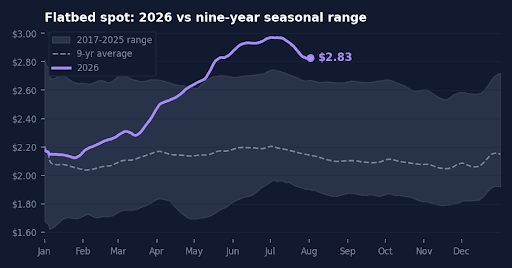

Every March, flatbed carriers along the East Coast and into the Mid-Atlantic feel a familiar tightening — and the Port of Baltimore is ground zero for why. March is the peak import month for farm equipment at Baltimore, the point in the calendar where vessel arrivals loaded with tractors, combines, excavators, and balers align almost perfectly with the start of planting season in the Midwest and the ramp-up of construction activity across the region. It’s not a coincidence. It’s a supply chain designed around the agricultural calendar, and it turns Baltimore into one of the most intense flatbed freight events of the year.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The reason Baltimore dominates this freight category starts with geography and ends with relationships. The port is closer by 150 miles than any other mid-Atlantic harbor to Midwest markets, making it the nation’s largest ro/ro transportation hub for nearly every major ag equipment manufacturer in the U.S. The customer list reads like a who’s who of heavy iron: John Deere, CNH Industrial (Case IH and New Holland), AGCO (Fendt and Massey Ferguson), Caterpillar, CLAAS, and Komatsu all move equipment through Baltimore’s ro/ro terminals. CNH alone averages between 14,000 and 16,000 units annually through the port, covering everything from large tractors and combines to excavators and wheel loaders. AGCO maintains an assembly facility just 27 miles from the port, where Fendt and Massey Ferguson tractors arriving from Europe are prepped for North American distribution. In 2024, Baltimore ranked first in the U.S. for roll-on/roll-off farm and construction machinery — a title it has held for years and is not in danger of losing.

For flatbed carriers, the downstream freight opportunity is substantial. Heavy farm equipment doesn’t move in a dry van — it moves on step-decks, RGNs, and flatbeds, often requiring permits and escorts for the largest units. When March import volumes surge at Baltimore’s Dundalk and Seagirt terminals, that freight fans out across a wide geography: north toward Pennsylvania and New York, west into Ohio and Indiana farm country, and south through Virginia and the Carolinas toward construction corridors that are ramping up with the warming weather. The convergence of ro/ro import peaks, planting season urgency, and spring construction starts creates a narrow window where demand for open-deck equipment is high, transit timelines are tight, and shippers are less rate-sensitive than at any other point in the year. For carriers positioned in the Baltimore market in late February and early March, the timing couldn’t be better.

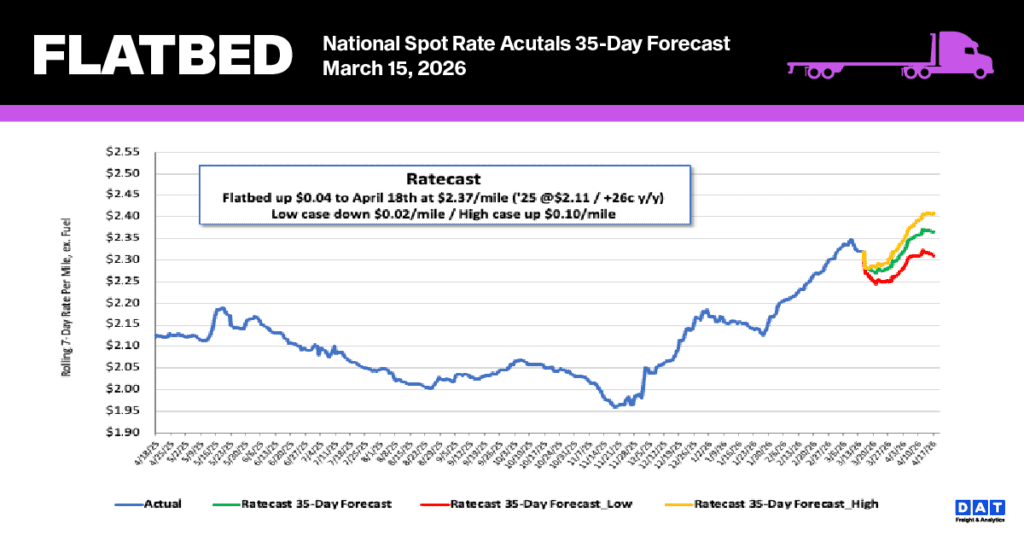

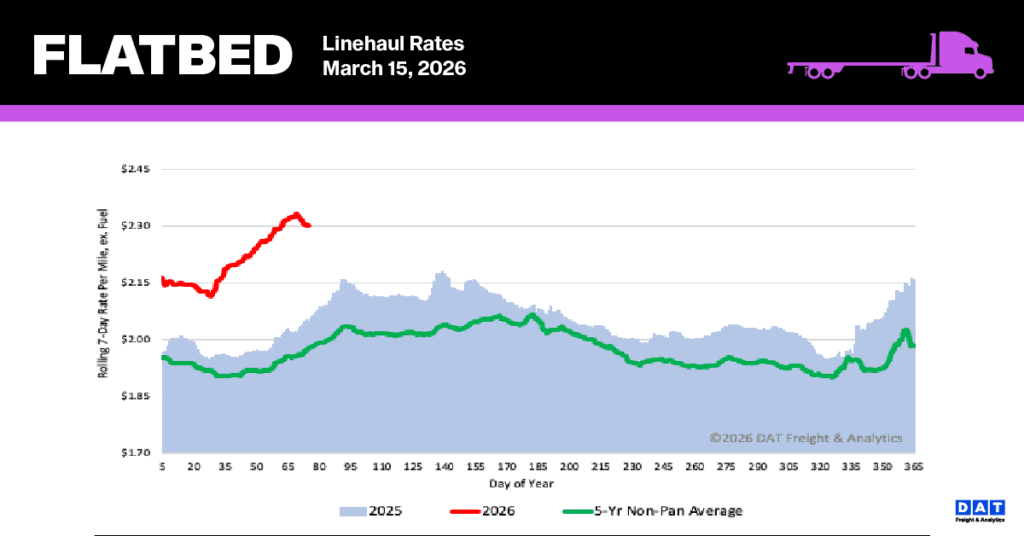

National flatbed linehaul spot rates

The national average spot rate for flatbed linehaul dropped to $2.31 per mile after a $0.02 decline last week, interrupting a six-week upward trend that had seen rates increase by $0.16 per mile. Despite this recent dip, the rate remains significantly elevated compared to historical data: it is $0.25 (12%) higher than the rate from the same period last year, $0.12 higher than the 2018 rate, and surpasses the five-year average (excluding pandemic years) by $0.34 (15%).

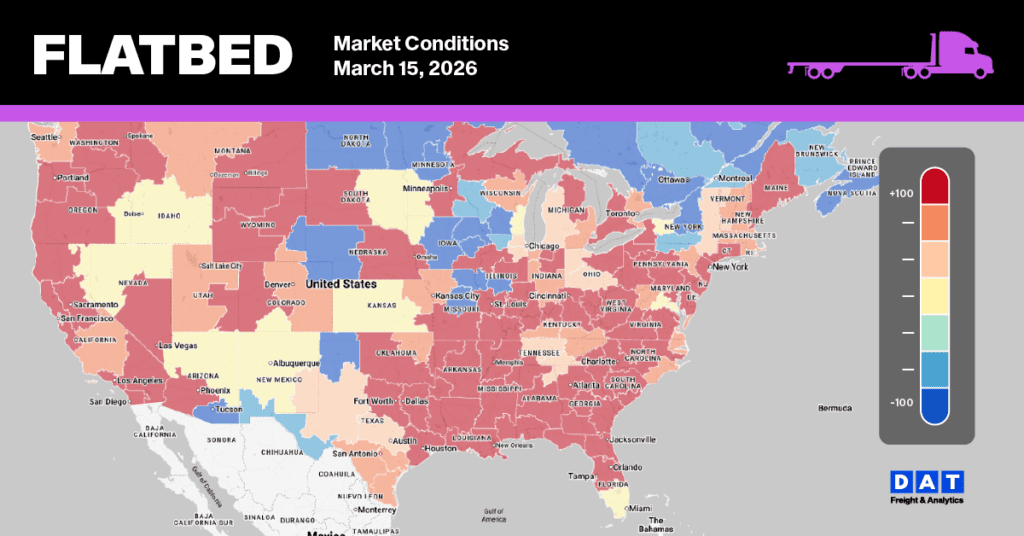

Flatbed Market Conditions

Flatbed load post volumes experienced a 7% increase last week, marking the highest weekly volume so far this year and an almost 47% rise compared to the same period last year. This increase in loads, combined with flatbed equipment posts remaining largely unchanged for the second consecutive week, resulted in the flatbed load-to-truck ratio climbing 10% to 76.39.