This week, industry expert Dustin Jalbert and the entire Fastmarkets Wood Products team take a look at the housing construction industry and what it means for flatbed carriers in 2022.

The strength in the housing market over the last two years has been impossible to miss and can be briefly underlined with price and inventory data. National home prices are pacing at 15-20% gains year over year. The scramble for bigger and better places to live has left the market depleted of inventory, with enough existing homes on the market for just 1.6 months of supply at January’s sales pace.

For context, 4.5 months’ worth of inventory would be normal. The surge in home buying and renovation activity spurred on by the pandemic occurred in an already-strong demand environment, underpinned by healthy demographics and a decade of underbuilding shelter. Squeezed by labor shortages and supply chain backlogs, home builders and contractors have struggled to keep pace.

Get the clearest, most accurate view of the truckload marketplace with data from DAT iQ.

Tune into DAT iQ Live, live on YouTube or LinkedIn, 10am ET every Tuesday.

Until recently, rising home prices did not deter buyers, as mortgage rates remained low for most of 2020 and 2021. Many households also had additional cash on hand from the combined effect of the coronavirus relief efforts. Since the Federal Reserve has announced aggressive rate hikes for the coming year to stem inflation, mortgage rates have been on a steep climb. Though rates have fallen slightly following the Russian invasion of Ukraine, they are likely to remain well above record lows seen over the last two years. The combination of higher rates and soaring home prices will be a headwind for homebuilding and, consequently, wood products demand. Some builders are throttling new construction as they struggle to complete existing projects. Rising cycle times and increasing concerns about affordability are only adding to builder wariness.

What’s 2022 going to look like?

Despite these challenges for the industry, the outlook for housing construction activity in 2022 remains generally positive. Demand for housing that existed prior to the pandemic has not gone away. Estimates of pent-up housing demand differ, but it is generally accepted that the housing market is underbuilt. There is also a shift underway towards more multifamily construction, thanks to the affordability issues and skyrocketing rents. The multifamily sector will be hampered less by the challenges mentioned above than the single-family sector.

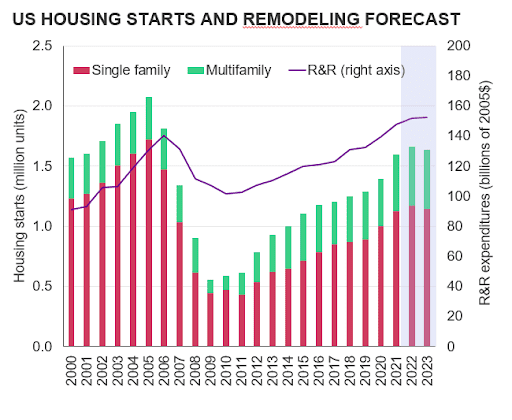

This year is shaping up to be the year in which the housing market transitions away from the rapid growth of 2020 and 2021. In 2021, there were 14% more homes started than in 2020. A slowdown from this unsustainable rate of growth was inevitable given labor and building material constraints that continue to plague the industry. We anticipate housing starts will grow 3.7% in 2022 to 1.66 million units. Repair and remodeling activity will grow at a similar pace, powered by soaring home equity, the rise of remote work, and historically low home inventory for sale on the market. Both lumber and structural wood panel demand in the US should march higher in 2022, advancing 5.8% and 4.3%, respectively.

Currently, wood products markets are going through yet another unprecedented price run, driven by bottlenecks in rail shipments from Canada and chronic trucking shortages. This contrasts with the mostly demand-driven price run of last summer. Sawmill inventories are reportedly swelling in Canada as production outpaces shipping capacity due to the lingering effects of historic flooding in British Columbia and as winter weather constrains shipping capacity. The situation is forcing mills to curtail production in response. It will take some time for normalcy to return, and there will be an additional layer of pressure on the flatbed market until that occurs.

What impact will the Russia-Ukraine conflict have on the U.S. construction industry?

Of course, the Russian invasion of Ukraine is a rapidly changing and uncertainty-laden event. The direct impacts on wood products demand in North America appear uncertain, but it is clear indirect effects from higher inflation will certainly play a role. It is likely that the conflict and sanctions will contribute to additional increases in food and energy prices, tying up an increased share of consumer budgets at the expense of expenditures on home improvement. We may also see some deterioration in consumer confidence, which could impact home sales down the road. The unexpected geopolitical turmoil will only provide further fuel to what has already been an incredibly volatile North American wood products market.