The Baker Hughes oil and gas rig count, an early indicator of future output and flatbed demand, increased by three units to a total of 782 in the week of November 18, the highest since March 2020. Compared to the previous year, the rigs count is up 219 or 39%, although current levels are still slightly below March 2020 at the start of the pandemic. One of the high-volume lanes for flatbed carriers hauling drill pipe and casing out of Houston is 600 miles west to Lubbock, TX, in the Permian Basin, where around half of the drilling rigs are located. Spot rates on that lane are currently at a 12-month low of $2.47/mile, down from $2.99/mile last year and almost $1.25/mile since this year’s peak of $3.72/mile in July. Lower linehaul rates on this lane reflect an oversupplied market more than lower demand.

Looking more broadly at national steel output, production for the week ending November 19, 2022, fell by 10.9% compared with the same time frame in 2021, according to the American Iron and Steel Institute (AISI). Adjusted year-to-date (YTD) production is 79,620,00 net tons, at a capability utilization rate of 78.7%, down 5.1% from the 83,877,000 net tons during the same period last year. In flatbed truckload equivalent terms, that’s approximately 170,000 fewer truckloads of steel this year. Year-to-date (YTD) total tonnage is down 14% YTD and closest to 2016 output levels trending 5% lower than six years ago. In the largest steel-producing market for flatbed carriers in Indianna, tonnage is down 22% YTD y/y.

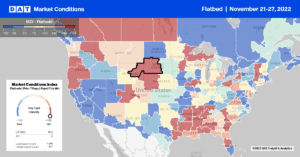

At the regional level, YTD tonnage through October is trending down in all five regions:

- Great Lakes: down 14% y/y

- Midwest: down 4% y/y

- Northeast: down 3% y/y

- Southern: down 9% y/y

- Western: down 12% y/y.

Market Watch

All rates cited below exclude fuel surcharges unless otherwise noted.

Although California outbound flatbed linehaul rates are identical to 2018 levels, they increased by $0.11/mile last week to $2.18/mile, the highest in the previous six weeks. In the Los Angeles market, rates jumped to $2.07/mile following last week’s $0.19/mile increase, driven mainly by tight capacity on the short-haul San Diego lane. Higher volume longer-haul lanes east to Phoenix were at a new 12-month low of $2.41/mile or around $1.60/mile lower than the previous year.

In the second-largest Christmas tree-producing state of North Carolina, flatbed linehaul rates increased by $0.22/mile to $2.47/mile last week, identical to 2020 levels. In the Southeast lumber-producing markets, including Georgia, Mississippi, and Alabama, spot rates increased to $2.39/mile following last week’s $0.14/mile gain. Load posts increased for the fifth week in Albany, NY, following a 12% w/w gain. Capacity was also tight for outbound loads at $5.02/mile, up $0.55/mile in the last week.

Load-to-Truck Ratio (LTR)

Flatbed load posts followed a typical seasonal pattern during last week’s short work week. Both decreased as expected, with load posts 70% lower y/y and now just 14% higher than in 2019. Carrier equipment posts remained at their highest level in six years and are now 10% higher than 2019 levels. As a result, last week’s load-to-truck (LTR) ratio decreased by 17% w/w 8.84 to 7.34, which is just 4% above 2019 LTR levels.

Spot Rates

After dropping for the prior seven weeks, flatbed linehaul rates increased last week by $0.01/mile to a national average of $2.05/mile. Compared to the previous year, last week’s average spot rate is 22% or $0.57/mile lower and now $0.10/mile lower than in 2017 but still $0.20/mile higher than the oversupplied 2019 flatbed market.