is the headline number this week – Miami to New York loads are 28% higher than last year. If you’re running Southeast-to-Northeast corridors, you have real pricing power right now. Mother’s Day floral volumes are adding pressure in the Miami market on top of the ongoing enforcement hangover from Operation Highway Shield. Don’t leave money on the table on Florida northbound lanes. South Texas rate declines this week are explained by a real volume drop — Mexico imports down 6% last week and South Texas specifically down 11% w/w, with avocados off 47% — so don’t read the rate pullback as a structural loosening. If import volumes recover, those lanes can firm quickly. Imperial/Coachella opening at Slight Shortage is a new load source to add to your California routing calculus. Yakima moving from Surplus to Adequate means the backhaul play from last week has tightened up.

Shippers: Florida shippers are now two weeks into Shortage conditions with no relief in sight before the season winds down. The New York lane jumped 35% in a single week — if you haven’t locked in capacity on northeast lanes, you are now paying a significant premium over what was available two weeks ago. The Vidalia onion pack is underway out of Georgia, which adds a new load source to the Southeast. South Texas shippers got a brief reprieve on long-haul lane rates this week, but it’s driven by a volume drop — Mexico imports down 6%, South Texas down 11% w/w, avocados down 47% — not by structural loosening. If those volumes recover next week, the rate relief disappears with them. California shippers across all coast districts are looking at a stable-to-flat rate environment — use it.

Brokers: Two weeks of Florida Shortage with rates still climbing means your coverage costs have risen materially since April 14. The cumulative move on the New York lane — up roughly 55% in two weeks — is the kind of shift that exposes any broker holding fixed-rate commitments. Reprice now or manage your exposure carefully. The South Texas pullback is now explained: USDA data shows Mexico import volumes down 6% last week and South Texas down 11% w/w, with avocados cratering 47%. This is a volume-driven rate correction, not a capacity surge — which means it can reverse fast if imports normalize. Don’t build a forward position in South Texas based on this week’s rates without first tracking whether that import volume recovers. Imperial/Coachella’s first report at Slight Shortage is a market to watch; first reports at tightness tend to firm as the season builds. Vidalia’s entry adds a new Southeast origin to track weekly. And note the New York apple last report — that load source is gone for the season.

National reefer linehaul spot rates

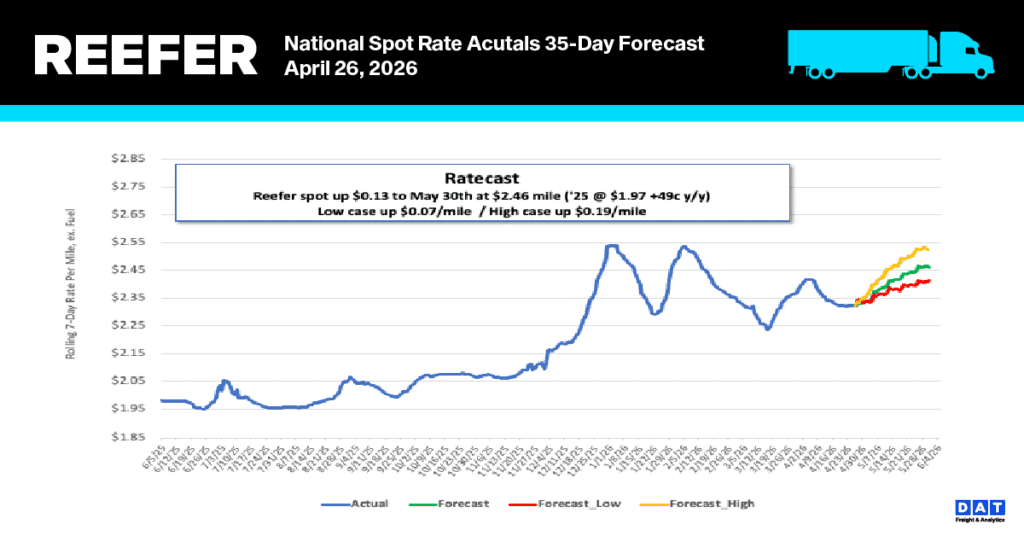

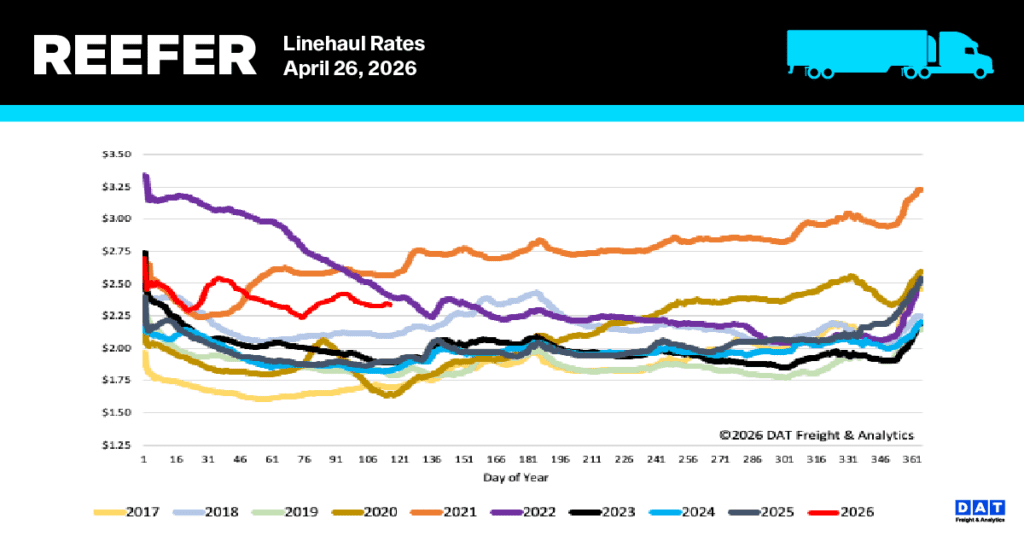

Reefer linehaul rates recently leveled off at an average of $2.35 per mile, following a $0.05 per mile drop over the preceding three weeks. Despite this minor decline, current reefer spot rates (excluding fuel) remain historically high. They are presently $0.44 (23%) higher than the rate from last year and $0.53 (23%) above the five-year average, excluding the exceptionally high-rate periods seen in 2021 and 2022.

Reefer Market Conditions

Despite a slight (1%) drop in load post volumes last week, the reefer market saw capacity tighten. The primary driver was a 7% decline in equipment posts, which caused the load-to-truck ratio to increase by 6% to 13.22. Equipment posts are now 13% lower than last year and nearly 50% below the long-term average (excluding the pandemic-affected years of 2021 and 2022). Meanwhile, domestic produce truckload volumes were flat last week and remain 15% behind last year’s total for the first four months of the year.