U.S. trucking activity hit a bit of a speed bump this spring, with the ATA Tonnage Index May 2026 contracting by 2% in May following a 0.9% slide in April. According to ATA Chief Economist Bob Costello, a strong 4.7% gain during the first quarter was offset by a 2.9% drop over the last two months. However, it is not all doom and gloom on the open road. Despite the recent monthly slowdown—largely driven by lackluster performance in core freight-generating sectors like manufacturing and construction—tonnage still managed to outpace year-earlier levels for the sixth consecutive month, proving the industry’s underlying resilience.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Diving into the data, the seasonally adjusted index landed at 114.4, representing a modest 0.6% increase compared to May 2025, while overall year-to-date tonnage remains up by 2%. Because trucking serves as a critical barometer for the broader U.S. economy—carrying a massive 72.7% of all domestic freight tonnage and pulling in nearly 77% of total transportation revenue—these shifting numbers offer vital clues about macroeconomic health. While contract freight continues to dominate over the volatile spot market, analysts will be keeping a close eye on the final report early next month to see if this recent dip is just a temporary detour or a sign of a longer plateau.

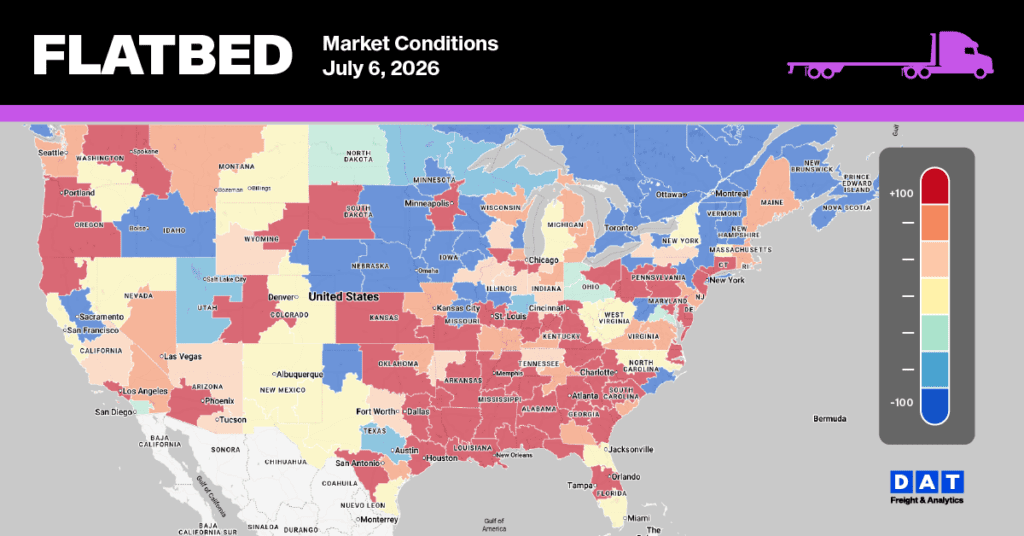

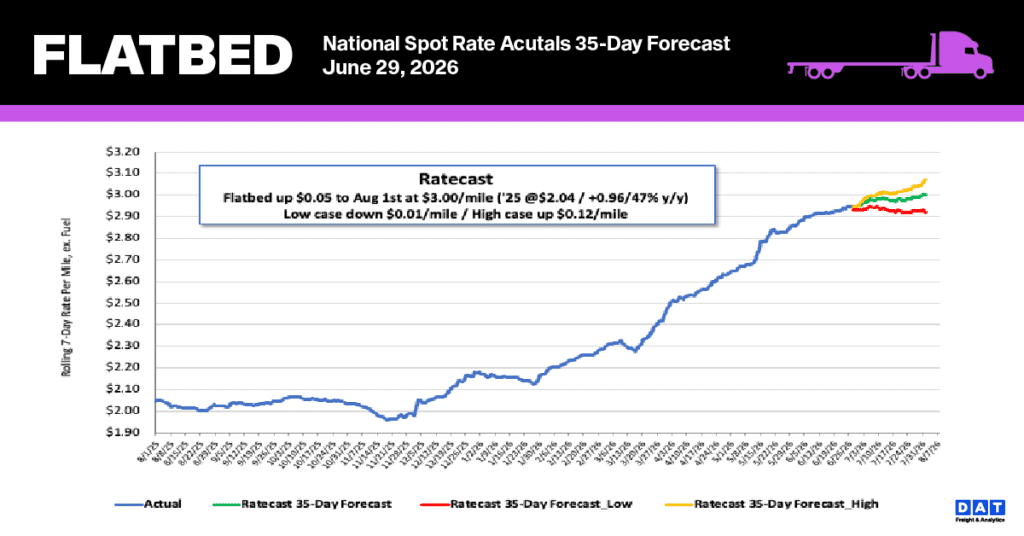

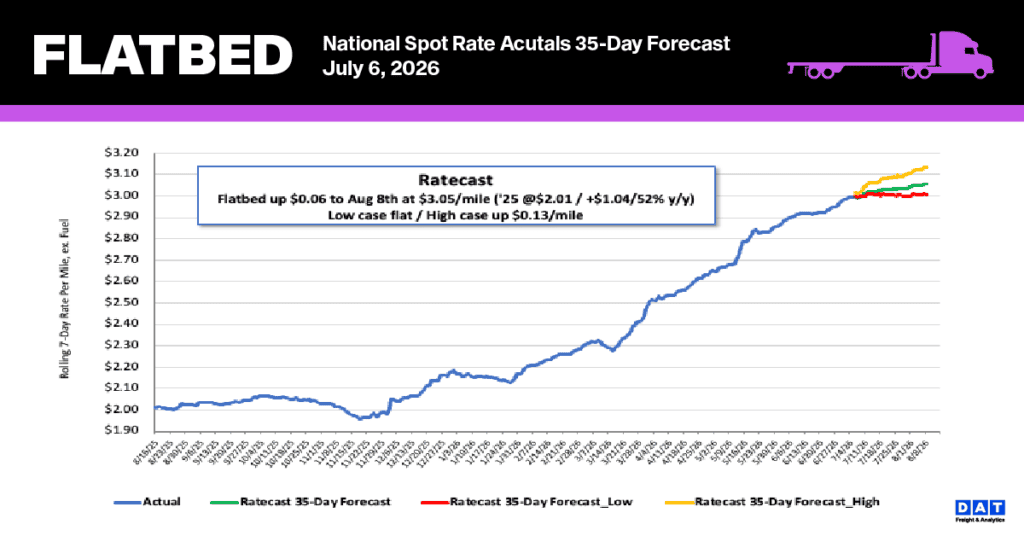

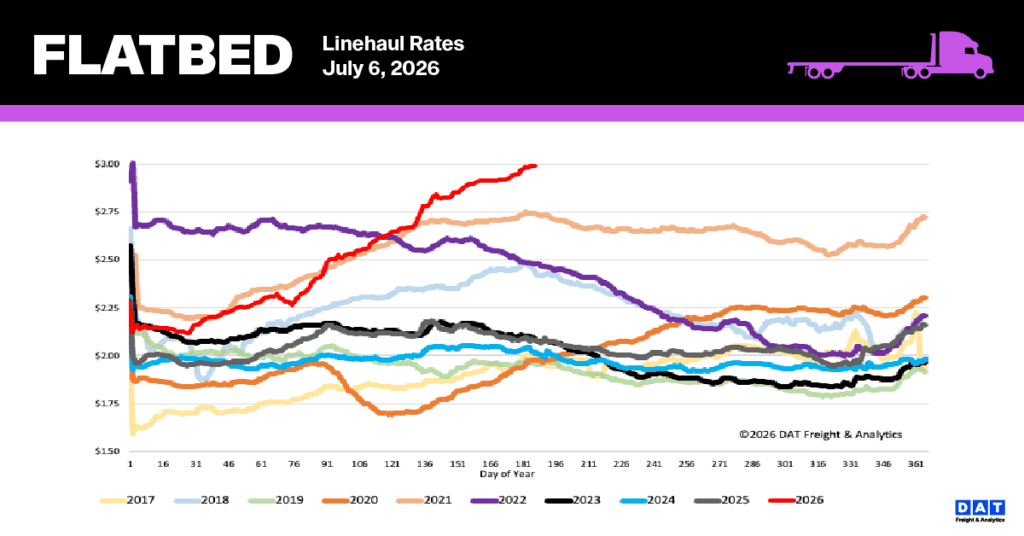

National flatbed spot rate trends

National flatbed spot rates achieved a new $3.00 milestone this week, bolstered by a $0.03 per mile increase. The 7-day rolling average, excluding fuel, has reached an all-time record, significantly outperforming historical norms. Current rates are 44% ($0.91) higher than last year and 32% ($0.96) above the non-pandemic five-year average. Furthermore, this pricing exceeds the previous record established in 2021 by 9%, or $0.24 per mile.

- Regional Bellwether Performance (TX, GA, PA, AL, OK, IL, TN, SC, AR, CA): Rates in this vital 10-state industrial corridor—which accounts for nearly 55% of national load volume—increased by $0.05 to an average of $3.58 per mile as route capacity tightened slightly.

- Market Significance: These bellwether states encompass the nation’s primary steel mills, energy hubs, and building-product plants. While the heavy nature of metals, energy, and construction freight causes weekly volatility, key markets like Texas, Georgia, and Alabama remain the most reliable indicators of the national flatbed rate trajectory.

Flatbed Market Conditions

Load post volumes in the flatbed sector have reached a seasonal summer plateau, currently tracking 55% above previous year levels. As equipment availability tightened by 20% year-over-year, the national flatbed load-to-truck ratio experienced a 24% decline, settling at 43.12.