January 2026 farm equipment sales data from the Association of Equipment Manufacturers (AEM) paints a cautious picture for agricultural activity heading into the new year. Total farm tractor sales fell 4.7% year-over-year to 8,771 units, with the headline decline driven largely by weakness at the high end of the market — tractors over 100 horsepower plunged 25.9% compared to January 2025, and 4WD tractors dropped 18.8%. These large-horsepower machines are the workhorses of row crop and grain farming operations, so a pullback of that magnitude suggests that major commodity producers are tightening capital budgets, likely reflecting the severe cost-price squeeze gripping the farm economy. USDA slashed its 2025 net farm income estimate by $25 billion and projects continued pressure into 2026, with corn prices down more than 50% from their 2022 peak while production costs have barely budged — leaving many large grain operations at or below breakeven even after government assistance.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

The one bright spot in the report has direct implications for freight capacity: self-propelled combine sales surged 68% year-over-year in January, jumping from 97 to 163 units. While January is an off-season month for combine purchases and the absolute numbers are small, a move like that can signal farmers locking in equipment ahead of the 2026 harvest cycle — a potential indicator of production confidence in certain crop segments. For carriers and brokers watching the ag freight calendar, the broader softness in large tractor sales tempers expectations for a robust spring planting season, which could weigh on demand for flatbed hauls of ag inputs like fertilizer and seed. Meanwhile, the combine uptick is worth watching as a leading indicator for harvest-season reefer and dry van volume later in the fall.

National flatbed spot rates

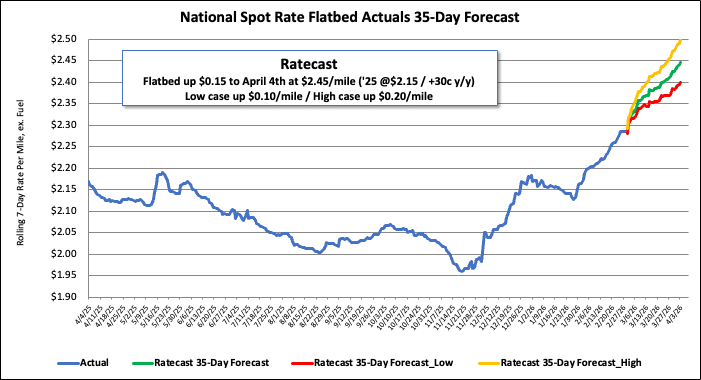

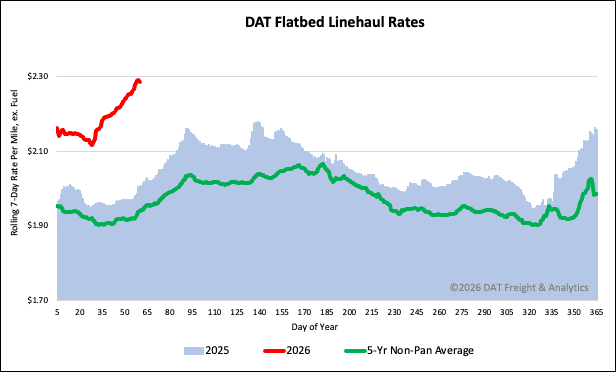

The national average spot rate for flatbed linehaul has reached a notably high level, settling at $2.29 per mile last week after increasing ($0.03) for the fifth consecutive week. This current rate is significantly higher than historical figures: it is $0.28 per mile (14%) above the rate from the same time last year, $0.15 per mile higher than the 2018 rate, and $0.35 per mile (15%) greater than the five-year average (excluding pandemic-impacted years).

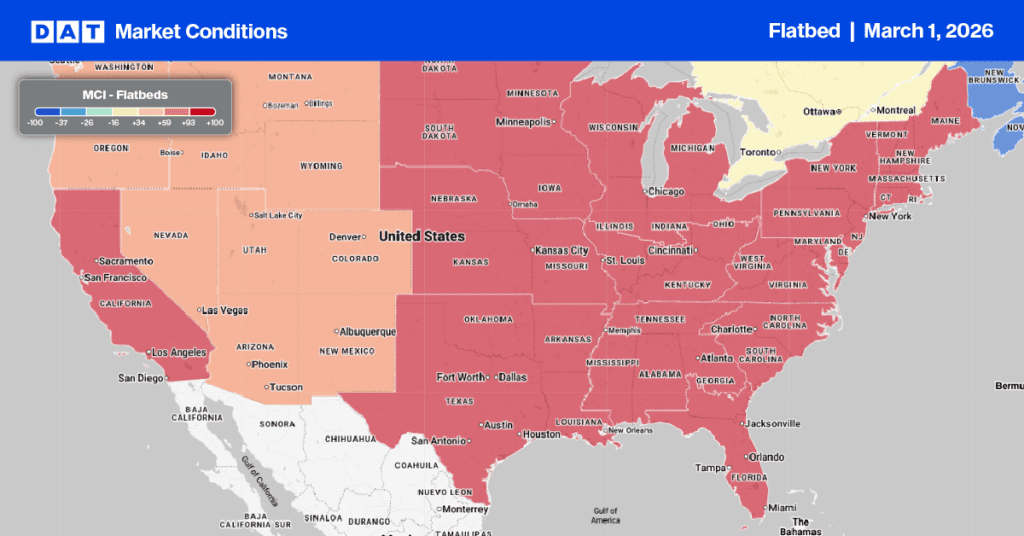

Flatbed Market Conditions

Flatbed load posts saw a 10% surge last week, driven by strong end-of-month shipping volumes. This increase reflects continued tightening of flatbed spot market capacity, with current volume nearly 43% higher than the same time last year. As equipment posts dropped by 10%, the flatbed load-to-truck ratio jumped 23%, reaching 70.34.