Nonresidential construction spending fell 0.6% in December, and the numbers underneath that headline are worse than they look for flatbed carriers and brokers. Manufacturing construction — the single largest nonresidential subcategory and a core flatbed freight driver — dropped 2.5% in December alone, its 11th consecutive monthly decline, and is now down nearly 16% from its August 2024 peak. That post-pandemic surge in domestic factory building, fueled by CHIPS Act incentives and reshoring tailwinds, has clearly crested. According to ABC Chief Economist Anirban Basu, trade policy uncertainty and the waning effects of federal stimulus mean manufacturing-related construction spending will likely continue declining for several more quarters. Twelve of 16 nonresidential subcategories posted declines in December, and total private nonresidential spending is now down 1.8% year over year — a broad-based softening, not an isolated blip.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

For flatbed operators, this is a demand signal worth watching closely heading into 2026. Construction-related freight — structural steel, rebar, lumber, equipment, and prefab components — has been one of the steadier load sources during an otherwise soft truckload cycle. With ABC’s Construction Backlog Indicator now at a four-year low, the forward pipeline is thinning. Highway and street construction, the third-largest nonresidential category, also slipped in December, removing another layer of load support. There were pockets of strength — power infrastructure spending ticked up 0.8% and office construction improved modestly — but those segments aren’t enough to offset the broader retreat. Flatbed capacity that repositioned toward industrial and manufacturing lanes over the past two years may face increasing rate pressure in 2026 as project starts slow and shipper volumes contract.

The interesting twist in freight economics is that construction spending behaves like a slow-moving glacier. Projects approved today generate truckloads months later. When the spending charts bend downward, flatbed demand rarely falls off a cliff—but the pipeline feeding it slowly narrows. For brokers and carriers trying to read 2026, this is one of those early signals that the construction-driven freight cycle is entering a different phase.

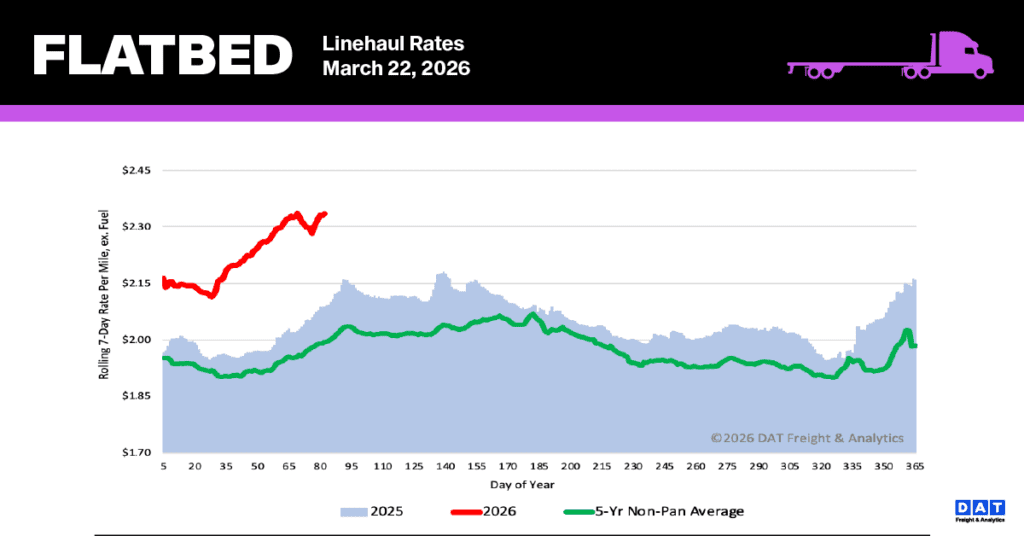

National flatbed linehaul spot rates

The national average spot rate for flatbed linehaul has risen to $2.34 per mile, marking a $0.03 increase last week. This rate is substantially higher than previous years, exceeding the rate from the same period last year by $0.25 (12%) and surpassing the five-year average (excluding pandemic years) by $0.35 (15%).

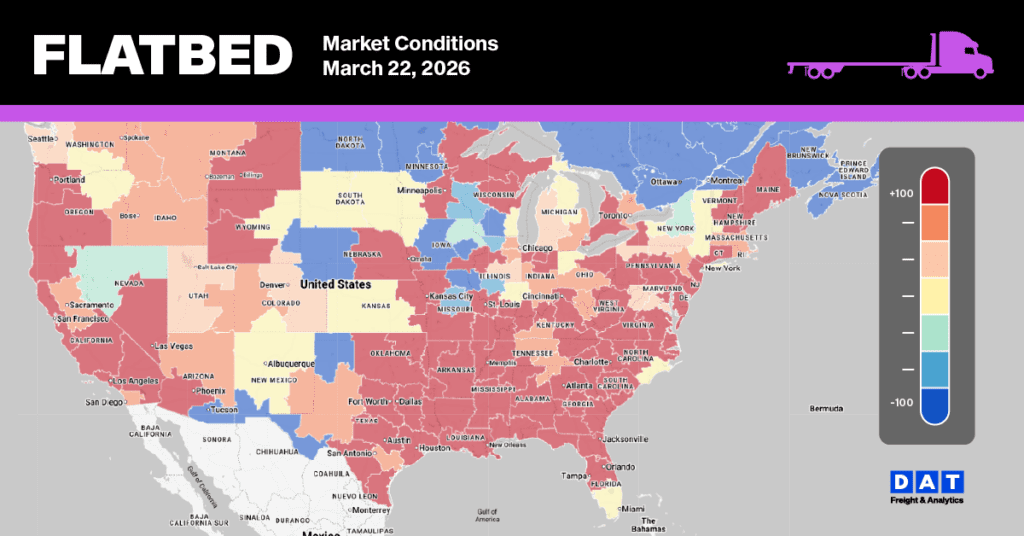

Flatbed Market Conditions

The flatbed market saw a significant tightening last week, with the load-to-truck ratio jumping 10% to 82.39. This climb was driven by a 2% week-over-week increase in flatbed load posts, which marked the highest weekly volume of the year and an impressive 46% rise compared to the same week in the previous year. Concurrently, flatbed equipment posts declined by 8% last week.