The Big Picture

Mother Nature is reshaping the produce freight map. California storms and Florida’s freeze are pulling supply out of the two biggest shipping regions in the country — and yet, rates aren’t responding the way you’d expect. Florida continues to slide for the second straight week, reefer rates down 15% , California capacity is loosening from Shortage to Slight Shortage as reefer spot rates slid 3% last week, and the real tightening is now showing up at the border in South Texas. This week’s story is about where damaged crop supply is creating freight opportunities — and where it isn’t.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The weather story: two regions, major damage

California storms hit the Central Valley hard last week. Produce volumes were down 14% week-over-week and are running 30% lower year to date, according to USDA data. The physical damage is real: at Fresno State’s agricultural fields, almond blossoms were knocked off by wind and rain — reducing future yields. Wheat crops have been knocked on their sides, and muddy fields are delaying normal farm activities. This isn’t just a one-week disruption; the yield impacts will ripple through spring and summer.

Florida’s freeze (Winter Storm Fern) continues to cast a long shadow, with an estimated $3.1 billion loss to Florida’s agricultural industry. Florida fruit and vegetable produce volume is 30% lower year to date. The crop damage is severe: up to 80% of remaining strawberry harvests were hurt by the freeze, and roughly 90% of the remaining blueberry crop was impacted. That’s not a blip — that’s a structural reduction in what Florida can ship for the rest of this season.

South Texas: The new hot spot

While Florida fades, Mexico crossings through South Texas are tightening. Truck availability shifted to slight shortage on five of nine lanes (Atlanta, Baltimore, Boston, New York, Philadelphia), up from Adequate last week.

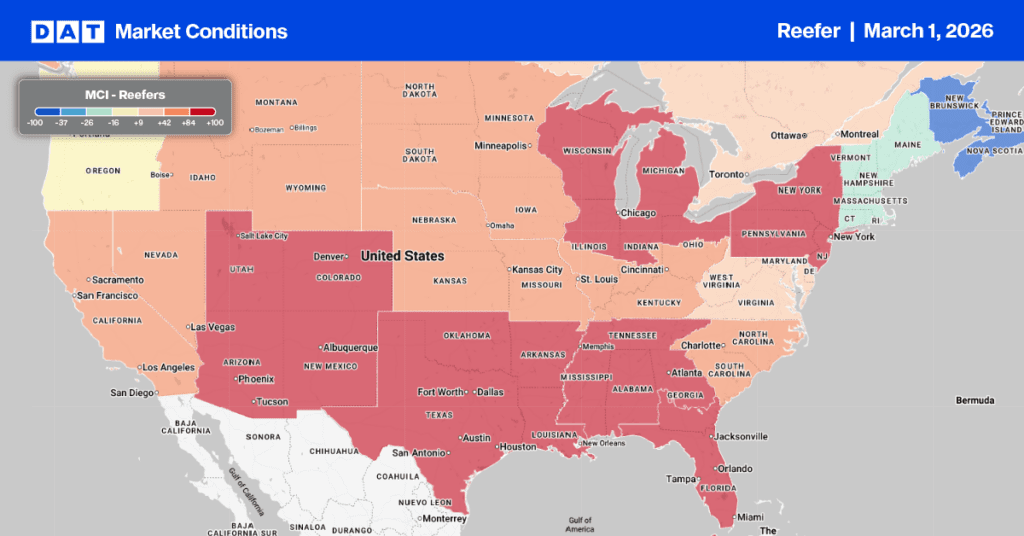

California: Capacity loosens, but the damage is done

A significant shift this week: California’s produce regions moved from shortage to slight shortage across Imperial/Coachella, Kern, Oxnard, Santa Maria, and South/Central districts. Reefer rates softened accordingly, down $0.07 per mile with several lanes showing modest declines or rates resetting (many lanes lack week-over-week comparisons, suggesting new rate baselines).

California citrus showed broader softening this week: Boston dropped -7%, Miami -4%, Philadelphia -4%, Chicago -3%, and Seattle -3%. The combination of storm-reduced volumes and loosening capacity is pulling rates lower — but the 30% year-to-date volume deficit means there’s simply less freight to move.

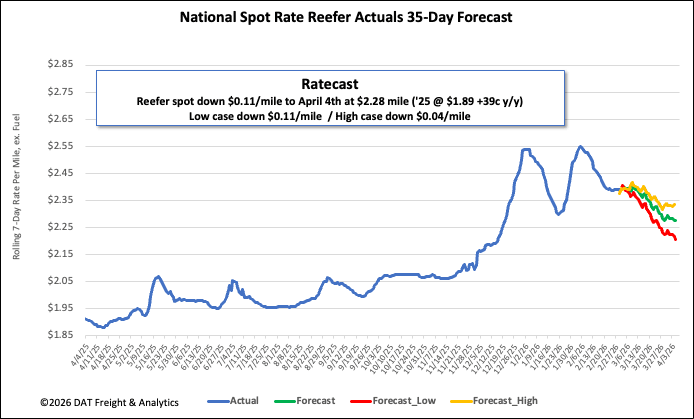

National reefer linehaul spot rates

The national average reefer spot rate, excluding fuel, has settled at $2.41 per mile, remaining significantly elevated. Despite declining for the third consecutive week—a total drop of $0.16 per mile, including a $0.05 per mile dip last week—this rate is notably high. It is $0.51 per mile (27%) higher than the rate for the same period last year and $0.56 per mile (23%) above the 5-year average (excluding pandemic years).

Reefer Market Conditions

After four straight weeks of decline, reefer load posts rose by 4% last week. This recovery was mainly fueled by an 11% week-over-week increase in produce volume and a surge in end-of-month shipping, highlighted by a substantial 32% jump in produce imports from Mexico. This increased demand, combined with a 6% drop in reefer equipment posts, led to a 12% boost in the load-to-truck ratio, which now stands at 15.76.