Since the new 1,400-foot berth Leatherman Terminal opened in April 2021, much larger container vessels have been calling on the Port of Charleston, South Carolina. Additional capacity has also resulted in more volume through the port. If we look closely at the number of TEU (twenty-foot equivalent units) imported before the new terminal and after, data from IHS Markit shows a 27% increase in average monthly TEU volume. That’s the equivalent of an extra 22,500 containers per month – or approximately 8,400 truckloads. China (27%) and Germany (15%) are the dominant countries of origin, with auto parts and furniture accounting for 9% and 8% of monthly TEU volume, respectively.

South Carolina Ports (SC Ports) said the port handled nearly 2.6 million TEUs and 1.4 million pier containers in fiscal year 2023. While this is down about 10% from fiscal year 2022 — when pandemic spending spurred an unprecedented cargo boom — volumes are up 1% from fiscal year 2021, a much more typical year. “SC Ports provides reliable, efficient service for companies’ supply chains,” SC Ports President and CEO Barbara Melvin said. “Port-dependent businesses will continue to invest in South Carolina to gain access to a well-run port with capacity in the booming Southeast market.”

SC Ports was ranked the 9th-largest U.S. port for imports in June, with a 4% market share.

Market Watch

All rates cited below exclude fuel surcharges unless otherwise noted.

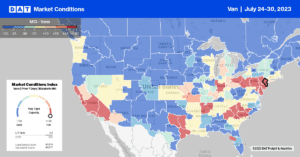

Dry van capacity has been tightening in Maine for the last three weeks following last week’s $0.17/mile increase to a state average of $1.84/mile. At this level, however, spot rates are still at their lowest level in seven years. On some of the longer haul lanes from Augusta, Maine, to Phoenix, rates have increased to $1.24/mile after decreasing since January. At $1.96/mile, regional loads to Elizabeth, New Jersey, are the lowest in 12 months. Capacity also tightened in the Massachusetts market following last week’s $0.06/mile increase to the state average of $1.29/mile, while in Springfield, spot rates were up a penny-per-mile to $1.43/mile.

Most markets in New England are considered strong backhaul markets, which typically means the head haul lane will reflect the lower outbound rates reported last week. For example, loads from Allentown to Boston were the highest since March at $3.33/mile; on the return leg, carriers were paid $1.57/mile. Allentown is a large distribution warehouse market serving the Northeast, so for dedicated carriers on this lane, the round-trip rate would be around $2.45/mile.

In the large Midwestern market of Indianapolis, spot rates increased a penny-per-mile to $1.83/mile, while in nearby Columbus, outbound loads paid carriers $1.78/mile, down $0.07/mile in the last month. On the West Coast in Los Angeles and Ontario, rates dropped for the fourth week to $1.89/mile and $1.96/mile, respectively.

Load-to-Truck Ratio (LTR)

End-of-month shipping boosted load posts last week, increasing by 6% week-over-week (w/w), just 2% higher than the year-to-date average for dry van volume. Fewer carriers posted their equipment looking for loads, down by 8% w/w, resulting in last week’s dry van load-to-truck ratio (LTR) improving by 15% – from 2.43 to 2.81.

Linehaul Spot Rates

Even though we saw an increase in volume last week, capacity continued to loosen following a $0.02/mile decrease in dry van linehaul rates. At $1.64/mile, the national average is $0.31/mile lower than in 2022 – but still $0.10/mile higher than in 2019. Compared to DAT’s Top 50 lanes (which averaged $1.97/mile last week), the national average was $0.33/mile lower.