The March Logistics Managers’ Index (LMI) hit 65.7, the highest since May 2022, driven by a surge in Transportation Prices to 89.4—a 12.7-point jump. This is tied to the Strait of Hormuz closure, pushing national diesel to $5.40/gallon and California’s to a record $7.60, with carriers quickly passing on the cost. The 50.2-point gap between Transportation Prices (89.4) and Transportation Capacity (39.2) is the widest positive inversion since November 2021, signaling a harder and more expensive market for finding trucks.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Unlike the 2022 freight boom, current inventories are lean (LMI Inventory Levels at 54.8 vs. 75.7 in 2022), leaving shippers with less buffer against disruption. Smaller firms are hit hardest; they report Transportation Price expansion of 92.7, much higher than the 84.6 for larger counterparts, with fuel surcharges acting as “tariffs 2.0.”

For carriers, while rates are the best in four years, high diesel costs are squeezing margins, especially for small fleets lacking long-term fuel contracts and contracted rate floors. The rising rates are often offset by fuel surcharges. Twelve carriers over 100 employees filed Chapter 11 in March, signaling consolidation. However, tightening capacity (39.2) means growing pricing power for those who can withstand the cost pressure. Carriers should secure fuel surcharge agreements reflecting current diesel prices.

The forward LMI predicts Transportation Prices will hit 93.0 in the next 12 months. Aggregate logistics costs are nearing the 240+ historical inflation threshold. With Warehousing Capacity contracting and Transportation Capacity at its tightest since September 2021, brokers face expensive spot exposure. Shippers must pivot from lean inventory to shoring up carrier networks and revising fuel surcharge language now to avoid painful Q2 rate resets.

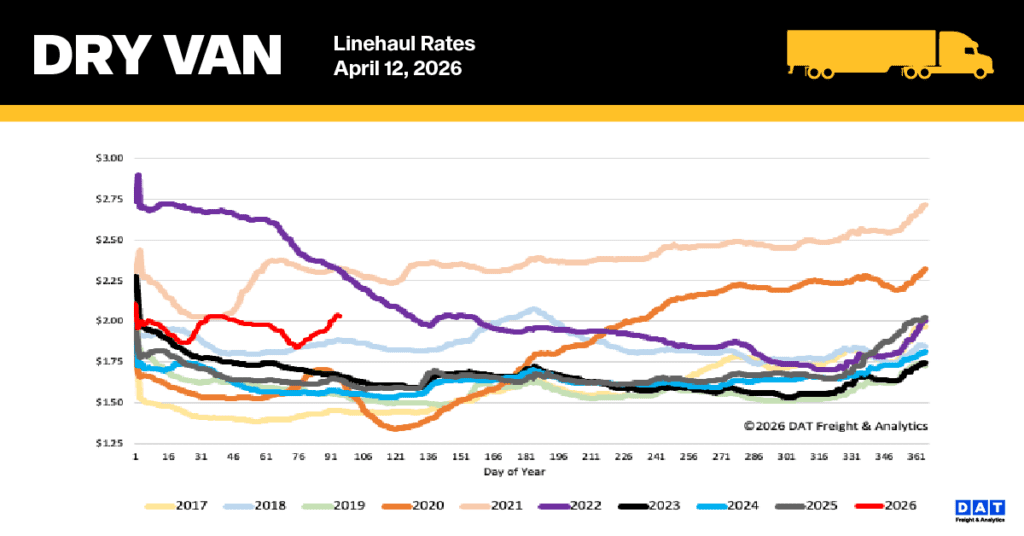

National dry van linehaul spot rates

The national 7-day average dry van linehaul spot rate (excluding fuel) stabilized early last week before declining by $0.04 per mile toward the end. This drop coincided with a retreat in retail diesel prices, which peaked at a national average of $5.90/gallon at the start of the week and then fell by $0.10/gallon to $5.80/gallon. Nevertheless, diesel costs remain significantly elevated, up $1.50 (35%) since the onset of the Middle East War six weeks ago.

The current linehaul rate of $2.00, when fuel is excluded, is notably elevated compared to historical data. This rate represents a 25% increase, or $0.40, over the rate from one year ago. Furthermore, it is $0.43 (22%) higher than the five-year average, excluding the years impacted by the pandemic.

Last week, spot rates on DAT’s top 50 lanes, based on load volume, experienced a minor drop of $0.01 per mile, settling the average at $2.39 per mile. This figure is $0.39 higher than the national 7-day rolling spot rate.

The average rate for the 13 key Midwest states, often viewed as a national bellwether and representing nearly half of the country’s load volume, decreased by $0.07 per mile, settling at $2.37 per mile. Importantly, this Midwest average continues to exceed the national 7-day rolling average by $0.37, a trend consistent with the performance of top lanes.

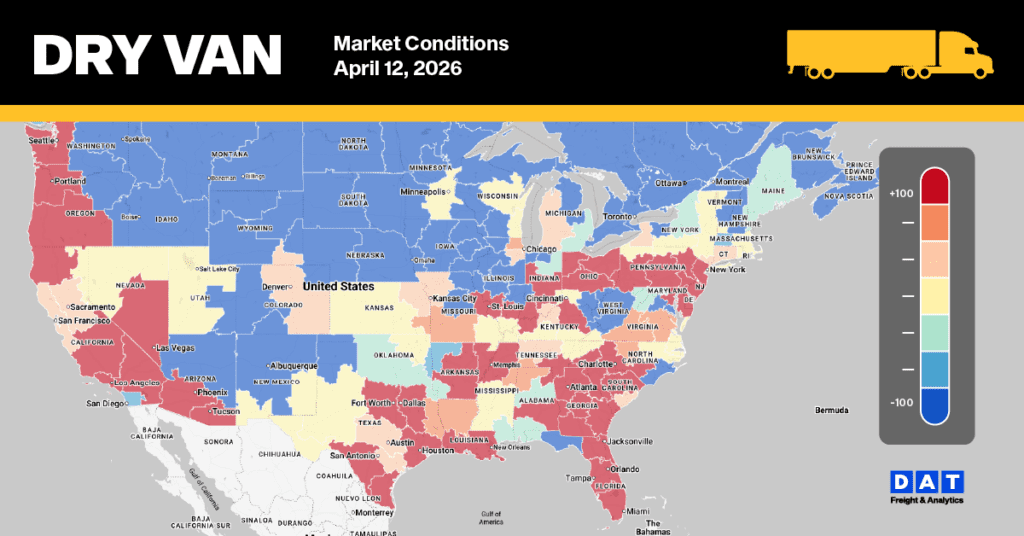

Dry Van Market Conditions

The national dry van load-to-truck ratio saw a 9% decrease last week, dropping to 8.02. This decline occurred despite robust load post volumes, which, while down 8% week-over-week, were still 70% higher than the previous year and more than double the long-term average for Week 15. The decrease in equipment posts, down 2%, indicates a continued reduction in available truckload capacity.