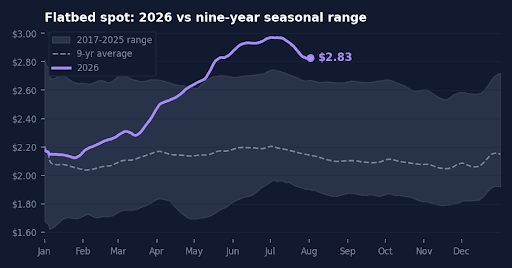

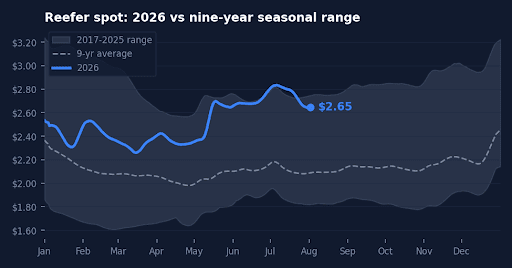

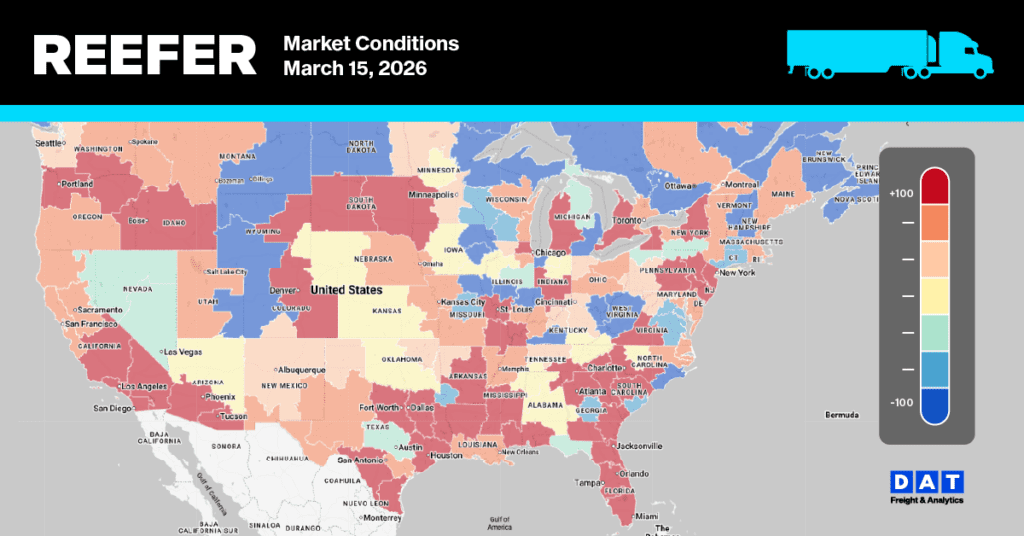

The big picture

Last week’s all-Adequate reset? Gone. Slight Shortage conditions are back at three of the four biggest produce origins — Nogales, South Texas, and Central Florida — and the rate moves are significant. South Texas posted the largest increases in the report with lanes up +13% to +28%. Nogales surged +5% to +13% on most eastbound lanes. Even Florida, after four straight weeks of declines, reversed course with rates up +7% to +12%. California remains the outlier: flat rates, Adequate capacity, and no drama. The spring tightening may have just started.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

South Texas: The biggest moves in the report

Mexico crossings through South Texas posted double-digit rate increases on nearly every lane. Truck availability shifted to Slight Shortage on five lanes (Baltimore, Boston, Miami, New York, Philadelphia), with the remaining four at Adequate.

That +28% to Chicago is the single biggest lane move in the entire report. With Mexican import volumes building into spring and Florida’s diminished crop supply redirecting demand to the border, South Texas is now the tightest produce origin in the country.

According to DAT RateView, carriers hauling reefer loads from McAllen to Chicago are seeing a significant increase, with rates this week commanding $1,100 more than they did at the same time last year. This surge in demand is further evidenced by a 16% week-over-week jump in reefer load posts, which are now 37% higher than last year. Overall, outbound reefer rates from McAllen, across all commodities and destinations, are up 19% year-over-year.

Nogales: Tightening returns after one-week pause

Nogales snapped back hard after last week’s mixed performance. Truck availability split between Adequate (Atlanta, LA) and Slight Shortage (Baltimore, Boston, Chicago, Dallas, New York, Philadelphia) — a significant shift from all-Adequate last week.

The general trend is one of significant tightening across most lanes, with the exception of the Atlanta lane, which dropped 10% this week after a 15% jump last week. The established tightening pattern eastward out of Arizona is notable. Carriers hauling reefer loads from Nogales to Atlanta are seeing a substantial premium, averaging $1,400 more per load compared to a year ago, according to DAT RateView.

The Baltimore reefer lane shows an even greater increase, with carriers earning an average of $2,100 more per load than last year. Reflecting this surge, reefer load posts on this lane are up 58% already this week and are 69% higher than last year.

Florida: The slide reverses

After four consecutive weeks of rate declines, Central and South Florida flipped positive this week. Truck availability shifted back to a mix of Adequate (Atlanta, Chicago) and Slight Shortage (Baltimore, Boston, New York, Philadelphia), and rates moved up across the board.

These rates are still well below where they were five weeks ago during the initial spike, but the reversal is meaningful. The question: is this the start of a seasonal firming pattern, or a one-week bounce before further softening? According to DAT RateView, carriers hauling reefer loads outbound Lakeland, FL are seeing reefer spot rates 23% higher y/y, following last week’s 7% increase in linehaul rates.

California: Flat and steady — the exception

Every California region remains at Adequate truck availability with zero rate movement on produce lanes week-over-week. Imperial/Coachella, Kern, Oxnard, Santa Maria, and South/Central districts all held perfectly flat to Baltimore and Philadelphia.

According to DAT RateView, carriers hauling reefer loads for all commodities outbound California are earning 13% (+26 cpm) more than a year ago, and 14% more in the larger produce growing market in Fresno.

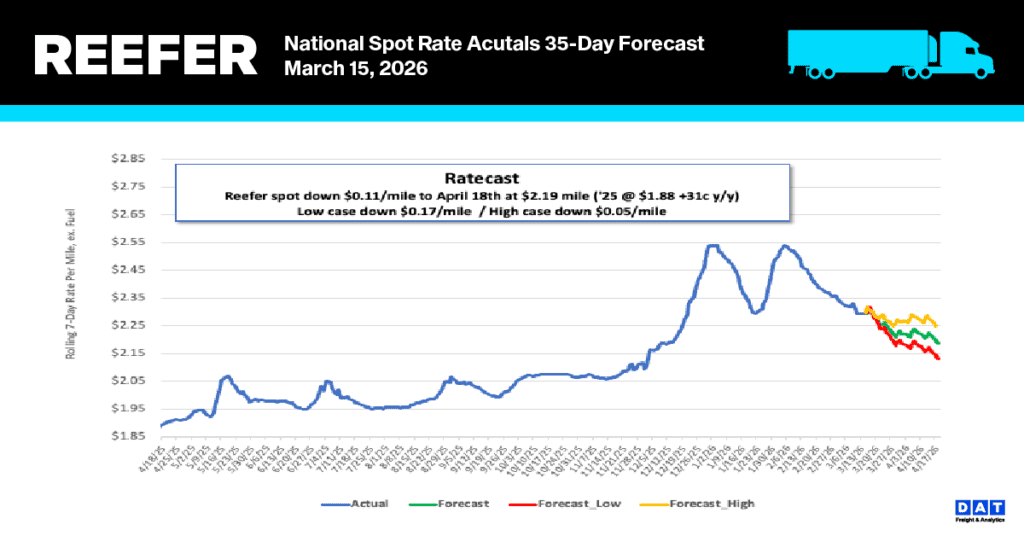

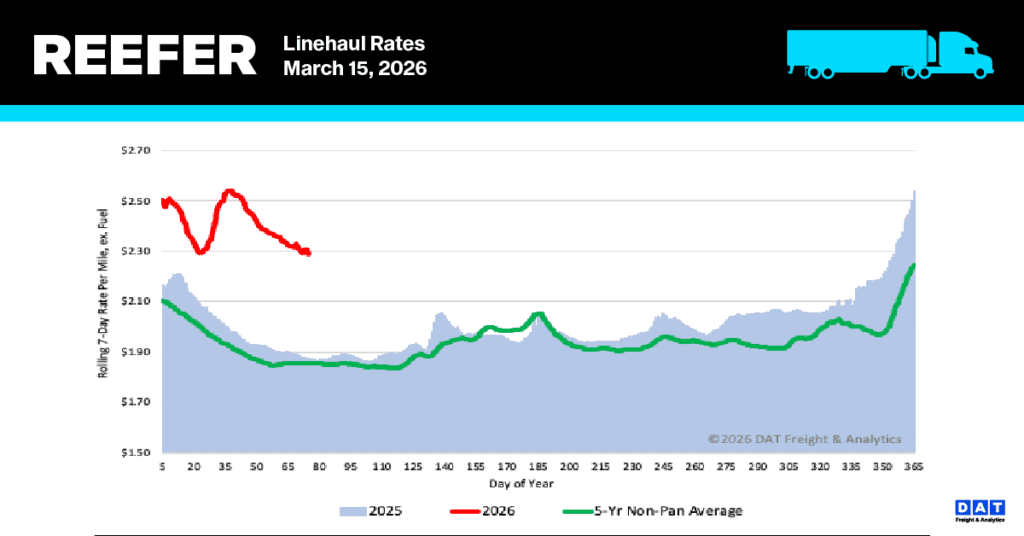

National reefer linehaul spot rates

The national average reefer spot rate (excluding fuel) has experienced its largest single-week decline this year, dropping $0.08 per mile to reach $2.30 per mile. This recent decrease nullifies the rate gains achieved during last month’s Winter Storms Fern and Gianna, and more. This marks the fifth consecutive weekly decline, totaling a $0.26 per mile drop. Despite this ongoing slump, the current average reefer linehaul rate remains significantly higher than historical levels. It is $0.41 per mile (22%) above the rate from the same period last year, and $0.44 (19%) higher than the five-year average (excluding the 2021 and 2022 outliers).

Reefer Market Conditions

Reefer load post volumes increased 4% last week—nearly double the volume from this time last year—driven by a 9% rise in domestic produce volumes and a surge in outbound loads of lettuce from Yumas, AZ . This, combined with a 6% drop in available reefer equipment posts, pushed the load-to-truck ratio up by 11% to 16.05.