When the current freight market cycle ends and the next one begins, one thing is for sure: We’ll need more drivers and trucks. After the amount of for-hire carriers doubled between mid-2020 and the end of 2021, the industry has witnessed a slow exodus of carriers since. When the market turns, there’ll be fewer trucks and drivers to handle more loads; the big question is when in 2024 this will occur.

As we start 2024, large truckload carrier capacity levels continue to contract after an unprecedented expansion. They are right around the same level they were at the end of the second quarter in 2020, immediately after the pandemic upended the economy and demand crashed.

According to the Journal of Commerce, truckload carrier capacity, measured by the number of trucks in publicly listed trucking companies each quarter, continues to contract after an unprecedented expansion.

Washington jumps in to grease the skids

Late last year, the U.S. Department of Transportation’s (USDOT) Federal Motor Carrier Safety Administration (FMCSA) announced it would award approximately $48 million in grant funding to increase commercial driver’s license (CDL) driver training opportunities and continue to improve the process to obtain a CDL. This funding aims to improve our national supply chain’s resiliency and strengthen America’s trucking workforce.

“Every day, we all count on food, clothing, medicine, and other goods that reach us thanks to America’s truck drivers,” said U.S. Transportation Secretary Pete Buttigieg. “With these grants, we are helping states bring more well-trained drivers into this essential field, strengthening our supply chains for years to come.”

FMCSA is awarding more than $44 million to states and other entities to operate national CDL programs through the Commercial Driver’s License Program Implementation (CDLPI) grant. This will help states expedite CDL issuance and renewals and ensure states electronically exchange conviction and disqualification data. It will also implement regulatory safety requirements supporting the National Roadway Safety Strategy and develop human trafficking outreach and education materials for CDL drivers.

Examples of projects funded include:

- Hiring state personnel to reduce CDL skills testing delays.

- Improving CDL reporting.

- Maintaining accurate driver records.

- Training CDL skills test examiners.

Focus on former military members given a priority

According to FMCSA Administrator Robin Hutcheson, “This essential funding provided through the CMVOST grant program will help expand and diversify the pool of trained drivers, with an important focus on attracting Veterans and individuals from underserved and refugee communities. We’re proud that these grants prioritize current and former U.S. Armed Forces members pursuing a commercial driver’s license, including National Guard, Reservists, and their family members.”

All rates cited below exclude fuel surcharges unless otherwise noted.

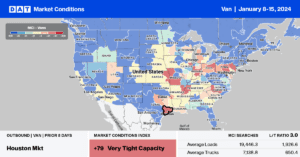

December imports increased by 5% compared to the prior month and 4% year-over-year (y/y), according to data from IHS Markit/PIERS. Compared to the prior December, last month’s containerized import volume was 5% higher than the December monthly average back to 2015, or 100,000 more containers/month or the equivalent of an additional 40,000 freight truckloads. The Port of Houston reported a 34% month-over-month (m/m) increase with an 11% share of the national total import volume, while New York, the second largest port in the nation, recorded a 12% m/m increase.

Load post volume in Houston’s spot market has increased by 66% in the first two weeks of the year, but with truckload capacity returning to the market, rates were mostly flat last week. On high-volume lanes between Houston and Dallas/Ft Worth, which accounted for 20% of spot market volume last week, linehaul rates were the lowest in 12 months, averaging $2.02/mile. Nationally, the top 5 markets, including Atlanta, Elizabeth, Chicago, Los Angeles, and Dallas, recorded a $0.03/mile decrease to an average of $1.67/mile after increasing for the prior three weeks.

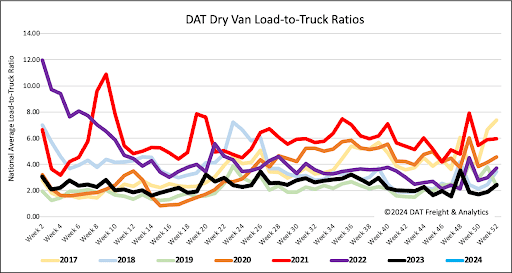

Spot market load post (LP) volumes were 46% lower than last year following last week’s 4% week-over-week (w/w) increase. Carriers returned to the market in much higher numbers last week – equipment posts (EP) increased by 41% following seasonal trends, although EP volumes remain 4% lower than the pre-pandemic average. Last week’s dry van load-to-truck ratio (LTR) was 2.40.

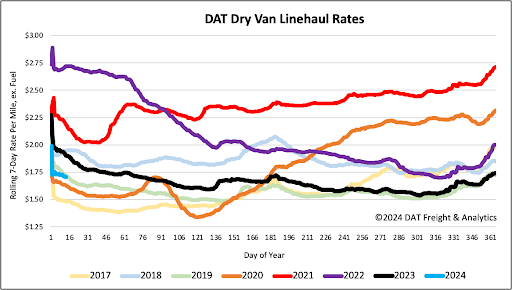

Dry van linehaul rates followed seasonal trends last week, decreasing by $0.02/mile to a national average of $1.71/mile. Spot rates are $0.20/mile lower than last year and $0.03/mile higher than the long-term average for this time of the year when capacity typically returns to the market. Based on the volume of loads moved, the top 50 lanes averaged $2.02/mile last week, $0.31/mile higher than the national average.