All rates cited below exclude fuel surcharges, and load volume refers to loads moved unless otherwise noted. The rate charts exclude 2021 and 2022 years influenced by the pandemic. Data analysis for the week ending Saturday, May 2nd, 2026.

The U.S. trucking industry is showing significant signs of resilience as we move through the first quarter of 2026. According to the latest data from the American Trucking Associations (ATA), the seasonally adjusted For-Hire Truck Tonnage Index rose 0.3% in March, following a substantial 2.9% surge in February. While the monthly gain was modest, the bigger picture reveals a major recovery: March saw the largest year-over-year increase since October 2022, with tonnage climbing 3% compared to the same month last year.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

ATA Chief Economist Bob Costello noted that the first quarter of 2026 represents the industry’s strongest performance in nearly a decade when weighing both sequential and annual results. In March, the index reached 117.0, a clear step up from the previous month’s 116.6. These figures suggest that the “freight recession” of previous years is firmly in the rearview mirror, as the first three months of the year have already outpaced 2025 levels by 2.1%.

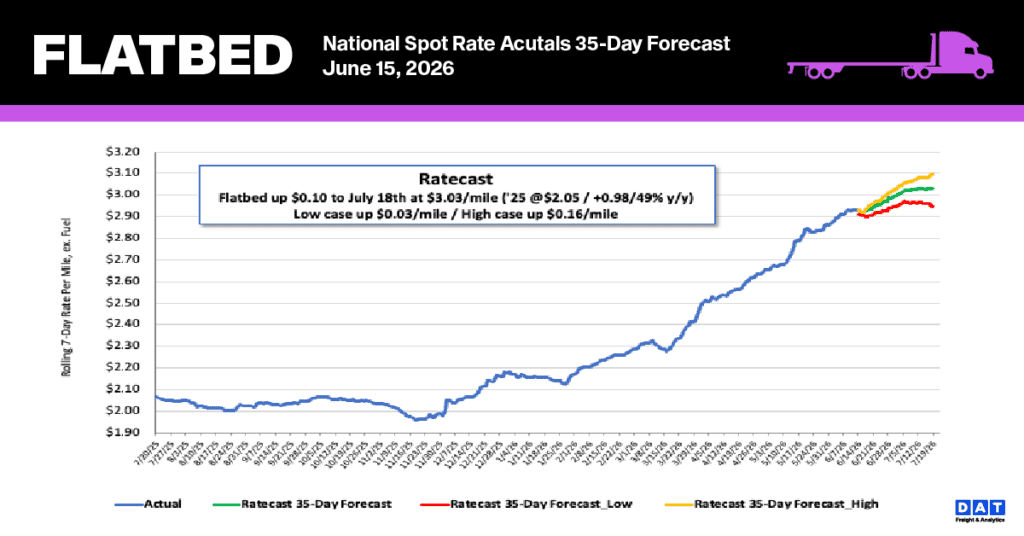

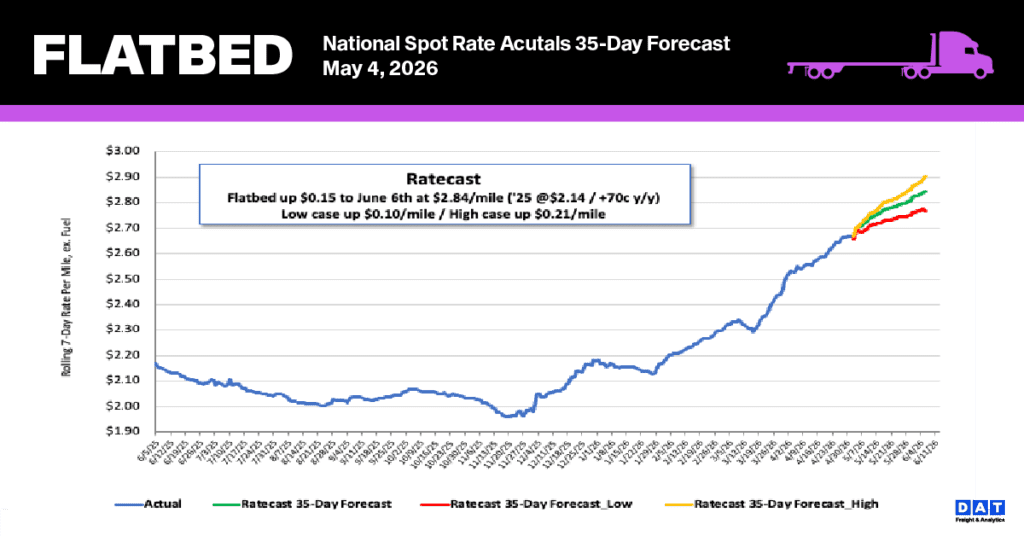

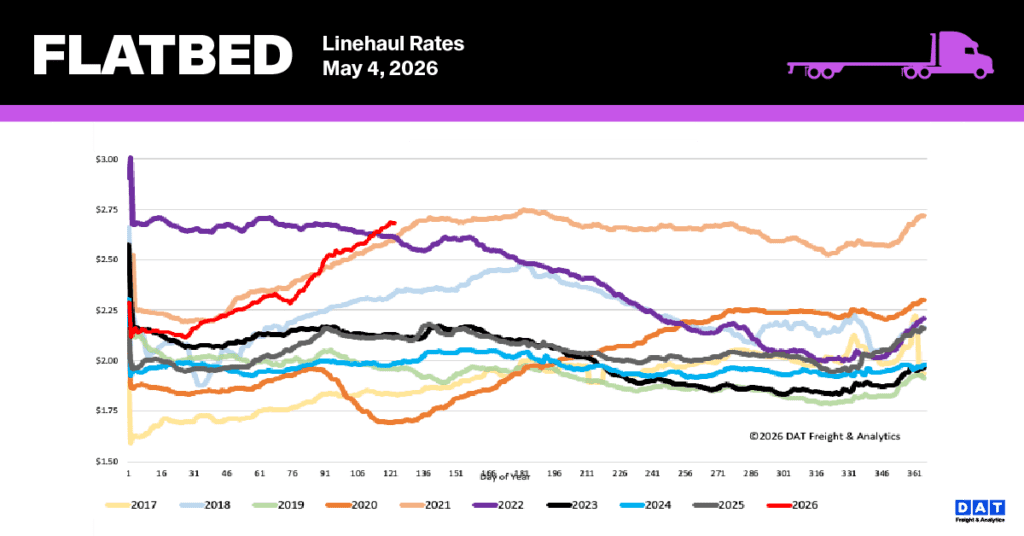

National flatbed linehaul spot rates

Flatbed spot rates continue a significant, sustained rise, culminating in a new high of $2.69 per mile in Week 18, an increase of $0.03 from the previous week. This seven-week growth streak has added a total of $0.38 to the national average, bringing it within $0.05 of the all-time record set in late June 2022. The current rate is notably elevated compared to historical figures. It is $0.57 (27%) higher than the rate during the same period last year and surpasses the five-year average (excluding pandemic years) by $0.71 (26%).

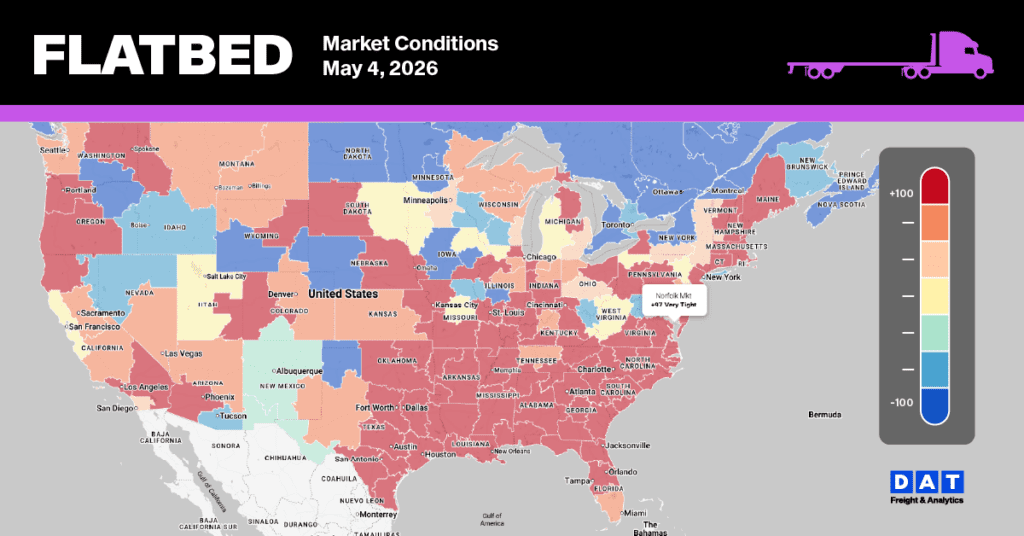

Flatbed Market Conditions

Market conditions for the flatbed segment are currently characterized by extreme tightness. A 13% weekly increase in load posts, spurred by a surge in end-of-month shipping, has pushed volumes to levels that are 50% higher than the previous year and 39% above the five-year average (omitting 2021 and 2022). Simultaneously, available equipment posts declined by 3% last week, further intensifying the pressure. As a result of these shifts, the flatbed load-to-truck ratio reached 64.89, representing a 10% decrease.